With energy markets outperforming in recent weeks and precious metals delivering strong returns over the past several years, the importance of commodity exposure has become increasingly apparent. However, with many commodities now trading near all-time highs, or having already delivered strong returns, investors may be questioning whether the trade has become overcrowded or is nearing exhaustion.

We believe commodities broadly are not overvalued and may be well-positioned for a sustained rally. Investors may benefit from reassessing the role commodities play in portfolios as they increasingly function as strategic, geopolitical assets and potential hedges against inflation, while continuing to offer meaningful diversification benefits.

Key Takeaways

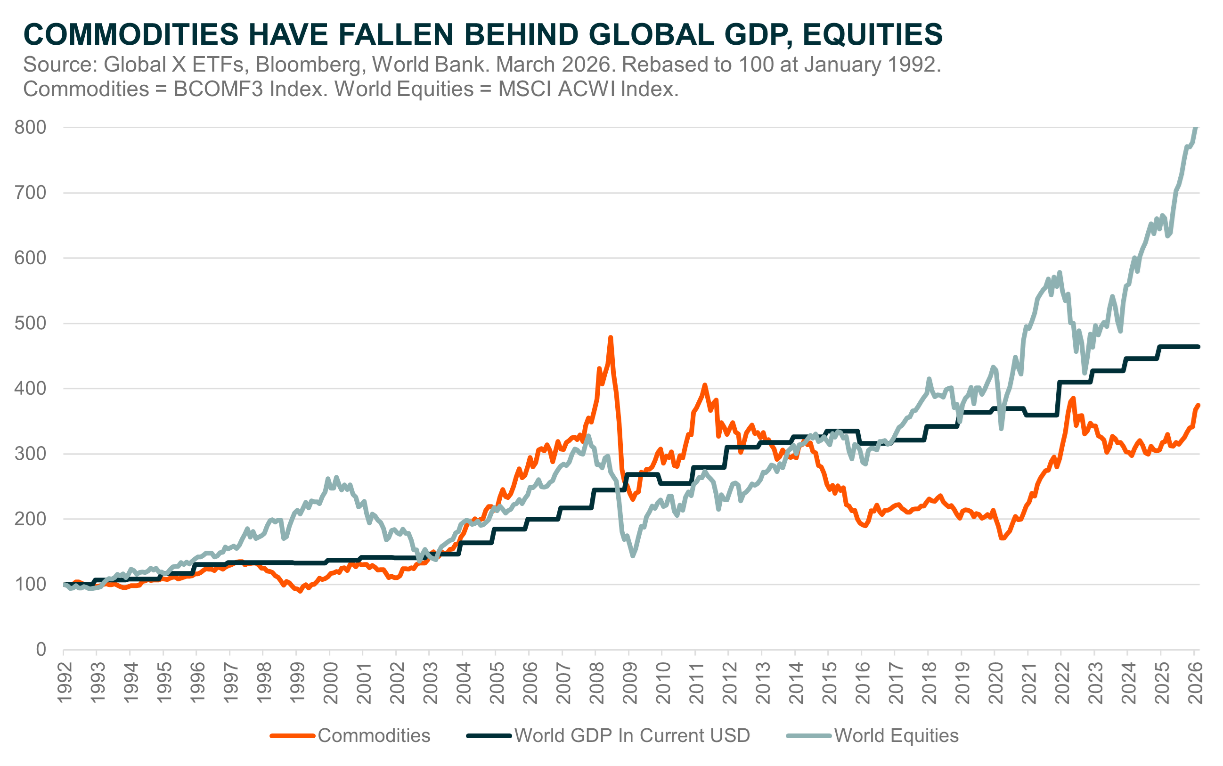

- Commodities have underperformed equity markets and global GDP for more than a decade. That gap is now beginning to narrow as investors reprice the value of real assets and technology buildouts increase demand for raw materials.

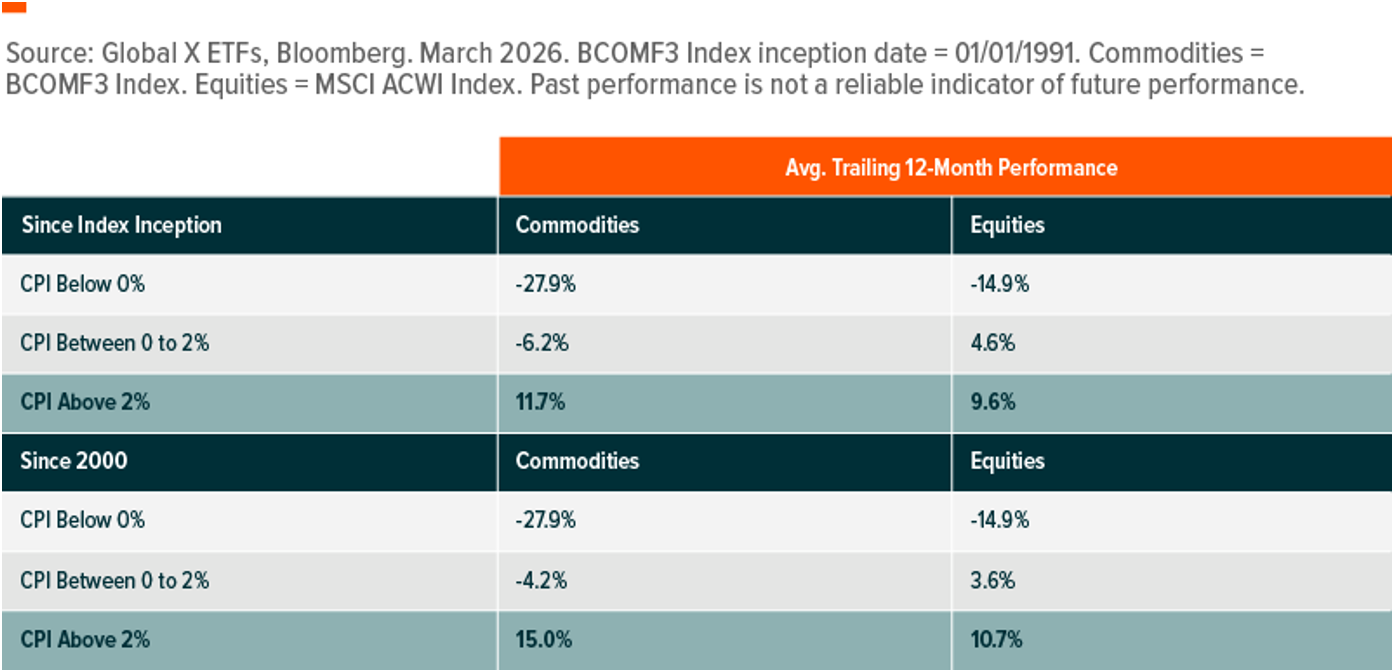

- As the Middle East conflict revives inflation concerns, broad commodity baskets may offer a powerful hedge, having historically outperformed equities during periods of elevated inflation.

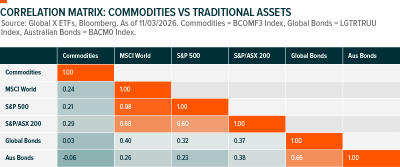

- Broad commodities exposure remains a powerful diversification tool, with historically low correlation to traditional financial assets.

A Long Time Coming

Commodities have long been an under-loved corner of the investment universe, with investors often favouring cashflow-generating assets such as equities and fixed income, citing their higher "predictability" and "fundamentals-driven" nature. While this perspective is understandable, it is also important to recognise that real assets like commodities, not financial instruments, ultimately power the economy, enable productivity, and sit at the centre of even the most future-facing technologies. In that sense, demand for commodities is itself highly fundamental and persistently anchored in real economic activity.

Against this backdrop, it may surprise many that commodities, a key input into global productivity, have significantly lagged global GDP over the past 15 years, while equities have comfortably outpaced both since bottoming in 2009 following the fallout from the Global Financial Crisis.

Past performance is not a reliable indicator of future performance.

There are, of course, many reasons for this underperformance. Low inflation, near-zero interest rates, weaker emerging market demand, overproduction in the early 2000s, and the overall lack of yield all contributed to investors rotating away from commodities and toward risk assets. However, such a divergence between GDP growth and real asset prices is unsustainable in the long-term and often proves self-correcting.

As it stands, commodities remain ~20% below their pre-GFC peaks.1 We believe they may now be in the process of repricing, triggered by the disruption of the 2020 pandemic, and further reinforced by renewed focus on structural megatrends such as electrification, the transition to clean energy, and, more recently, their growing strategic importance in an increasingly deglobalizing world.

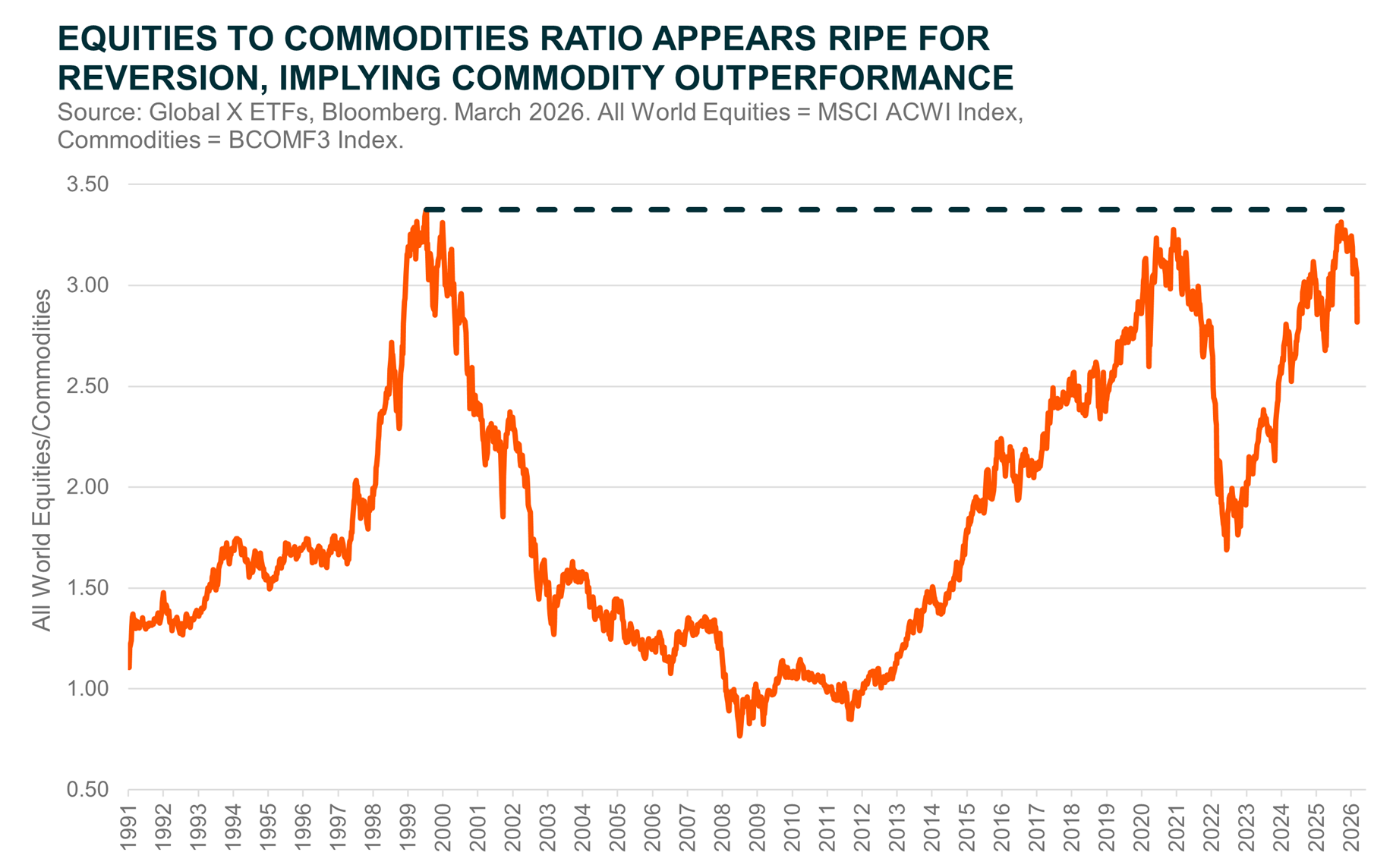

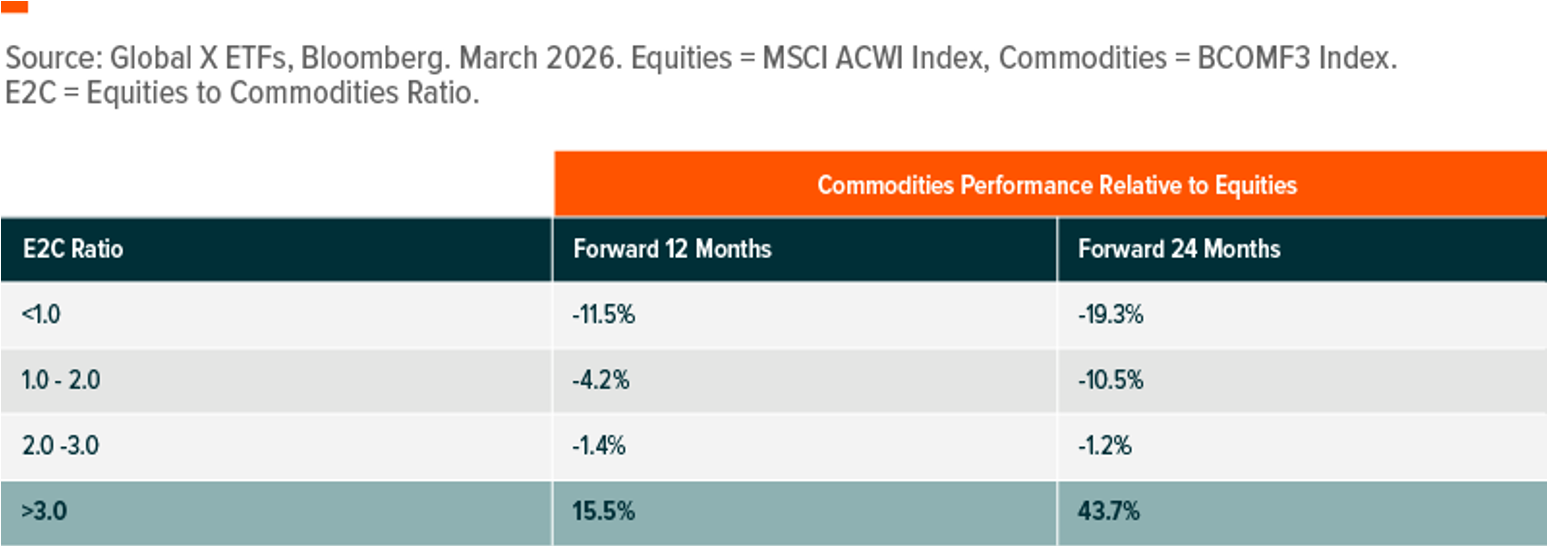

Indeed, if we observe the equities-to-commodities ratio (a commonly quoted relative valuation metric, from here on refer to as E2C), it appears that the outperformance of equities over commodities may be due for a reversal. Over the past 35 years2, an E2C reading of 3.0 or above has reliably signalled a changing of the guard, with commodities often going on to outperform equities sharply over the following 12 to 24 months.

With equities experiencing significant volatility in recent months, and the war in Iran increasing demand for precious metals and driving higher energy prices while also disrupting supply across other soft and industrial goods, commodities appear well positioned to repeat this historical pattern. Indeed, the E2C ratio remained above 3.0 as recently as February 27, 2026, implying a potentially strong 12-24-month period ahead relative to equities.

Bulwark Against Inflation Led Downturns

Some investors may point out that relative valuations and mean reversion are long-term dynamics which, while meaningful, tend to be signs of potential opportunity rather than an outright buy signal. However, the potentially incoming wave of inflation stemming from recent conflicts in the Middle East may provide the catalyst needed to unlock and sustain commodity outperformance.

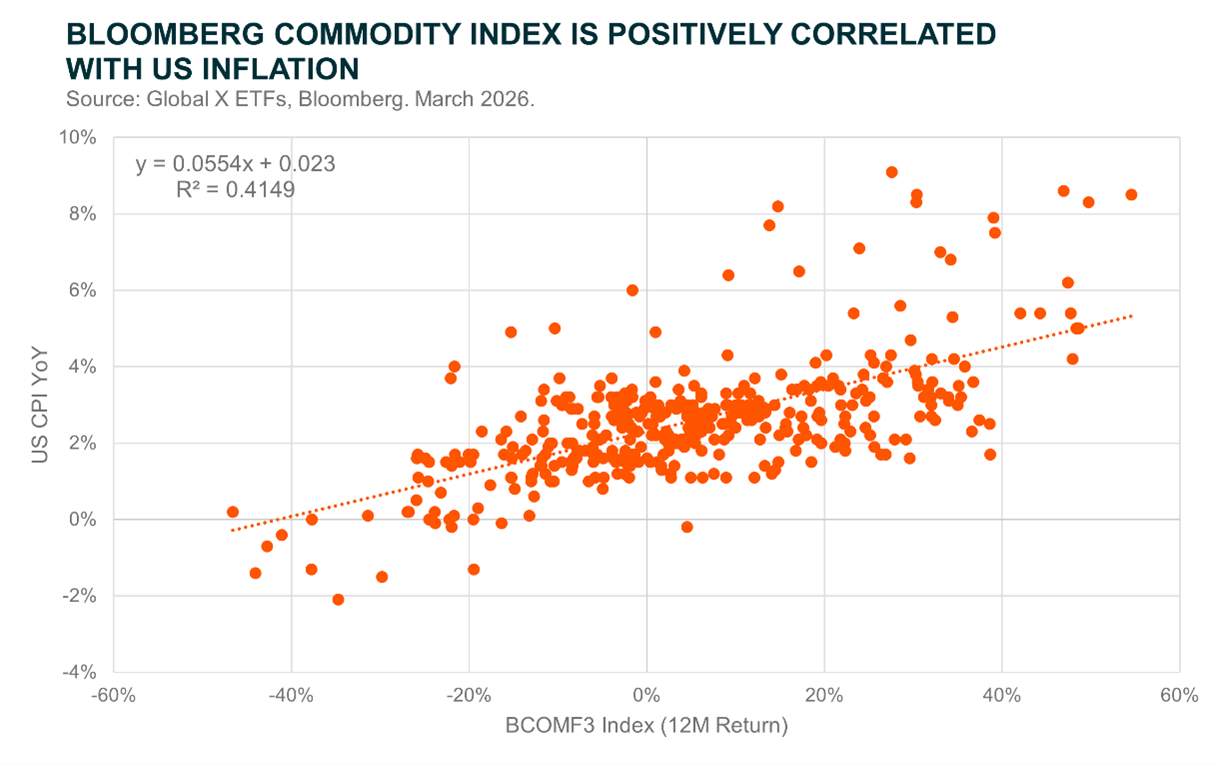

Rising commodity prices, particularly crude oil and natural gas, have a well-understood and strong relationship with consumer prices. These commodities serve as key inputs across the economy, influencing the cost of everything from food and housing to electricity and transportation. As such, it is unsurprising that an analysis comparing a variant of the Bloomberg Commodity Index, a widely cited benchmark for broad-basket commodity prices, with inflation reveals a strong positive correlation.3

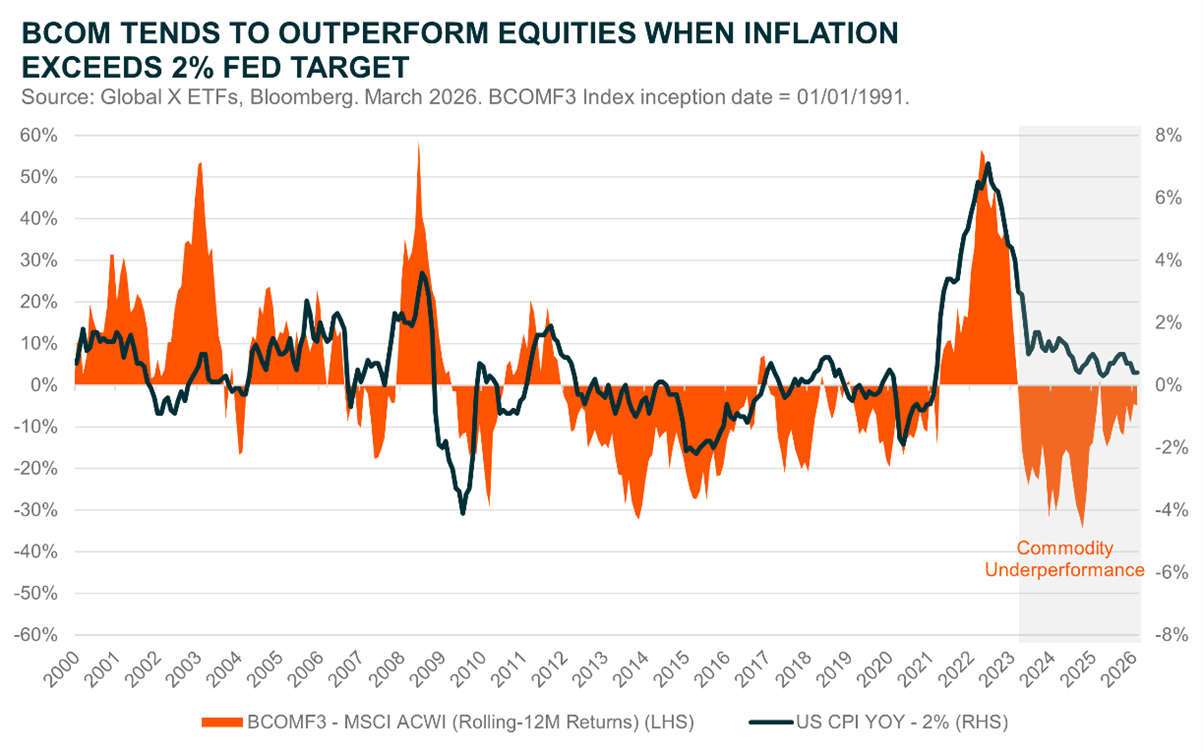

What may be less expected is that commodities do not just perform well in isolation during high-inflation environments; they often outperform equities. This dynamic likely arises because periods of high inflation tend to lead to higher interest rates which, while a net drag on the broader economy, places pressure on equity valuations through higher discount rates. The effect is often even more pronounced when inflation is catalysed by rising input costs.

Looking back at past periods of commodity outperformance in inflation regimes, two themes stand out. The first is inflationary shocks driven by geopolitical disruption, such as the 2022 Russia Ukraine war. The second is structural demand booms, most notably in the early 2000s when China's industrialisation, alongside rapid housing and infrastructure construction, drove a powerful surge in global commodity demand.

Today’s environment appears to combine elements of both. The war in Iran has the potential to push energy prices higher and, if sustained, could contribute to a hotter for longer inflation environment. At the same time, structural demand drivers are building through the rapid expansion of artificial intelligence, electrification, and other large-scale industrial megatrends.

Importantly, these catalysts are emerging at a time when commodities have anomalously underperformed equities despite a high inflation backdrop, potentially laying the groundwork for a more pronounced catch-up rally and even the emergence of a new commodity "super-cycle."

Diversifying With Commodities

For the average investor, investing in commodities can appear complex, often requiring a detailed understanding of the macro environment and global supply and demand dynamics. However, commodities offer benefits beyond attempting to time potential super cycles or serving as a strategic inflation hedge. They have also proven to be powerful diversifiers within equity-bond portfolios due to their historically low correlations with traditional assets.

This characteristic has become increasingly important as equity and bond correlations have risen in recent years, reducing the protective qualities of the traditional 60/40 portfolio during periods of market stress.4 Commodities can help improve risk adjusted returns and smooth portfolio performance, an attractive proposition when considered alongside their strong price potential and their role as upstream beneficiaries of many of the world's most impactful megatrends.

For investors seeking pure, yet broad-based exposure to commodities, the Global X Bloomberg Commodity Complex ETF (BCOM) may be a compelling option. It provides direct exposure to a marquee commodity basket through futures contracts. The fund also aims to maintain exposure to contracts which expire ~3 months in the future, helping minimise negative roll yield by investing further up the curve.

Related Fund

BCOM: For those wishing to invest in broad commodities, the Global X Bloomberg Commodity ETF (Synthetic) (ASX: BCOM) provides one way of doing so. BCOM tracks the Bloomberg Commodity Index, which tracks a basket of global commodities based on production and liquidity. It invests in its index via a swap agreement with J.P. Morgan.