After a nearly two-year pause, the Initial Public Offering (IPO) markets have come to life in the second half of 2023, helped by a robust Artificial Intelligence (AI) rally, moderating inflation, and stability in interest rate policy. September included three of the most anticipated listings in Arm Holdings, Instacart, and Klaviyo, and we are bullish on the market opportunity in front of these companies and the themes that they represent. They can provide valuable insights into emerging trends and sub-themes within the Semiconductor, AI, and Software-as-a-Service (SaaS) sectors, which we explore in this piece. Market volatility is likely to persist in the near term, but the success of these listings suggests a continued resurgence in IPO activity heading into 2024.

Key Takeaways

- The IPO landscape turned positive in recent months. In September alone, companies listed on U.S. exchanges raised $7.2 billion, the biggest IPO fundraising month since the end of 2021.2 Also, on the year, of the 16 companies that raised over $300 million on U.S. exchanges, only four currently trade below their IPO price.3

- Profitability and strong unit economics prior to going public are key for the success of upcoming listings, given the reality of higher rates and tighter liquidity. Critical for consumer-first businesses is revenue diversification through channels such as advertising.

- We believe that the companies that can meet these investor demands and the companies that provide legitimate exposure to the rapidly evolving AI ecosystem are likely to emerge as the next wave of IPO winners.

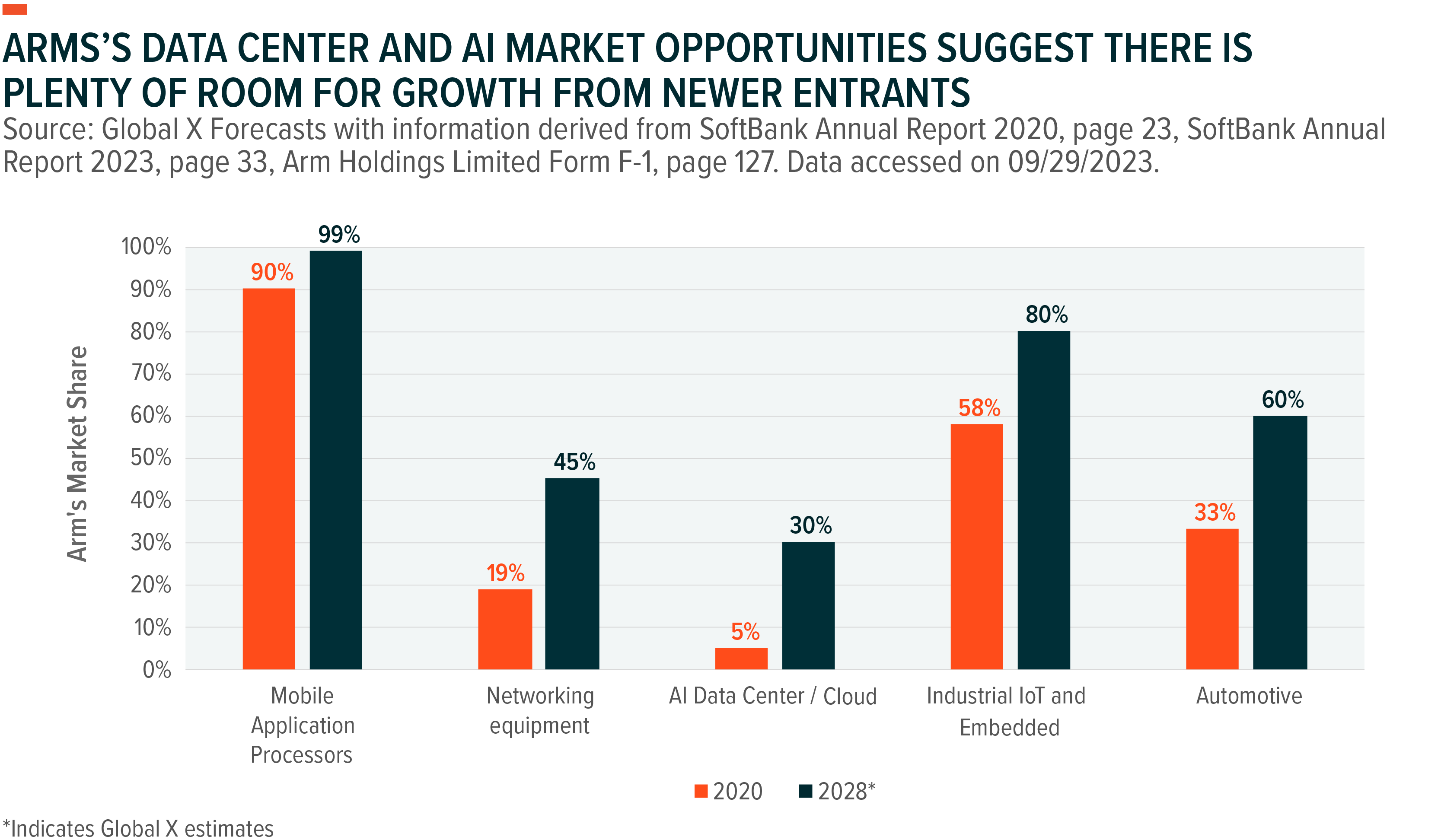

The Arm IPO Underscores the Red-Hot Demand in the AI Chip Market

Arm Holdings, the chip design company controlled by SoftBank, was the most widely anticipated technology IPO of the year and marked the largest IPO since electric truck maker Rivian in 2021.4 The company is capitalising on the enthusiasm surrounding new AI technologies at the right time, which helped it land a nearly $60 billion valuation upon debut, putting it among the upper echelon of semiconductor firms.5

Arm is primarily known for its near monopoly in mobile and internet of things (IoT) application processors, but the company is strategically positioning to become a pivotal player in the burgeoning semiconductor value chain for AI computing, alongside the likes of Nvidia and AMD. Semiconductor companies developing high-performance chips that cater to the unique computational demands of AI workloads are well positioned, especially if they offer high levels of profitability and have previously demonstrated leadership across other verticals within the semiconductor landscape. By the end of the decade, annual spending on AI chips is projected to grow at a compound annual growth rate (CAGR) of over 30% to nearly $165 billion.6

As graphics processing units (GPUs) start to take precedence over central processing units (CPUs), Arm-based chips are expected to gain prominence alongside the GPU as a low-cost alternative to traditional CPU set ups. Arm’s chip designs are expected to be in demand and potentially worth $250 billion by 2025.7

Arm monetises through a mix of licensing and royalty-based revenue models, which results in high margins and profitability, partially justifying the company’s premium valuation. And the success of the business could pave the way for several emerging AI-focused chip companies to consider tapping the public markets in the near future.

Instacart Paves the Way with Advertising-Led Monetisation

Grocery delivery giant Instacart, which was valued at $39 billion in 2021, came to the public market at a much more reasonable $10 billion valuation, even after pricing its shares at the top end of its expected range of $28-$30.8 Growth in the company’s core delivery services business cooled off quite significantly in 2023, in line with the broader digital commerce industry.

Investors were more pleased by the company’s rapid diversification of revenues however, which helped significantly in pushing the IPO through. Instacart expanded its ad network to include over 5,500 brands, while growing its ad revenue from $295 million in 2020 to $740 million in 2022 (29% of total revenue).9 Broadly speaking, digital marketplaces have effectively embraced advertising-driven monetisation, and we expect this approach to become the industry norm for marketplaces moving forward. Instacart’s focus on profitability also paid dividends in its IPO process. The company managed to grow net income to a robust $114 million in Q2 2023 from only $8 million in Q2 2022. Its operating margins were roughly 15% and its profit margins roughly 16%.10

Instacart’s success can help improve sentiment around the broader digital commerce theme, helping to make the investment case for other marketplaces charting their way to profits via ads. Moreover, warm market reception may also compel other late-stage consumer-based internet players such as Fanatics, Klarna, or Reddit to consider a listing soon.11

Klaviyo Leads with Profits, Re-writing SaaS Playbook

Valuations tumbled across the SaaS landscape over the last few quarters, forcing late-stage private companies considering going public to do so at public-market multiples far below their peak private market tags. Marketing automation firm Klaviyo stands out as a company that smoothly transitioned from the private to public market without incurring a substantial decrease to its record valuation. The company secured a $9.2 billion valuation in its September IPO after pricing its share sale above its indicated range, which is close to the $9.5 billion post-money valuation it earned during its May 2021 fundraising round. 12 13

In addition to partnerships with market leading platforms like Shopify, Klaviyo also stood out from recent SaaS IPOs by demonstrating profitability in the first half of 2023. The company reported net income of $15.2 million in H1 2023, compared to a loss of $24.6 million in H1 2022.14 In the coming tech IPO cycle, we expect established brands boasting profitability and solid unit economics prior to going public to emerge as the winners, despite sacrificing potential growth, as investor appetite has shifted from growth to value in recent quarters due to unfavourable market conditions.

We expect SaaS IPO hopefuls to prioritise getting profitability in check before tapping the public markets, as the Klaviyo listing is further proof that the IPO window remains open for high quality companies.

Conclusion: Emerging Opportunities for IPO Hopefuls

Momentum for the new issuance market can continue through year-end and into 2024 even if market conditions remain less than ideal in the coming quarters. This expectation is also bolstered by the fact that many companies have not raised private capital in 1-2 years and are reaching a pivotal point where they must raise additional funding and/or provide liquidity for their employees. We expect many IPO candidates to push forward with listings, especially those boasting strong fundamentals, given the shift in investor preferences towards profitability overgrowth. Also, the continued proliferation of AI opens new doors for companies capable of meeting the growing demand for AI and AI-related technologies.