Artificial intelligence is often framed as a story about software, algorithms and increasingly powerful semiconductors. That framing made sense in the early stages of the AI cycle, when attention centred on model breakthroughs and the computing power required to train them. As AI moves from experimentation into industrial-scale deployment, the conversation is beginning to broaden. The systems supporting this technology are becoming larger, more energy intensive and more physical, spanning data centres, power infrastructure, cooling systems and advanced manufacturing equipment.

This shift is bringing a different layer of the technology stack into focus. Rare earth elements, once viewed as niche industrial inputs, are embedded across many of the machines that power modern computing, from semiconductor manufacturing tools to high-precision motors used across data centre infrastructure. As artificial intelligence scales from a software breakthrough into a global industrial system, the materials inside that hardware are becoming increasingly important.

In other words, the future of artificial intelligence is being shaped not only by code, but by chemistry.

Key Takeaways

- Rare earth elements are increasingly embedded across AI hardware and semiconductor manufacturing systems.

- China’s dominance in refining and magnet production is turning rare earths into a strategic supply chain vulnerability.

- As AI infrastructure expands, the demand for specialised materials is pulling the entire critical minerals stack higher.

AI hardware depends on materials few investors discuss

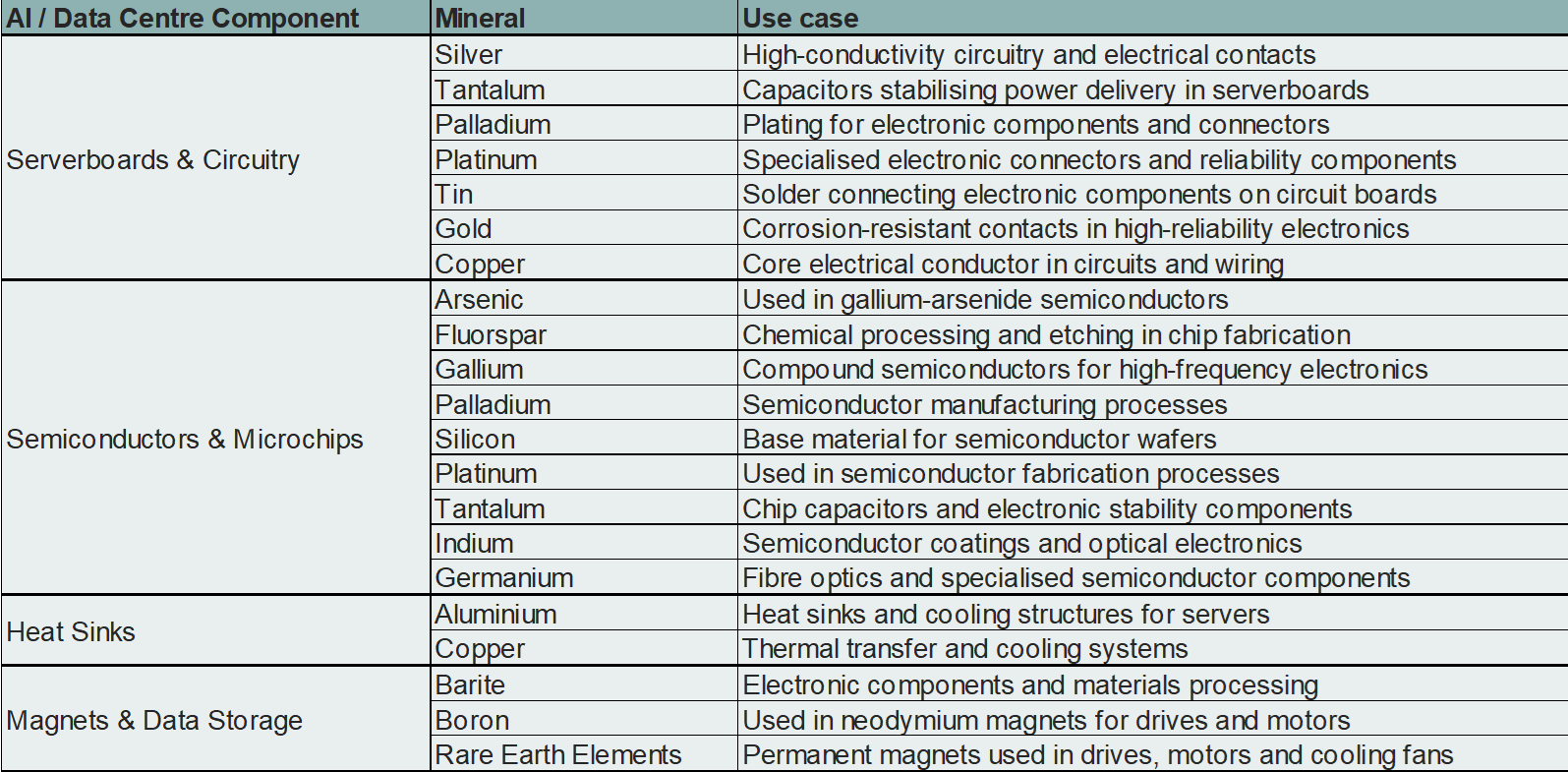

When investors think about AI hardware, the focus usually lands on GPUs, advanced semiconductors, and the companies designing them. But every layer of the semiconductor manufacturing process relies on extremely precise physical systems, many of which depend on rare earth materials1.

Permanent magnets made with neodymium, praseodymium, dysprosium and terbium are used across high-precision motors that control wafer handling, lithography equipment, ion implantation systems and vacuum pumps. These magnets provide extremely stable magnetic fields and motion control, allowing chip manufacturing equipment to operate with the accuracy required for advanced node production2.

The importance of these materials extends beyond chip fabrication. Rare earth magnets are also used in cooling systems, robotics, electric motors and power infrastructure that increasingly sit inside modern data centres. As AI workloads expand and facilities become more power-dense, the amount of specialised hardware embedded in these systems continues to grow3.

What this means in practice is that AI hardware is not simply a silicon story. It is also about other materials as well. The further AI scales into real-world deployment, the more the industry begins to depend on a broader stack of industrial inputs that historically sat far away from the technology sector.

Source: USGS, IEA, US Department of Energy, Semiconductor Industry Association

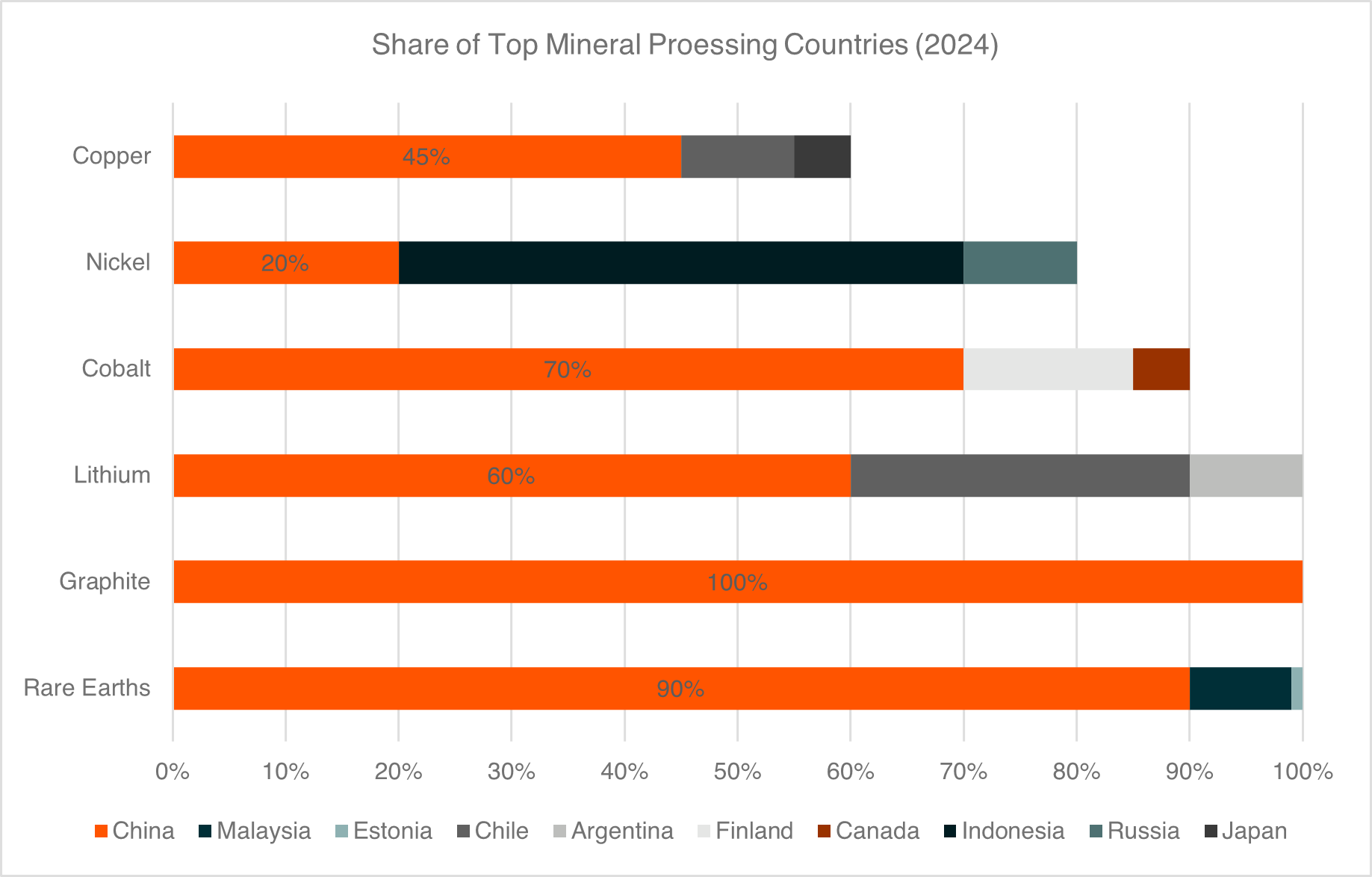

A supply chain dominated by one country

The second dimension of the rare earth story is geopolitical. Rare earth minerals themselves are not particularly rare in geological terms. Deposits exist across multiple regions, including Australia, Brazil, India and China. The challenge lies in what happens after extraction.

Processing and refining rare earths into usable materials is technically complex, environmentally challenging and capital intensive. Over the past several decades, China has built overwhelming dominance across this midstream stage of the supply chain. Today it controls the majority of global refining capacity and an even larger share of magnet production4.

That concentration means the rare earth ecosystem behaves less like a typical commodity market and more like a strategic industrial system. Policy decisions, export controls and national security considerations can influence supply just as much as traditional market dynamics5.

Recent export licensing requirements on certain rare earth materials and technologies highlight how quickly the supply chain can become a geopolitical lever6. Materials that once traded quietly in industrial markets are now appearing in discussions about technology security and global manufacturing resilience. The implication is that rare earths are gradually shifting from commodities to strategic infrastructure.

Source: Benchmark Mineral Intelligence, IEA, World Bank

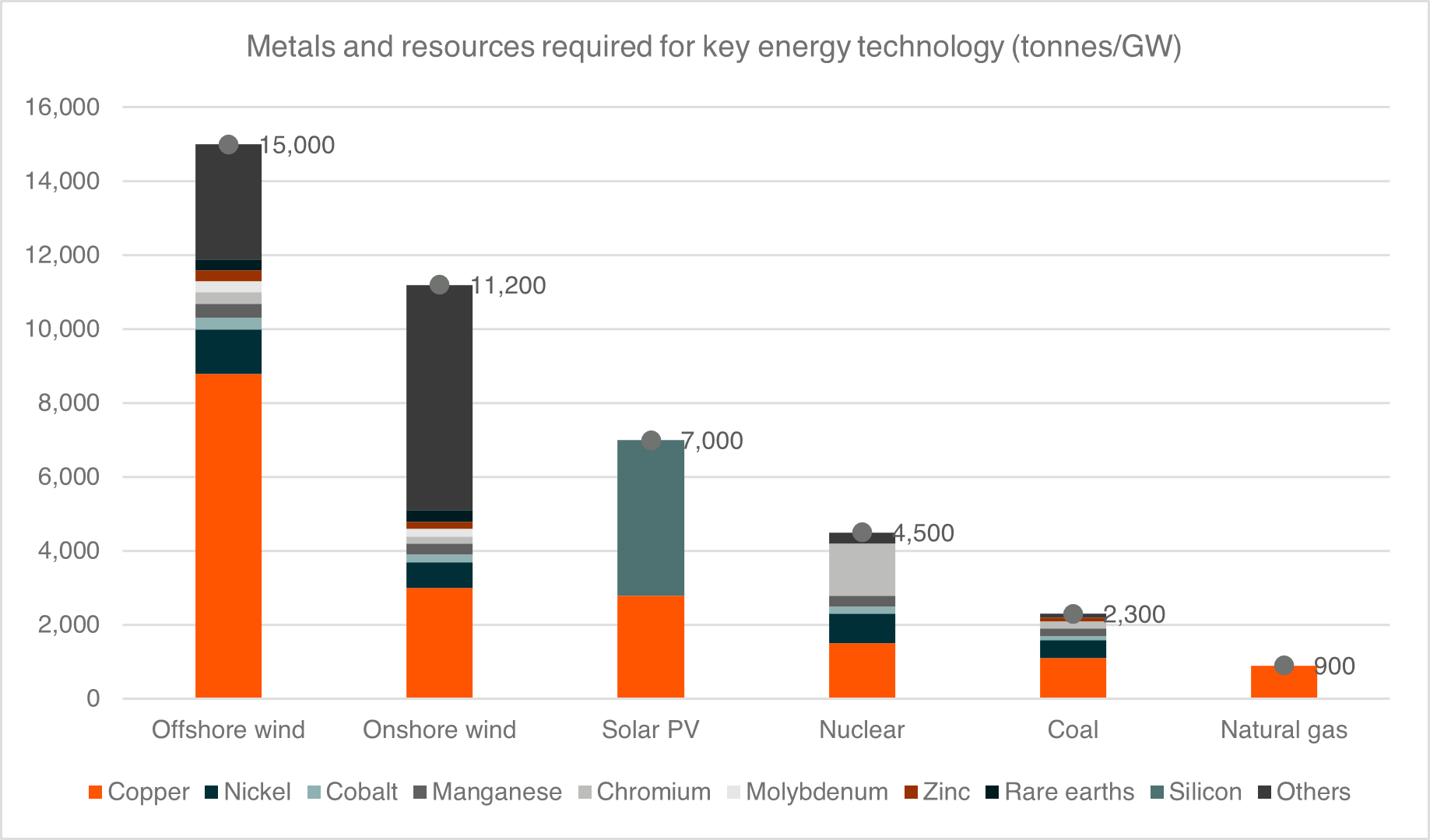

The AI build-out is pulling the materials stack with it

At the same time as geopolitics reshapes the supply chain, structural demand is also accelerating.

Artificial intelligence is one of the most capital-intensive technology cycles in decades. Training clusters, inference infrastructure, hyperscale data centres and advanced semiconductor fabs require enormous quantities of physical equipment. Each layer of that equipment carries embedded materials demand7.

Copper is required to carry electricity through increasingly dense data centre environments. Aluminium is used in cooling systems and structural components8. Rare earth magnets sit inside motors, robotics and semiconductor manufacturing tools. Battery materials support energy storage systems that stabilise power supply.

This dynamic is not unique to AI as many modern energy technologies are already highly materials-intensive, particularly renewable energy systems such as wind and solar, which require large quantities of copper, rare earths and other specialised metals. As electricity demand from AI infrastructure accelerates, it is effectively adding another powerful driver to an already metal-intensive energy transition.

The expansion of AI infrastructure is beginning to pull the entire materials stack higher. This dynamic resembles earlier technology cycles, where new industries triggered demand waves across upstream sectors that initially appeared unrelated. The difference today is that the scale of the AI build-out is far larger and more global. Investment in data centre infrastructure alone is expected to reach trillions of dollars over the coming decade. As this spending accelerates, it pushes demand further upstream into mining, refining and advanced materials processing.

The hidden layer of AI is therefore not software, nor even chips. It is the industrial supply chain that sits underneath them.

Source: IEA, Goldman Sachs Research

From niche inputs to strategic assets

The AI build-out is now spreading beyond software and semiconductors into the materials that enable them. Advanced chips require highly specialised manufacturing equipment, while the infrastructure supporting AI workloads demands enormous amounts of power, cooling, and electrical connectivity. Beneath these systems sits a layer of critical materials that quietly enable the entire technology stack.

Copper carries electricity through increasingly power-dense data centres. Uranium is emerging as a scalable source of reliable baseload power for energy-hungry digital infrastructure. Rare earth elements sit inside the high-precision motors and magnets used across semiconductor manufacturing equipment and advanced electronics.

As AI moves from a software breakthrough into a global industrial build-out, the investment opportunity is expanding beyond compute and into the materials that power the system. This broader exposure is reflected across areas such as copper through the Global X Copper Miners ETF (WIRE), uranium through the Global X Uranium ETF (ATOM), and critical minerals including rare earths through the Global X Green Metal Miners ETF (GMTL).

The future of AI may be digital, but it is built from the periodic table.