Crypto Market Monitor – 16th November 2022

Powered by 21Shares

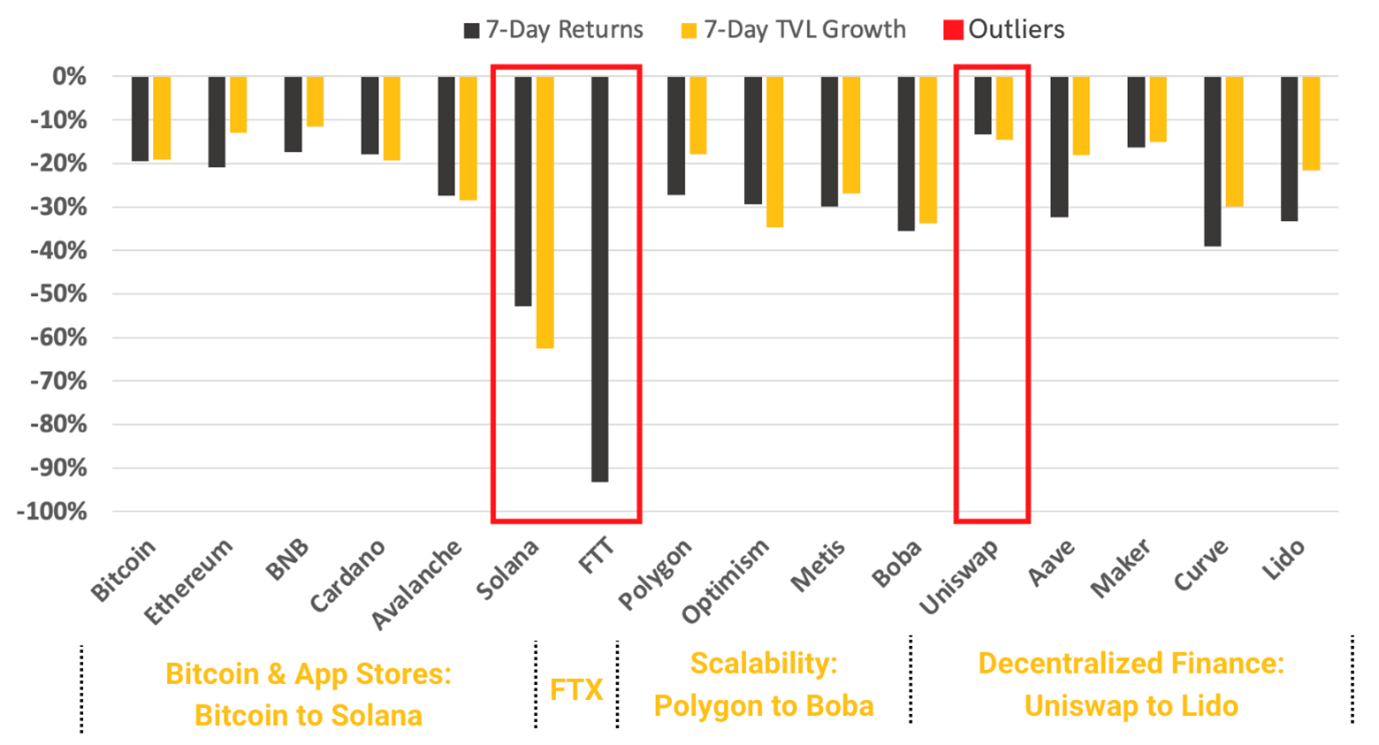

It was one of the most shocking weeks in crypto history. On November 2, CoinDesk leaked Alameda’s balance sheet, showing that $5.2 billion of the trading firm’s $14.6 billion of assets (36%) were held in FTT, a token issued by the now-bankrupt FTX crypto exchange. In light of these revelations, Binance chose to sell a portion of FTT on its books, which spooked investors and prompted a bank run on FTX. By November 8, FTX had halted withdrawals, and the price of FTT had dropped more than 85% since the CoinDesk report came out. After failing to raise capital, on November 11, more than 130 entities tied to FTX.com, FTX US, and Alameda Research filed for bankruptcy, with the Alameda petition listing assets and liabilities of at least $10 billion each. As of Monday’s close, Bitcoin and Ethereum are down by 19.42% and 20.85% week-over-week, respectively. In addition, among the top cryptoassets within the major categories, the most hurt is Solana, which declined by 52.82% over the same period. Below we will walk you through the events of the FTX debacle and what to expect in the coming weeks and months.

Figure 1: Weekly TVL and Price Performance of Major Crypto Categories

Source: Messari (Close Price) and DeFi Llama, Data as of November 14, 2022

Key takeaways:

- More than $1.5 billion in liquidations between November 6-11.

- Ether’s net issuance since the Merge has turned negative.

- FTX US, FTX.com, and Alameda filed for bankruptcy with a multi-billion dollar hole in their balance sheets.

- Binance among a number of crypto exchanges to provide proof-of-reserves.

Spot and Derivatives Markets

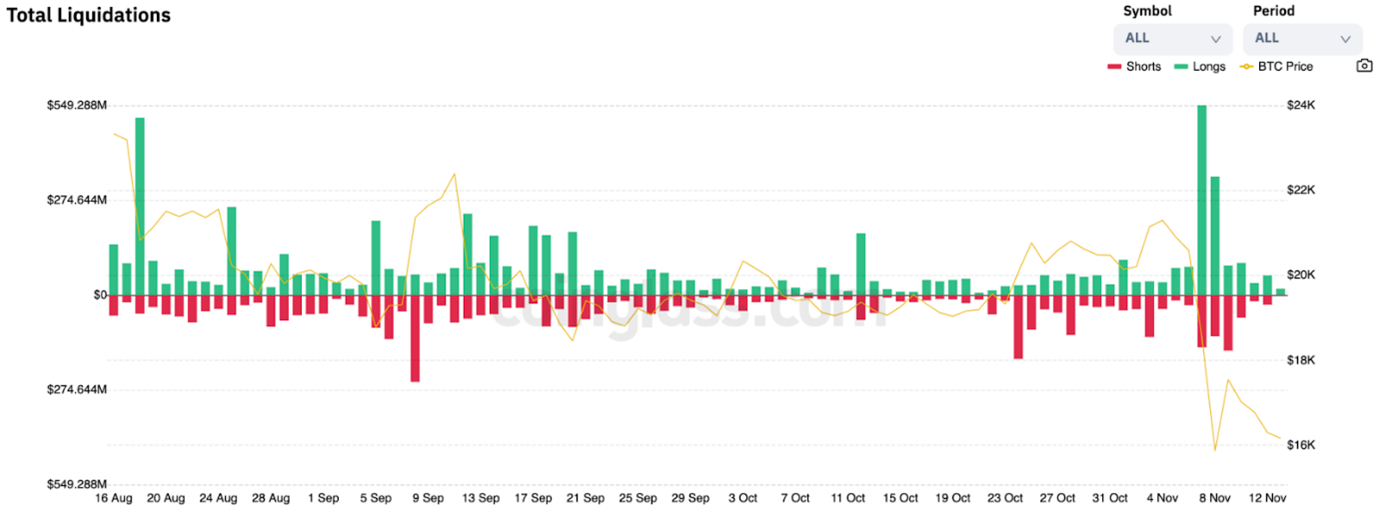

Figure 2: Total Liquidations (Longs and Shorts) Over the Past Three Months

Source: Coinglass, Data as of November 13, 2022

If we look at the derivatives market, between November 6 and 11, we saw more than $1.5 billion of liquidations (primarily longs) as BTC’s price breached below $16,000 for the first time since November 2020. This event constituted the most significant long liquidations in recent months (see Figure 2), indicating that many investors were positioned to the upside amidst the FTX debacle.

On-chain Indicators

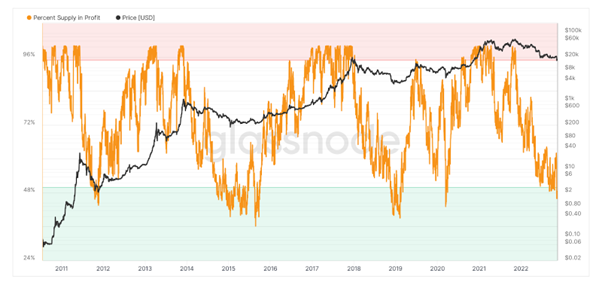

Figure 3: BTC Percent Supply in Profit.

Source: Glassnode, Data as of November 13, 2022

Figure 3 highlights the percentage of the current BTC circulating supply in profit. This metric represents an oscillator that allows us to understand the current state of the market better. Historically, values above 95% have coincided with market tops, while values below 50% have preceded past cycles’ bottoms. On November 9, the BTC percent supply in profit reached 45.93%, the lowest level since March 2020.

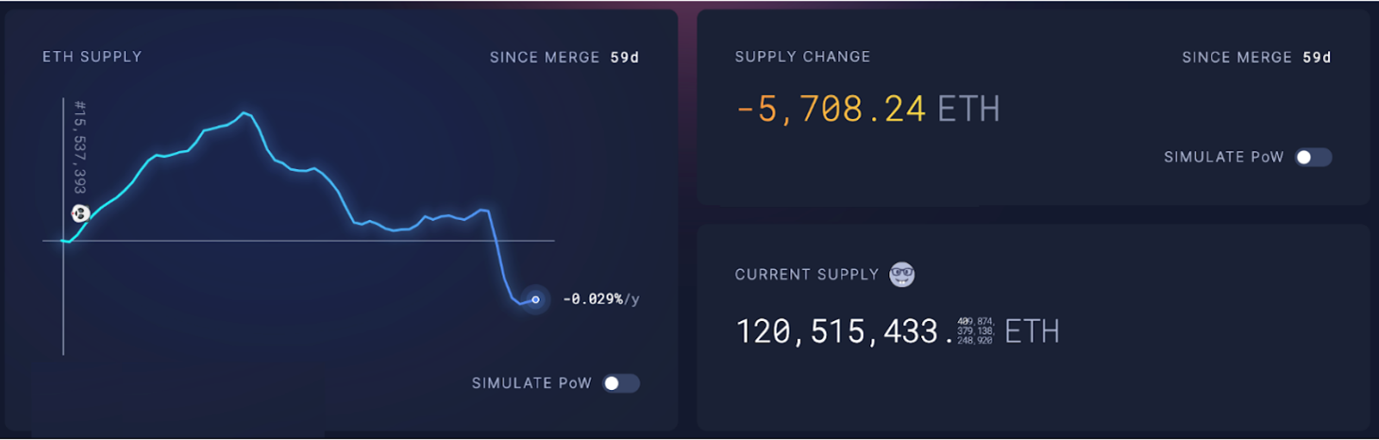

Figure 4: ETH Supply Change Since the Merge

Source: https://ultrasound.money/, Data as of November 13, 2022

On another front, Figure 4 shows that ETH’s net issuance since the Merge turned negative on November 8 (54 days after the switch to PoS) alongside an increase in the amount of ETH burned, a sign that the cryptoasset’s prospects as a deflationary asset depend heavily on network usage. In contrast, without the switch to PoS, the issuance would have increased by more than 700,000 ETH.

The FTX Debacle: What Happened?

To fully understand last week’s events, it’s necessary to go back a few years. Alameda Research was Sam Bankman-Fried’s first successful venture, a proprietary trading firm he founded in 2017 after getting his start arbitraging the Japanese Bitcoin premium. Then, in 2019, Bankman-Fried founded FTX, a cryptocurrency exchange marketed as a platform “built by traders, for traders.” FTX became one of the world’s largest crypto exchanges. At the same time, Bankman-Fried’s unique persona and “effective altruism” act intrigued crypto-native and traditional investors alike – even celebrities – all keen to invest in the business. FTX raised $1.8 billion over seven funding rounds from notable names such as Sequoia, Temasek, and Softbank, securing a $32 billion valuation in January of this year. So, what went wrong?

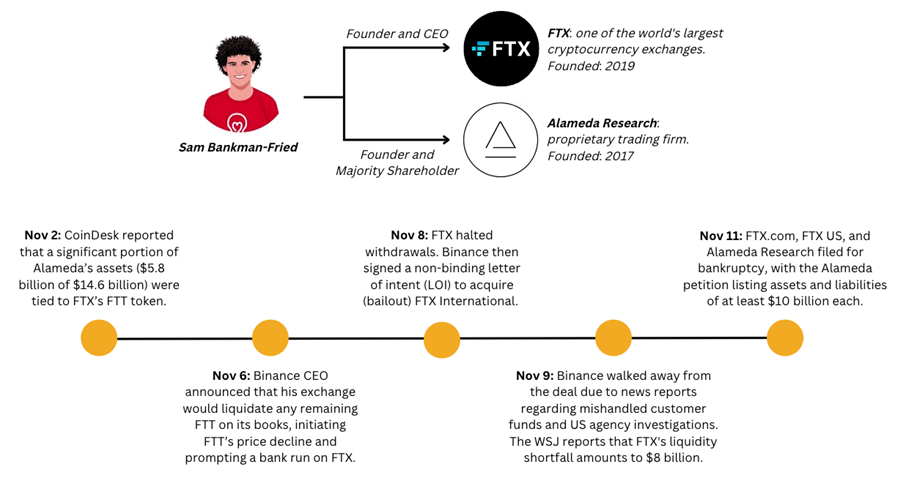

Figure 5 – Timeline of the FTX Collapse

Source: 21Shares

Alameda was the first market maker for FTX, giving the exchange the liquidity it needed to get off the ground. However, as the media increasingly pressured Bankman-Fried on the potential conflicts of interest, he expressed his intent on establishing clear “walls” between the two firms, which would operate as separate businesses in their respective verticals. Bankman-Fried publicly focused on his role as FTX’s CEO while remaining a majority shareholder of Alameda. On the other hand, Caroline Ellison became the sole CEO of Alameda in August of this year after her co-CEO Sam Trabucco stepped down. However, on November 2, a CoinDesk report showed that the division between the two entities broke down in one crucial place – Alameda’s balance sheet. Of the trading firm’s $14.6 billion of assets, $5.8 billion were held in FTT, a token issued by the FTX exchange that granted certain benefits to holders, such as lower trading fees. Another critical aspect of FTT was that one-third of FTX’s trading revenue was used to purchase and burn part of the FTT supply (the equivalent of retiring shares to increase the price of a stock).

Binance had been an early investor of FTX and, as part of its exit, received about $2.1 billion divided between BUSD and FTT. The CoinDesk revelations were troublesome, as the $5.8 billion Alameda held in FTT as of June 30, 2022, represented almost two times (1.75x) the circulating market cap of FTT at the time! As a result, on November 6, Binance CEO Changpeng Zhao (known as “CZ”) announced that his exchange would liquidate any remaining FTT on its books. The announcement initiated FTT’s price decline and prompted a bank run on the FTX exchange due to insolvency concerns. Such concerns turned out to be well grounded as FTX halted withdrawals two days later and, in an unexpected turn of events, announced that Binance had signed a non-binding letter of intent (LOI) to acquire (i.e., bailout) FTX International. At this point, the worst-case scenario was that Binance didn’t go through with the deal after conducting the due diligence. Once again, fears became a reality as Binance backed away from the LOI on November 9, citing “the latest news reports regarding mishandled customer funds and alleged US agency investigations.” That day, The Wall Street Journal reported that FTX’s liquidity shortfall amounted to $8 billion.

After failing to raise capital, on November 11, more than 130 entities tied to FTX.com, FTX US, and Alameda Research filed for Chapter 11 bankruptcy, with the Alameda petition listing assets and liabilities of at least $10 billion each. At the heart of FTX’s problem were losses at Alameda that most FTX employees did not know existed. According to a Reuters report, on November 6 – the day CZ announced Binance would liquidate its FTT position – “Bankman-Fried held a meeting with several executives to calculate how much outside funding he needed to cover FTX’s shortfall.” The heads of the company’s regulatory and legal teams who attended the meeting revealed to Reuters that FTX had moved around $10 billion in customer deposits to Alameda. US regulators, including the SEC, CFTC, and DOJ, are all investigating the matter. As if the collapse of FTX wasn’t bad enough, hours after the exchange filed for bankruptcy, more than $600 million were siphoned from FTX wallets in an alleged hack, with many users reporting $0 balances in their FTX.com and FTX US wallets. The hacker was likely an inexperienced insider, as they used the Kraken exchange to offload some of the stolen funds. Kraken’s Chief Security Officer confirmed that they know the attacker’s identity, though it hasn’t been publicly disclosed.

What to Expect?

The collapse of FTX/Alameda will have second and third-order effects on the broader crypto industry beyond the impact on prices. Below we highlight the most crucial areas to monitor in the coming weeks and months.

- Solana Ecosystem: the November 2 CoinDesk report showed that Alameda owned ~$1.2 billion of Solana’s native token SOL, representing about 10% of the cryptoasset’s circulating supply. Alameda also held various Solana ecosystem tokens such as SRM, MAPS, OXY, and FIDA. For context, Bankman-Fried and Alameda were early investors of Solana. The now-bankrupt trading firm sold off large amounts of SOL in a failed attempt to raise liquidity, triggering a liquidation cascade that prompted more sell-offs. Furthermore, data showed that validators were unstaking millions of SOL, representing a potential threat to the chain’s security. Fortunately, it was later discovered that most of the unstaking was merely operational, with 28.5 million SOL being re-staked as part of the Solana Foundation Delegations Program. The Solana ecosystem may experience difficult times as many of its dApps face stress tests in the coming weeks. However, our view is that Solana has outgrown FTX/Alameda, attracting a vibrant and loyal community of developers focused on its long-term success.

- Institutional Investors: FTX raised $1.8 billion over seven funding rounds from more than 80 investors, including Sequoia, Temasek, and Softbank, securing a $32 billion valuation in January of this year. In this regard, Sequoia has already marked down to zero the value of its FTX stake. Many of these investors are now under public scrutiny, with some arguing that they weren’t doing real diligence. The hard reality is that Bankman-Fried positioned himself as the face of the industry, and it’s likely that some institutional investors will be reluctant to enter the space in the coming months to avoid reputational risks. On the other hand, others will recognize that the failure of a centralized entity (intermediary) does not represent the failure of blockchain systems or decentralized protocols.

- Lenders: it is critical to consider systemic risk, that is, the risk that a debt-fuelled collapse in one part of the system spreads across connected protocols and firms. The implosion of FTX and Alameda will have ripple effects across different parties exposed to them. For instance, crypto lender BlockFi has already paused client withdrawals, arguing that they cannot operate as usual given the lack of clarity around the FTX bankruptcy. For reference, FTX signed a deal in July that gave it the option to buy BlockFi after providing it with a $250 million line of credit. In addition, bankrupt crypto lender Voyager Digital has reopened its bidding process, acknowledging it has $3 million locked up on FTX. In September, FTX paid $1.4 billion to win a bidding war to acquire Voyager’s assets. Other lenders in the space have also been affected. Genesis sold collateral, resulting in a loss of $7 million across counterparties, and acknowledged that its derivatives business has ~$175 million in locked funds in FTX. Finally, TrueFi has a $7.8 million unsecured loan exposure to Alameda. Importantly, we are still witnessing the effects of this credit-fuelled collapse working its way to the market, and it will likely take weeks to resolve fully.

- Centralized Exchanges: a positive outcome of the FTX debacle is that it will accelerate crypto self-regulation. Centralized exchanges and, more broadly, custodial service providers will have to gradually adopt a routine Proof of Reserve program to maintain customers’ trust. Per Nic Carter, “Proof of Reserves is the idea that custodial businesses holding cryptocurrency should create public facing attestations as to their reserves, matched up with a proof of user balances (liabilities).” After last week’s events, Binance, Crypto.com, OKX, Kucoin, Huobi, and Poloniex have either published or announced plans to undergo periodic Proof of Reserves. Notably, Kraken has thus far set the standard for best practices on this front. The exchange undergoes a semi-annual cryptographic accounting procedure by external auditors. Kraken’s Merkle approach allows clients to independently verify that their balance was included in the Proof of Reserves audit.

- Regulation: the area with the most uncertainty is the regulatory response that the FTX collapse will bring about. Bankman-Fried had been publicly lobbying in Washington since last year, meeting with notable regulators such as CFTC Commissioner Caroline Pham. On October 19, Bankman-Fried posted his “Possible Digital Asset Industry Standards” (DCCPA). He described the document as “a set of standards that we as an industry could enact to create clarity and protect customers while waiting for full federal regulatory regimes.” In reality, the DCCPA was widely criticized by DeFi advocates as it threatened DeFi’s status as a censorship-resistant and open financial system. This week’s fallout likely killed the DCCPA, but what other legislative (re)actions will it bring about? First, regulators must understand that FTX and Alameda were opaque and trust-based centralized entities, which allowed them to act beneath the surface. In DeFi, self-enforcing smart contracts on top of a public blockchain allow for a more transparent and sustainable system. DeFi should not suffer the consequences of CeFi’s wrongdoings. In addition, it’s time for US regulators to quit stalling and provide clear regulatory guidelines. Coinbase CEO Brian Armstrong could not have been clearer: “the SEC failed to create regulatory clarity here in the US, so many American investors (and 95% of trading activity) went offshore.“

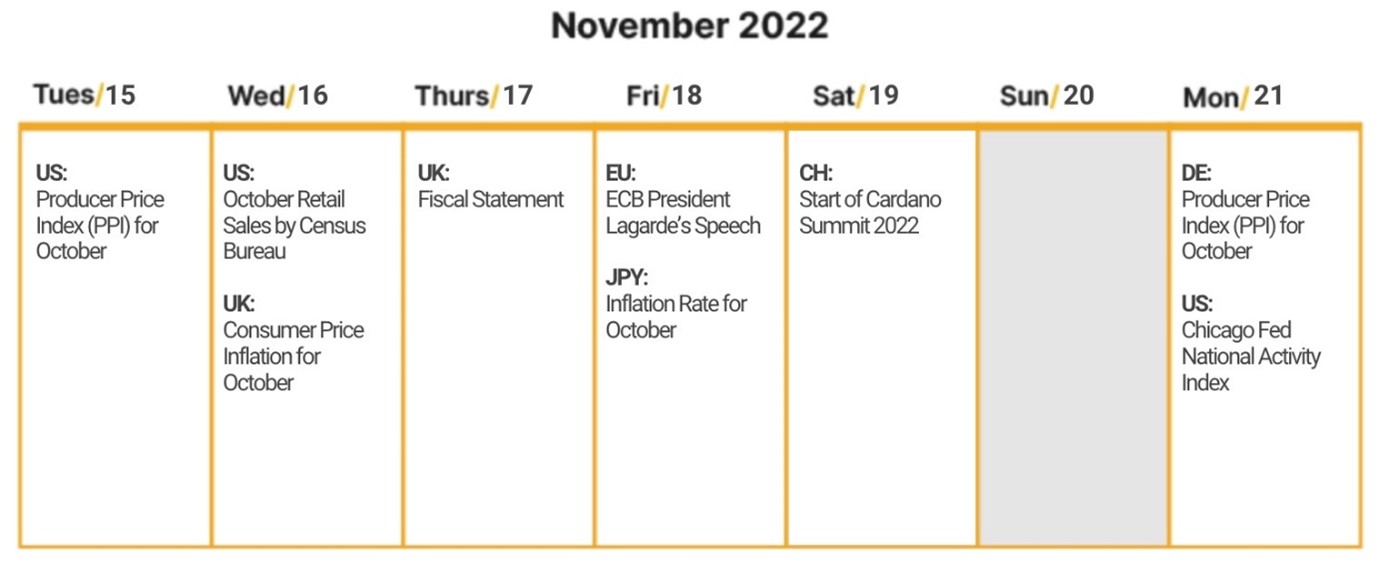

Next Week’s Calendar