When your rent jumps, your debt repayments rise and your weekly grocery bill creeps up, it can feel like you’re constantly on the defence and playing catch up. But here’s the shift: it’s a reminder that your money needs to work harder for you.

As prices rise, the spending power of your cash falls. If you leave $5,000 in a bank account earning 3% interest while inflation runs at 3.8%, you’re effectively losing money. Investing is how you give your money a chance to keep up with inflation. Investing is how your money grows, compounds, and to work just as hard as you do.

When you’re starting out on your journey as an investor, it pays to be prepared. We all tend to make the same mistakes at first, so it is worth being aware of them.

Here are three common mistakes new investors make and how to avoid them.

1. Paying too much in fees

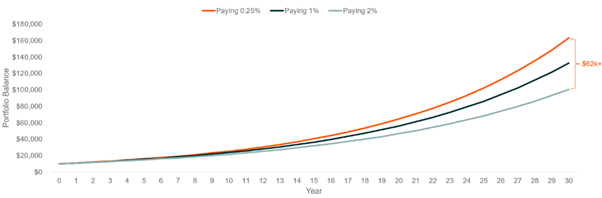

When you’re starting with a smaller balance, fees matter more than you think.

For example, investing $10,000 into an ETF with a 2% management fee instead of a similar ETF at 0.25% means you’re paying an extra $175 every year at the start - but over 30 years with an average 10% return per annum, the amount compounds to over $62,000.

Source: Management fee data by Global X ETFs based on theoretical portfolio of $10,000 invested over 30 years with 10% p.a. gross returns.

How to avoid it:

Compare brokers and ETF fees before you start. A difference of 0.20% or 0.30% is small day to day but huge over a decade. Choose low cost diversified ETFs like A300, which gives you ownership of 300 Australian stocks for a low fee of 0.04%. Oh, and another hot tip: avoid trading more often than necessary.

2. Checking your portfolio too often

Say you invest $1,000, and two weeks later it’s down to $960. That drop feels personal even though it’s a normal market movement. Many new investors respond by selling at the worst time or buying again when the price rebounds, locking in losses.

Remember: investing is a long-term discipline. Investing isn’t meant to be monitored daily, markets fluctuate and compounding takes time. The goal isn’t to avoid every dip, it’s to give your money enough time to recover and grow.

How to avoid it:

Review your portfolio once a quarter, not every day. It helps you avoid emotional decisions and stay focused on long term outcomes.

3. Not knowing your ‘why’

Without a clear goal, it’s easy to jump into whatever’s popular. One month it’s AI stocks, the next it’s silver, the next it’s something a friend mentioned at a barbecue.

How to avoid it:

Write down your goal before you invest. For example:

- I want $20,000 for a home deposit in 3-5 years.

- I’m building long term wealth for retirement.

- I want to starting putting away $200 a week until my child turns 18.

Your goal determines how much risk you can take, how long you can stay invested, and what products suit you.

So the next time you feel like losing it at the supermarket, remember that you have a choice. While inflation is reducing your purchasing power, investing is how you take some of that power back. Steadily, calmly, and with a plan.