The global space industry is moving from episodic innovation to commercial scale. Falling launch costs, improving rocket reusability, and rising demand for satellite-enabled connectivity and data are changing the economics of space. Once a prestige domain defined by government-led missions, space is now an infrastructure layer for modern communications, geospatial intelligence, defence systems, and emerging compute applications.1

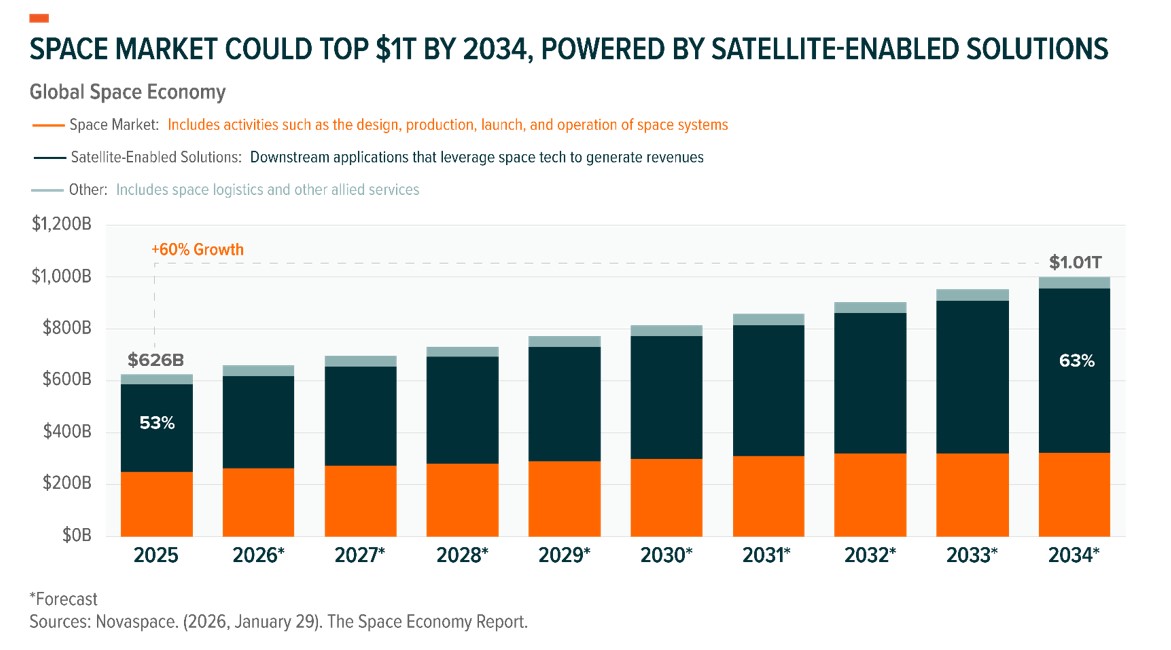

By 2034, the global space market could surpass US$1 trillion in annual revenues, up from US$626 billion in 2025, with substantial downstream value tied to services built on top of expanding space-based infrastructure. Segments such as launch services, satellite connectivity, and data services could grow roughly three times faster than the broader space market, with a small group of innovators well positioned to potentially capture a disproportionate share.2

The Global X Space Tech ETF (ASX: MOON) offers targeted access to this evolution. It tracks companies across the space tech value chain, spanning reusable rockets and launch systems, satellite connectivity, space exploration, and the businesses commercialising space-enabled services.

Key Takeaways

- The commercial era of space has arrived: reusable launch systems have collapsed the cost of accessing orbit and unlocked business models that were not economically viable a decade ago.

- The space market is on track to surpass US$1 trillion in revenues by 2034, with launch, satellite connectivity, and data intelligence segments growing roughly three times faster than the broader market.

- MOON provides pure-play exposure to the space technology value chain, including launch systems, satellites, and the space-enabled services built on top of orbital infrastructure.

Space Is Entering Its Commercial Phase

Space represents an unexplored economic frontier. Much like railroads in the 19th century, the internet in the 1990s, and AI in the 2020s, space infrastructure could define the 2030s as a foundation for the next phase of the global economy

For most of the modern space age, access to orbit was the exclusive domain of nation-states with vast budgets and long development timelines. That changed in the 2010s as private capital entered the launch market and commercial satellite operators demonstrated viable business models. Commercial activity now accounts for roughly 70% of global orbital launches, up from just 25% a decade ago.3

Two groups of companies are pushing the industry into commercialisation at scale. One is transforming launch services, turning access to space from bespoke aerospace engineering into repeatable logistics, led by SpaceX, Rocket Lab, and a growing field of new entrants such as Blue Origin and Firefly Aerospace. The other is monetising that infrastructure through satellites and the downstream applications built on top of them, with operators such as Starlink, Iridium, Planet Labs, and EchoStar building recurring-revenue service layers on top of constellation assets. Satellite-enabled solutions could account for roughly 63% of total space revenues by 2034, reflecting higher constellation density and the rollout of new service layers such as broadband internet.4

New Launch Economics Changed the Space Industry's DNA

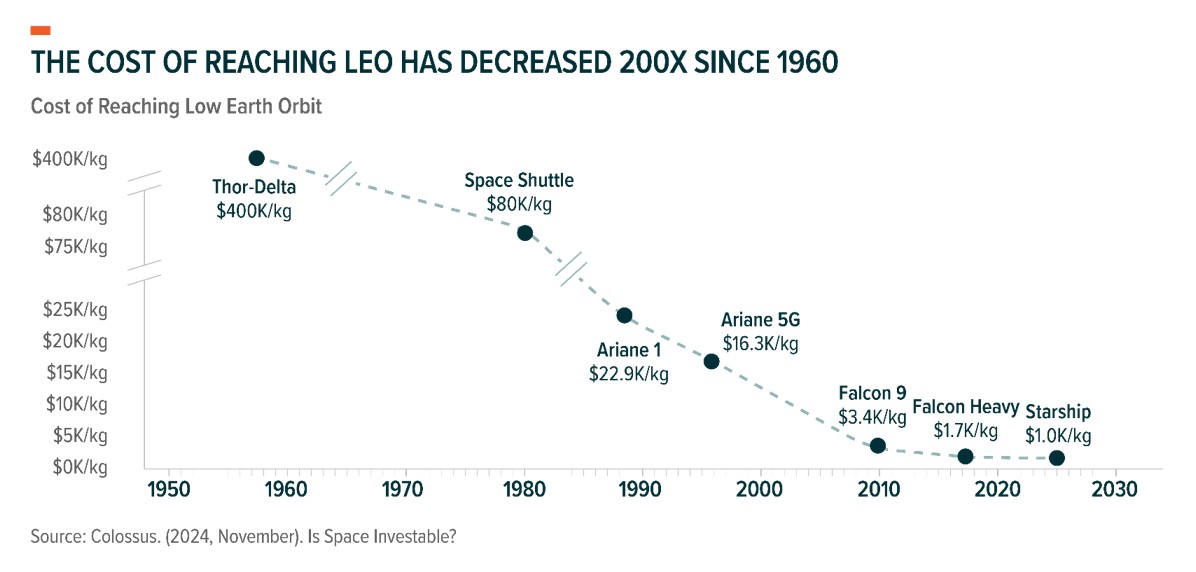

The single biggest structural change in space tech over the past two decades is the collapse in cost of payload delivery to Low Earth Orbit (LEO), the altitude ranges up to 2,000 kilometres where most commercial satellites operate. NASA's Space Shuttle, which flew its last mission in 2011, cost US$54,500 per kilogram to LEO. SpaceX's Falcon 9, the workhorse of the modern launch market, now costs roughly US$2,720 per kilogram, with pricing listed at US$74 million per launch and payload capacity to LEO of up to 22,000 kilograms in expendable configuration.5

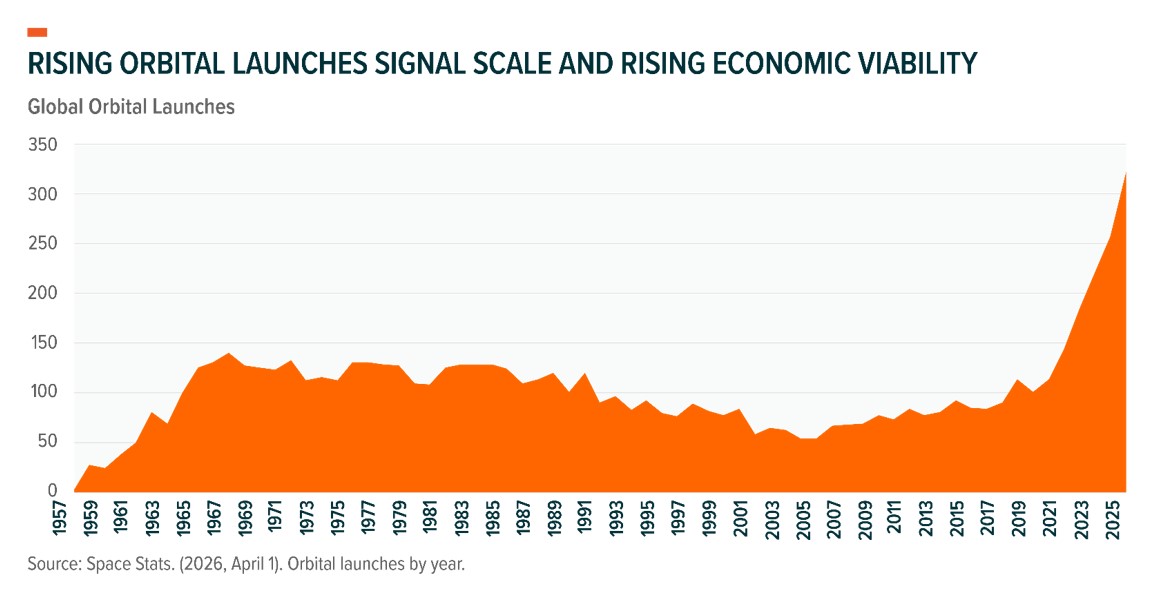

Reusability is what changed the economics. Recovering and re-flying first-stage boosters turns launch from a one-time expenditure into a repeatable operating model. With a 97% success rate on reused boosters and fairing halves, SpaceX has substantially reduced hardware amortisation costs and set a new pricing standard across the industry. Global orbital launch attempts jumped to roughly 325 in 2025, up from 85 in 2016, with the US alone accounting for nearly 179 successful launches, or about 52% of global activity.6

Rising launch cadence is reshaping the industry's planning cycle by enabling satellite operators to replenish constellations faster, governments to build more resilient architectures, and suppliers to serve a market with more predictable deployment schedules. The commercial launch market itself, the upstream segment that delivers payloads to orbit, is projected to grow to nearly US$70 billion by 2035 at a 13.4% CAGR from 2025, driven by broadband constellation deployment and the buildout of defence architectures that require tactically responsive access to orbit. Launch is only the entry point. The bulk of the US$600 billion to US$1 trillion total space economy sits downstream in satellite services, applications, and ground infrastructure, where recurring revenue and value accrual concentrate.7

The launch market is also broadening beyond SpaceX. Rocket Lab's Electron has established a niche in dedicated small satellite launches, where schedule control and mission specificity matter more than the lowest possible cost per kilogram. As of March 2026, Rocket Lab had completed nearly 85 launches and accounted for roughly 8% of Federal Aviation Administration (FAA)-licensed launches in 2025. The deepening of the launch ecosystem supports more business models across the broader space stack.8

Constellations Turn Orbit into Investable Infrastructure

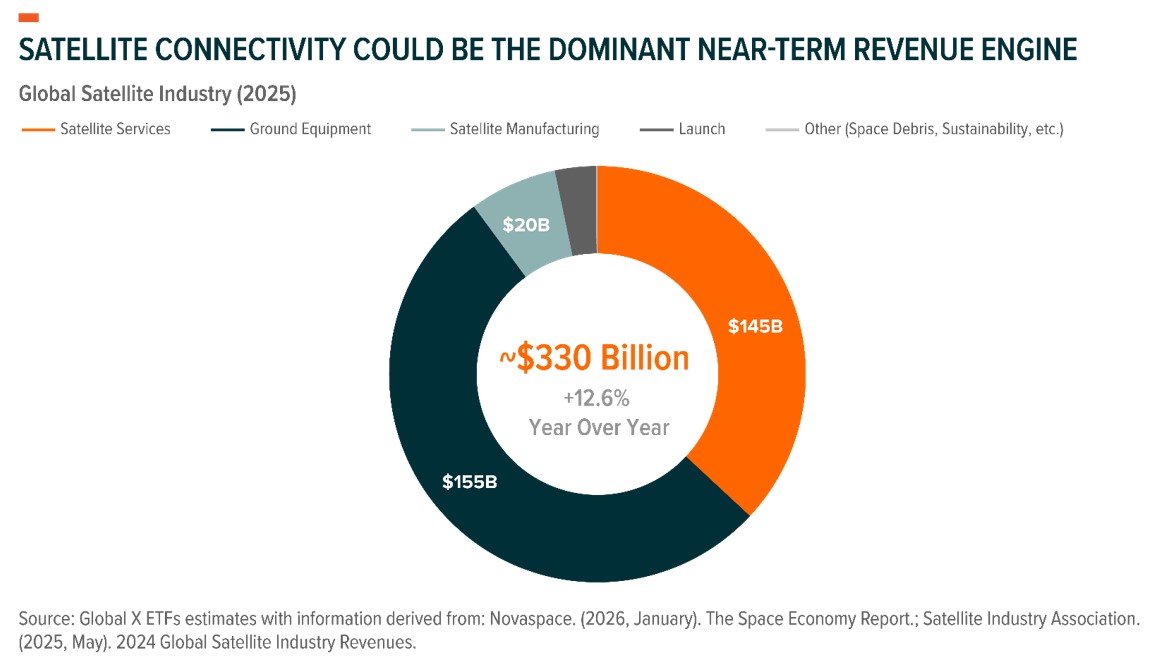

If launch is the enabler, satellites are the monetisation layer. Over 50% of today's space market is tied to satellites, spanning infrastructure, connectivity, and downstream applications. The opportunity is now shifting from individual satellites to dense LEO networks delivering broadband, navigation, Earth observation, and secure communications, transforming orbit from a collection of one-off assets into a persistent infrastructure layer.9

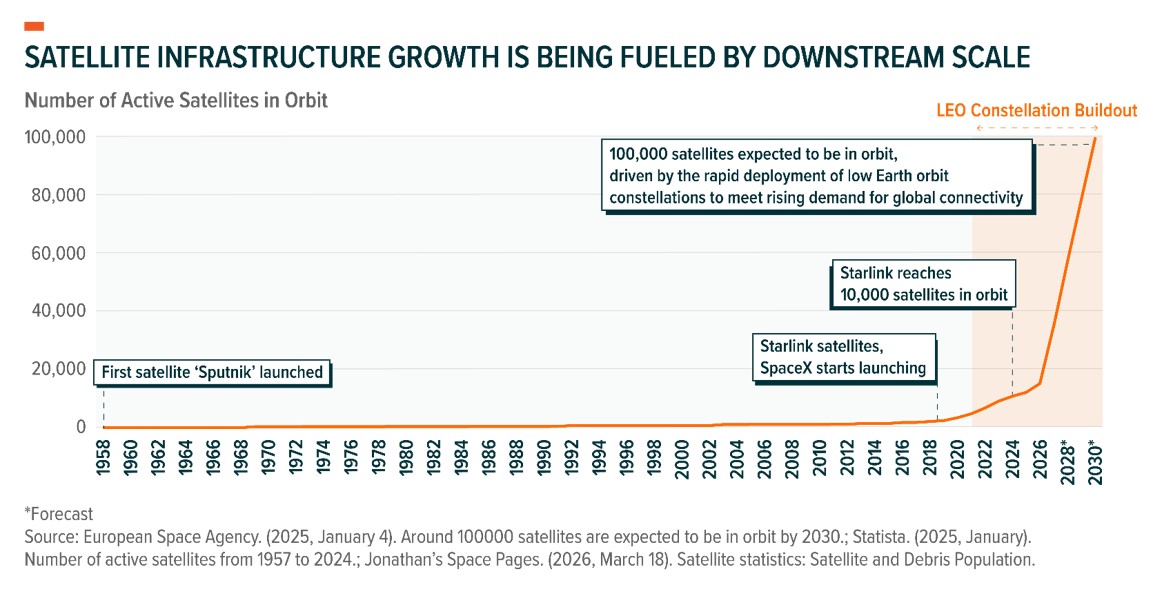

The installed base is rising quickly. Active satellites in orbit have grown from nearly 1,000 in 2010 to more than 12,000 in 2025 and could approach 100,000 by 2030 as operators such as Starlink and Amazon Leo (formerly Project Kuiper) continue scaling LEO satellite broadband. SpaceX's Starlink reached 10,000 satellites in orbit in 2025, supporting roughly 9.25 million active internet customers across 155 regions by early 2026.10

As networks like Starlink scale, satellite infrastructure begins to resemble a recurring-revenue service model rather than a project-based aerospace business with irregular cash flows. This transformation is one of the most important changes underway in space today and central to its investment case. By 2035, the satellite broadband market is projected to grow at a 16% CAGR to US$100 billion, up from an estimated US$22 billion in 2025, driven by household connectivity, enterprise backhaul, mobility, emergency response, and military use cases. Beyond broadband, the satellite services market extends into a downstream application layer covering climate monitoring, logistics visibility, precision agriculture, and defence intelligence, a roughly US$145 billion market still in its early stages relative to what is possible as constellation density rises.11

Defence and Orbital Compute Anchor the Long-Duration Case

Governments worldwide spent US$137 billion on space in 2025, of which roughly US$73 billion was defence-related, accounting for about 2% of total global military spending. In the US, investment is accelerating sharply with space recognised as a primary national security initiative. The US Space Force's fiscal 2027 budget request of nearly US$71 billion is double its fiscal 2025 budget, with proposed programs like the Golden Dome missile defence initiative reportedly requiring up to US$185 billion to complete.12

Space is increasingly central to missile warning, intelligence, surveillance, reconnaissance, and the broader architecture of resilient national defence. Assured access to orbit, space-based sensing, and the ability to rapidly reconstitute satellite capabilities in contested environments are strategic imperatives for modern military planning. The predictability of defence spending can also help stabilise the space tech market during periods when commercial capital becomes more selective.

Further out, space-based data centres and other power-intensive computing workloads represent a longer-duration optionality embedded in the space technology value chain that is beginning to attract significant capital and engineering attention. The economics remain challenging, as launch costs still need to fall below roughly US$200 per kilogram to LEO for orbital compute to be competitive with terrestrial alternatives. But the directional logic is compelling: orbital environments offer abundant solar energy and ease cooling and water use constraints, while bypassing many of the regulatory, permitting, land-use, and power procurement bottlenecks on Earth.13

MOON: A More Targeted Solution to Access the Space Tech Opportunity

The Global X Space Tech ETF (ASX: MOON) provides focused exposure to companies building and enabling the commercialisation of space, tracking the Mirae Asset Space Tech Index across four segments of the value chain:

- Rocket Launch and Reusable Rockets: launch systems and reusability technologies that reduce the cost of access to space

- Space Tech & Components: mission-critical hardware, propulsion, software, analytics, and specialised components supporting modern space operations

- Satellite Telecommunications & Data Services: connectivity, navigation, imaging, and secure communications through satellite systems and related infrastructure

- Space Transportation, Tourism, and Exploration: human spaceflight, orbital access, and related exploration services

To be eligible, companies must derive at least 50% of revenues from space tech-related activities, keeping the portfolio centred on businesses where space is a core driver of fundamentals rather than a peripheral line item. The index uses a modified market-cap weighted methodology that maintains exposure to established leaders while capturing smaller, high-growth companies shaping the next phase of the market.