The global economy is entering the next phase of the AI cycle, where intelligence extends beyond software and into the physical world. While the past decade has been defined by digital platforms and compute, the next phase is centred on applying that intelligence to real-world tasks through robotics1. Humanoid robots are designed to operate within human environments, enabling automation across a far broader set of use cases than traditional industrial systems. This shift is not incremental as it reflects a transition from automating processes to replicating human capability. As labour constraints intensify, productivity growth remains constrained, and capital continues to flow into AI, the convergence of robotics and artificial intelligence is beginning to unlock a new multi-year investment cycle that extends well beyond the factory floor2.

Key Takeaways

- Humanoid robotics is emerging as a new industrial platform, as AI extends into the physical economy and unlocks a multi-trillion-dollar market opportunity

- Adoption is being driven by labour shortages, accelerating AI capability, and increasing policy and capital support, though real-world deployment remains in early stages

- The investment opportunity spans the full humanoid robotics value chain, which is how the Global X Humanoid Robotics ETF captures exposure across AI, components, and enabling technologies

A New Industrial Platform: From Automation to Labour Substitution

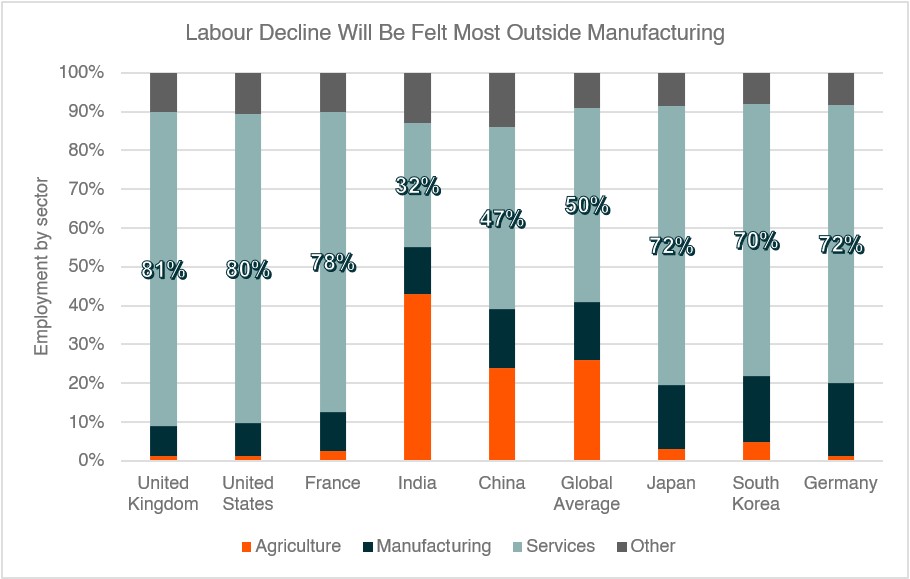

Humanoid robotics represents a structural expansion in the scope of automation. Traditional industrial robots have been highly effective within controlled, repetitive environments, particularly across manufacturing and assembly lines. However, the majority of global labour exists outside these structured settings, across logistics, services, healthcare, construction, and a wide range of semi-structured or unstructured environments3. The limitation has not been demand, but capability.

Humanoid robots address this constraint directly by adapting the machine to the human environment, rather than redesigning the environment for the machine. This shift significantly expands the addressable market for automation, effectively moving from process automation toward the digitisation of human labour itself. The implication is a step-change in total addressable market, with robotics no longer confined to industrial capex cycles but increasingly tied to broader labour substitution and productivity dynamics across the global economy.

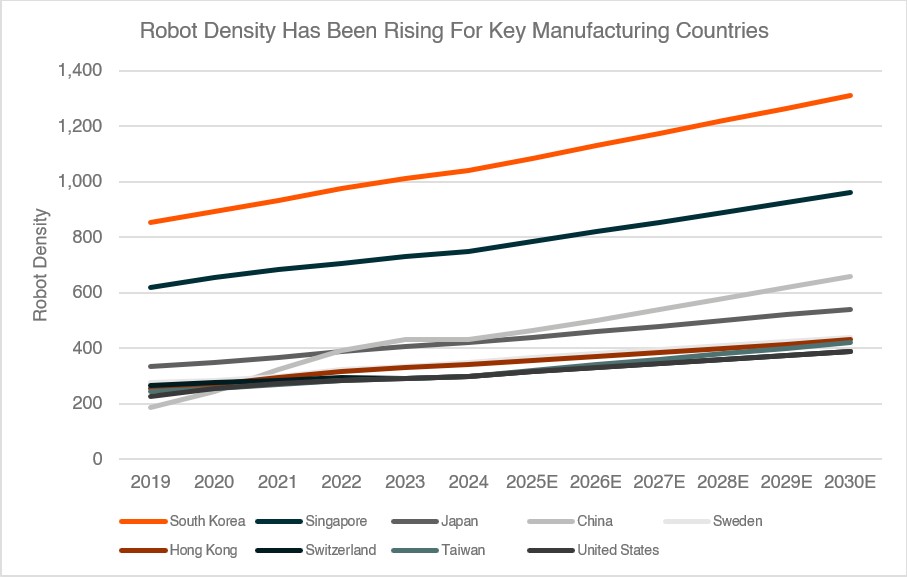

Source: International Federation of Robotics

Robot density = Automated robotics per 10,000 manufacuring workers

Source: World Bank, ILOSTAT, OECD, US Bureau of Labor Statistics, China National Bureau of Statistics

At the same time, this transition is being supported by the emergence of physical AI. Advances in perception, reasoning, and control are enabling machines to interact with dynamic environments in ways that were not previously possible. Robotics is no longer purely a hardware problem. It is becoming an integrated system of software, data, and hardware, where performance improves over time through iteration and learning rather than static engineering design.

Why Now: Convergence of Technology, Labour and Policy

The acceleration in humanoid robotics is not driven by a single factor, but by the convergence of multiple structural forces that are reinforcing each other.

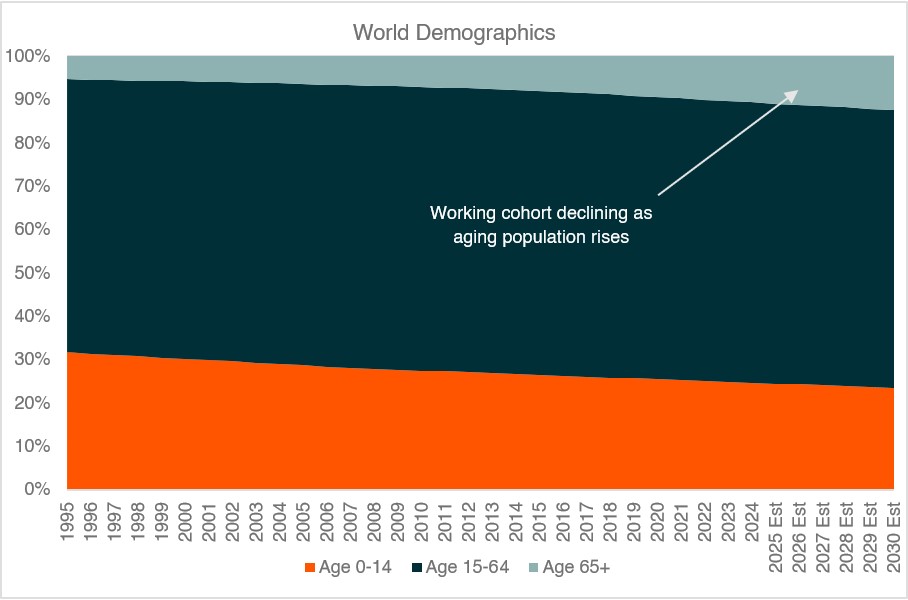

Labour dynamics are central to the investment case. Ageing populations and slowing workforce growth across developed economies are creating persistent shortages in physically intensive and repetitive roles4. At the same time, wage inflation and the need to maintain productivity are increasing the economic incentive to automate. In many industries, the cost of labour is no longer declining in real terms, making the relative economics of automation increasingly attractive over time.

Source: WHO, United Nations

Technological capability is also reaching a meaningful inflection point. The integration of AI into robotics is enabling machines to perform more generalised tasks rather than highly specific functions. This includes advances in vision-language-action models, improved simulation environments, and the growing availability of training data5. These developments are critical in enabling robots to operate in real-world environments, where variability and uncertainty have historically limited deployment.

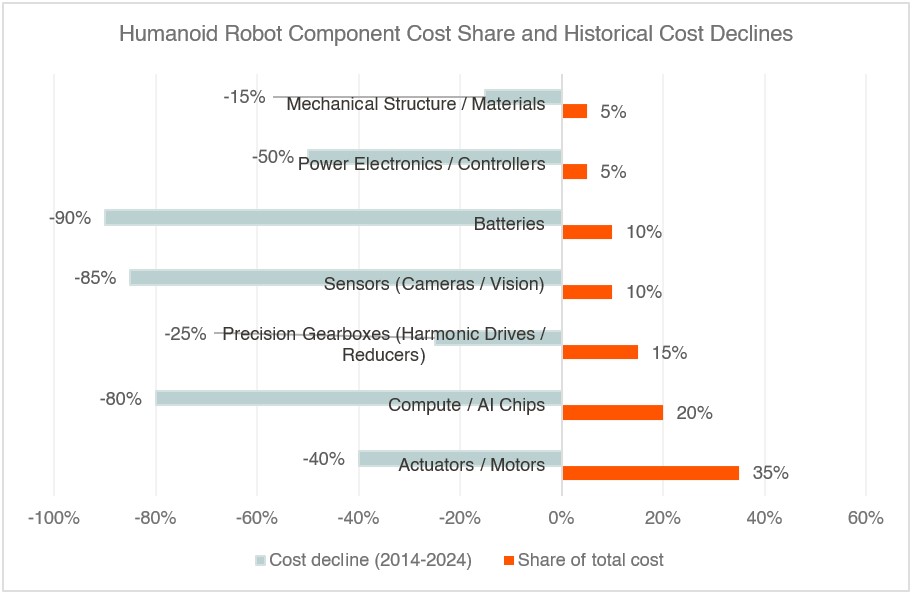

At the same time, hardware cost curves are beginning to benefit from adjacent industries. Supply chains developed for electric vehicles and consumer electronics are reducing the cost of key components such as motors, sensors, and batteries, improving the economic viability of humanoid systems over time. This mirrors previous technology adoption cycles, where cost declines have acted as a key catalyst for scaling.

Source: Robozaps.com, CSET

Policy and capital are reinforcing these trends. Governments are increasingly prioritising automation, domestic manufacturing capability, and technological leadership as part of broader industrial strategy. This is particularly evident in China, where robotics and embodied intelligence have been identified as strategic sectors, supported by both funding and industrial policy. In parallel, private capital continues to flow into AI and robotics as investors seek the next phase of growth beyond digital platforms6.

From Early Deployment to Scaled Economic Adoption

Humanoid robotics is progressing from early-stage deployment toward a phase defined by economic viability and scalable adoption. The initial phase of development has been centred on demonstrating capability, but the next stage is increasingly focused on delivering consistent, repeatable performance at a cost that supports broader commercial use across industries.

This shift is being driven by simultaneous improvements across both capability and cost. Advances in artificial intelligence, particularly in perception, reasoning and control, are enabling robots to operate more effectively in real-world, unstructured environments. At the same time, the underlying hardware stack is benefiting from scale and maturity in adjacent industries. Components such as actuators, sensors, batteries and semiconductors are seeing declining costs and improving performance, supported by supply chains developed through electric vehicles, consumer electronics and industrial automation.

As a result, the investment case is moving beyond technical feasibility toward economic competitiveness. The key inflection point is not whether humanoid robots can perform individual tasks, but whether they can do so reliably, safely and at a cost that is competitive with human labour. As cost per productive hour declines and utilisation increases, the economic case for deployment strengthens, particularly in sectors where labour constraints are most acute.

Adoption is therefore expected to follow a staged but accelerating path. Early deployment is concentrated in environments where tasks are repetitive, labour availability is limited and the return on automation is most immediate. Over time, as system capability improves and costs continue to decline, the range of viable use cases expands, supporting broader adoption across the global economy.

This progression is consistent with prior technology cycles, where initial deployment is followed by a period of rapid scaling once economic thresholds are reached. In this context, the current stage of development does not constrain the opportunity. It defines a multi-year pathway in which improvements in cost, capability and scale collectively drive sustained growth across the humanoid robotics ecosystem.

Capturing the Opportunity: A Full Value Chain Approach

The humanoid robotics opportunity is not limited to companies building end-products. In practice, value is distributed across a broad ecosystem of enablers that support the development, deployment, and scaling of robotic systems.

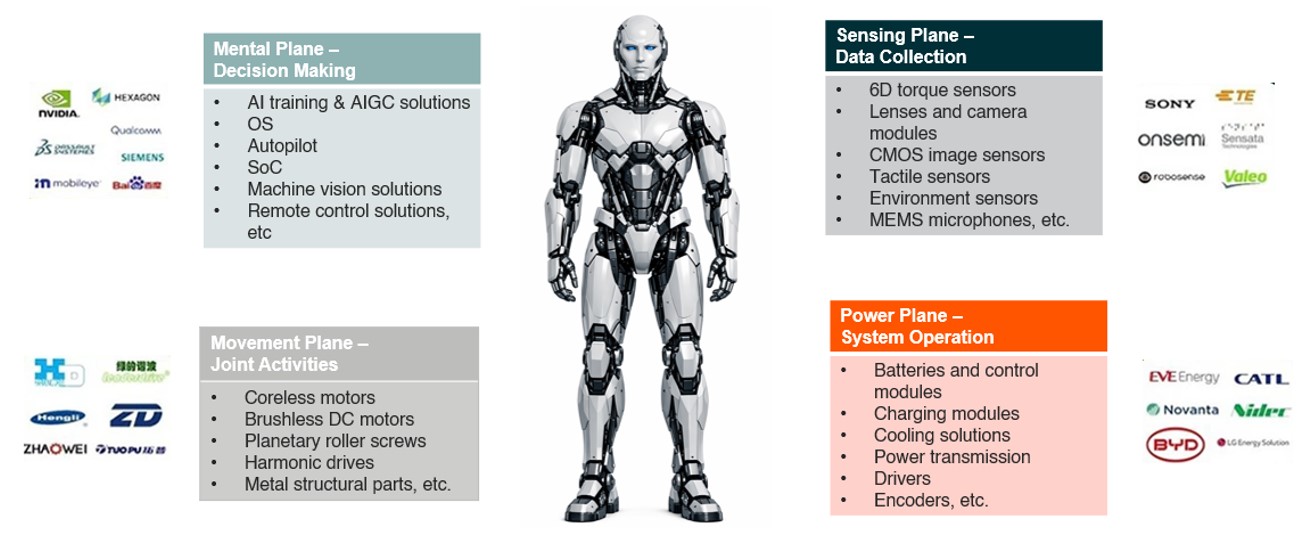

Artificial intelligence and compute providers play a central role, enabling perception, decision-making, and control. Semiconductor companies supply the processing power required for real-time operation, while sensor manufacturers provide the inputs necessary for robots to interpret their environment. Mechanical and electronic components, including actuators, motors, and precision systems, are critical in enabling movement, dexterity, and interaction7.

Source: TrendForce

In many cases, these components scale with complexity. A humanoid robot, for example, requires significantly more precision components and degrees of freedom than simpler robotic systems, increasing the content per unit as capability improves. This creates a structural tailwind for component suppliers, where demand grows not only with unit volumes but also with increasing system sophistication.

The Global X Humanoid Robotics EFT will track the Solactive Global Humanoid Robotics Index and is designed to capture this full ecosystem. It includes companies across humanoid and service robotics, industrial and autonomous systems, assistive technologies, and the underlying AI and hardware stack that powers next-generation robotics. Importantly, selection is based on measurable exposure to the theme, ensuring that constituents derive a meaningful portion of their revenues from relevant activities, while a capped, diversified approach avoids excessive concentration.

By taking a value chain approach, the strategy avoids relying on a narrow set of early-stage manufacturers and instead provides exposure to the broader infrastructure required for humanoid robotics to scale globally.