For decades, rare earths and critical metals were largely overlooked by investors, often viewed as exotic, difficult-to-understand materials with real economic applications but limited investment appeal. That is now changing. As geopolitical tailwinds align and technology advances, these commodities are moving from the investment periphery to the centre of global industrial strategy.

Critical technologies such as clean energy, artificial intelligence, robotics, and more - all depend on this group of materials. That is driving a sharp increase in demand, while also elevating their role in geopolitical strategy as governments and corporates look to secure supply chains and reduce strategic vulnerabilities.

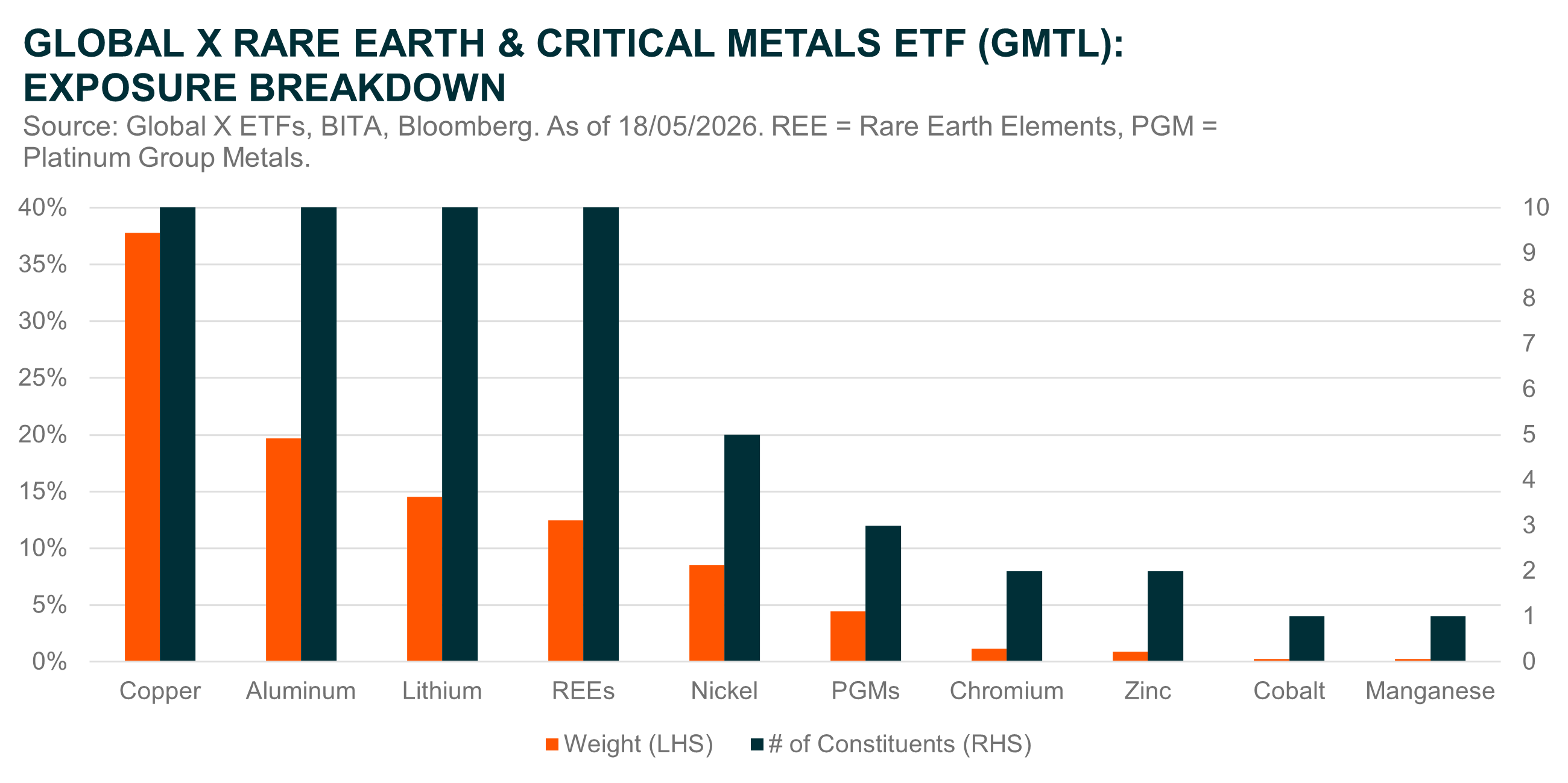

Against this backdrop, rare earths and critical metals present a significant opportunity for investors, sitting at the intersection of national security, industrial competitiveness and technological innovation. The Global X Rare Earths & Critical Metals ETF (GMTL) seeks to provide exposure to a pure play basket of the world’s leading producers of these minerals, offering investors a compelling way to capture their growing technological and geopolitical importance.

Key Takeaways

- While investors often frame modern innovation through a hardware or software lens, these industries are also driving a surge in demand for critical materials.

- The rapid rise in importance of these materials has caught much of the world wrong-footed, leaving supply chains concentrated among a handful of producer nations.

- Governments and industrial consumers are now stockpiling and investing heavily in domestic supply chains to secure uninterrupted access to critical materials.

Materials: The Foundation of Innovation

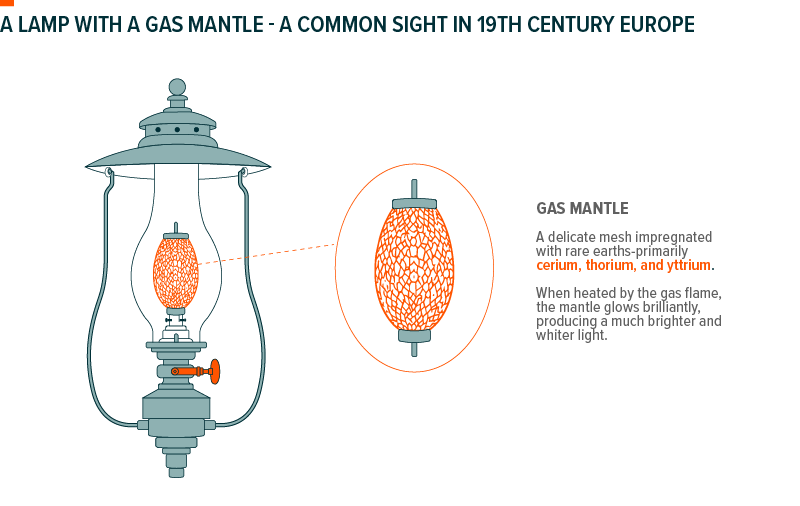

In the late 1800s, rare earth elements were considered obscure curiosities, studied mostly by chemists and scientists with little commercial relevance. That began to change when Austrian chemist Carl Auer von Welsbach discovered that compounds containing cerium, one of the 17 rare earth elements, could be used in gas mantle lighting, producing a brilliant white glow far brighter and more efficient than existing alternatives.1 His invention helped illuminate cities across Europe and marked one of the first meaningful commercial uses of rare earth elements.

Yet this early invention was only a glimpse of what was to come. Throughout the 20th century, advances in physics, metallurgy and electronics revealed that rare earth elements possessed extraordinary magnetic, conductive and heat-resistant properties. Scientists and engineers began incorporating them into radar systems, jet engines, lasers and precision-guided defence technologies during the Cold War.2

By the turn of the 21st century, the world had entered a new technological era, and the rise of smartphones, semiconductors and advanced robotics dramatically increased demand for high-performance magnets and specialised materials. Then came the energy transition. Electric vehicles, wind turbines, battery technologies and modern power systems all required enormous quantities of rare earths.

The relatively unknown story of rare earth elements’ rise to relevance over the past several decades is one that is echoed across a broader collection of minerals and metals. Nickel, for much of modern industrial history, was primarily associated with stainless steel production and coinage before becoming a critical input in high-performance battery chemistries used in electric vehicles and energy storage systems. Cobalt, too, existed largely as a niche industrial metal used in pigments, alloys and aerospace applications before emerging as an integral component of modern lithium-ion battery technology.

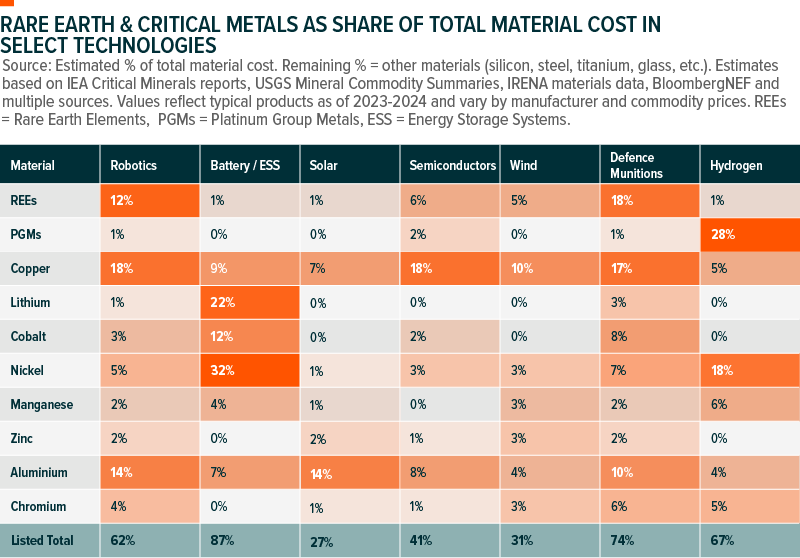

Today, these materials are increasingly labelled as “critical” to economic growth and national security by governments and international institutions. The Global X Rare Earths and Critical Metals ETF (GMTL) invests in producers across ten mineral groups that carry this designation: rare earths, PGMs (platinum group metals), copper, lithium, cobalt, nickel, manganese, zinc, aluminium and chromium. These minerals underpin some of the most important technologies of today and tomorrow, often accounting for a significant share of underlying raw material costs across the technology stack. As a result, they provide investors with a powerful picks-and-shovels exposure to some of the most prominent megatrends of our time.

A Wave of Demand

Given the intrinsic linkage between critical metals and many of today’s fastest-growing technologies, the scale of the opportunity set becomes difficult to ignore.

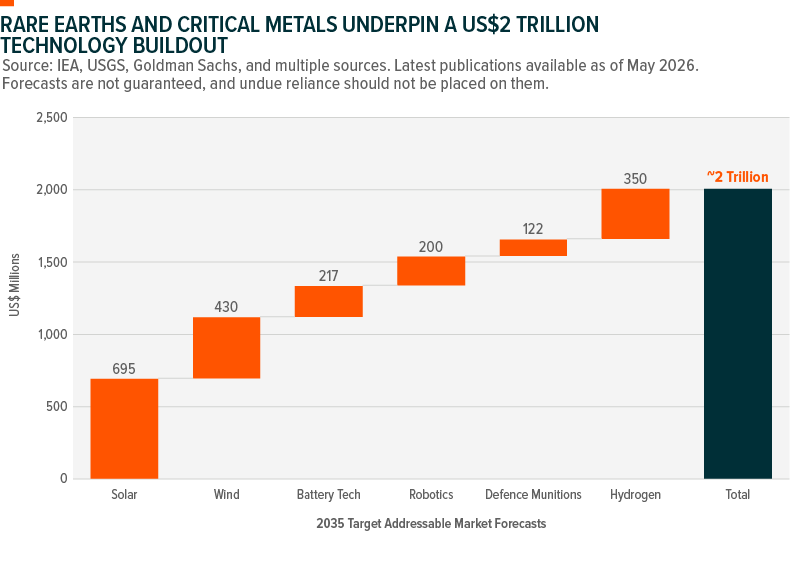

For example, solar and wind energy alone are expected to represent a US$1 trillion market by 2035. Add battery technology, robotics, defence systems and hydrogen – industries that are all heavily dependent on critical metals – and the combined total addressable market rises to roughly US$2 trillion.

As these technologies move through commercialisation and adoption curves, demand for the underlying materials rises alongside them. More importantly, once emerging technologies transition from proof-of-concept into large-scale deployment, unit volumes expand exponentially and material intensity accelerates once again.

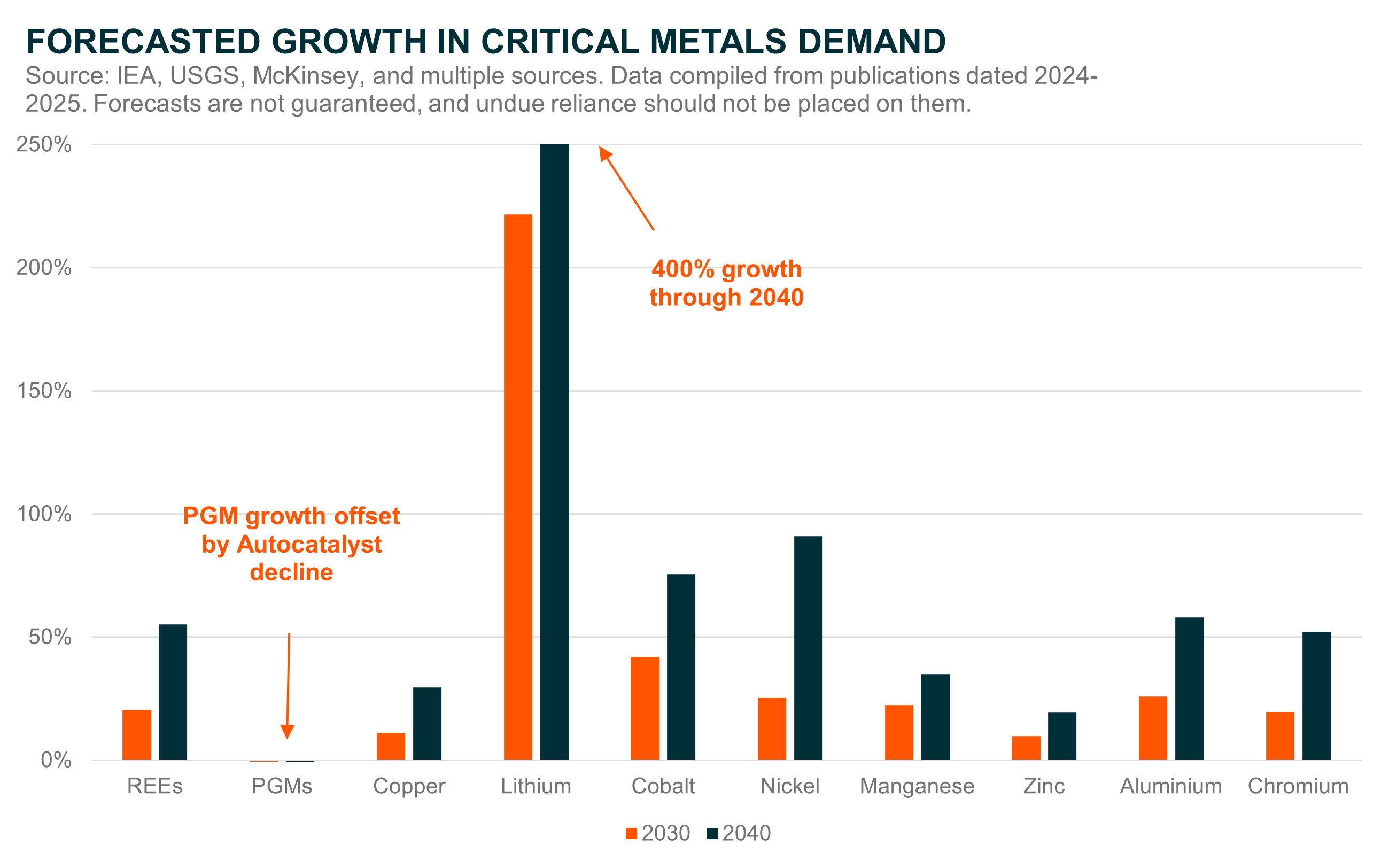

Analysts across the market are increasingly highlighting the scale of the incoming demand wave. A compilation of forecast estimates across the International Energy Agency, US Geological Survey, McKinsey and other institutions, shows that demand across the ten mineral categories represented in the Global X Rare Earths and Critical Metals ETF (GMTL) could grow by an average of 42% by 2030, and approaching 90% by 2040. Highlights within the complex include lithium, where demand forecasts in some cases point to growth of up to 400% by 2040. Cobalt and nickel also stand out, with demand expected to grow between 70-90% over the same period.

With demand expected to accelerate across multiple end markets simultaneously, producers of these materials are increasingly becoming strategic chokepoints within the global industrial supply chain. That positioning has the potential to drive greater investor focus, stronger pricing power and improved long-term profitability across the sector.

It’s Getting Political

It has become increasingly clear in recent years that the world is no longer operating within the same globalised, interconnected and rules-based economic system that defined previous decades. Where the flow of goods was once largely a matter of commerce and comparative advantage, supply chains today are increasingly shaped by tariffs, sanctions, export controls and geopolitical conflict. In response, nations around the world have started prioritising security, resilience and domestically accessible resources in an effort to reduce the risks associated with overreliance on external suppliers.

Unfortunately, the recognition of critical metals as truly “critical” to economic growth and technological innovation is still a relatively nascent development for much of the world. Chinese leader Deng Xiaoping famously remarked as early as 1992 that “The Middle East has oil, China has rare earths”, reflecting China’s early understanding of the strategic importance of these materials.3 However, it was not until China imposed rare earth export restrictions in 2010 following a territorial dispute with Japan that the rest of the world were truly jolted to the fragility of critical mineral supply chains and the strategic chokepoints embedded within them.4

While the 2010 dispute was eventually resolved and market attention faded, it has since become clear that this is a source of leverage China is unlikely to leave unused. In 2025, China once again imposed restrictions on rare earth exports, this time as a countermeasure to trade tariffs introduced by President Donald Trump, reinforcing the strategic importance of critical mineral supply chains within the modern geopolitical landscape.5

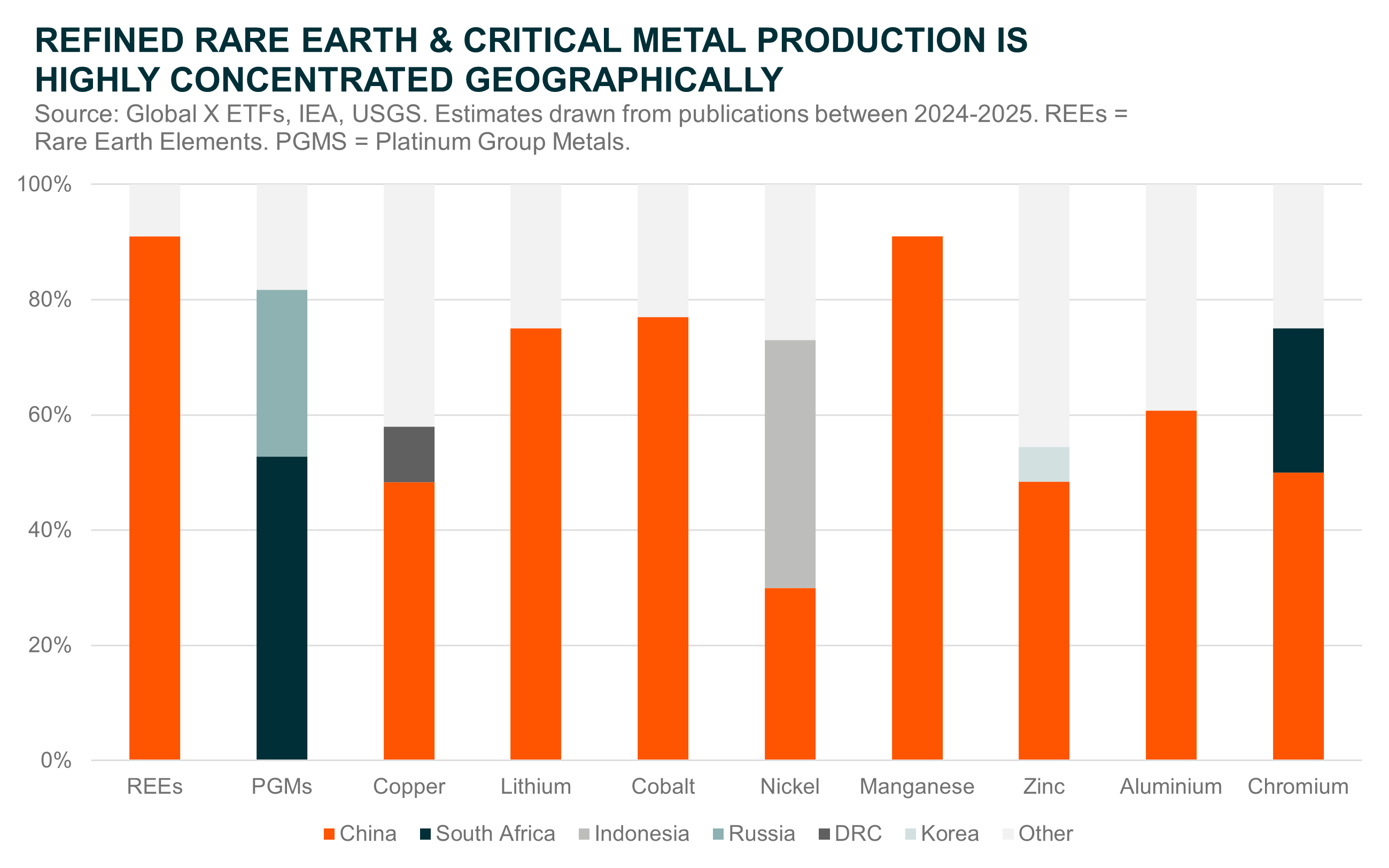

Today, production and processing across this group of critical metals remain highly concentrated. In fact, for every mineral within the complex covered by GMTL, more than 50% - and in some cases close to 100% - of global refined output can be accounted for by just two producer nations. In many cases, these dominant producers are BRICs-affiliated economies, with China remaining the clear leader across much of the complex.

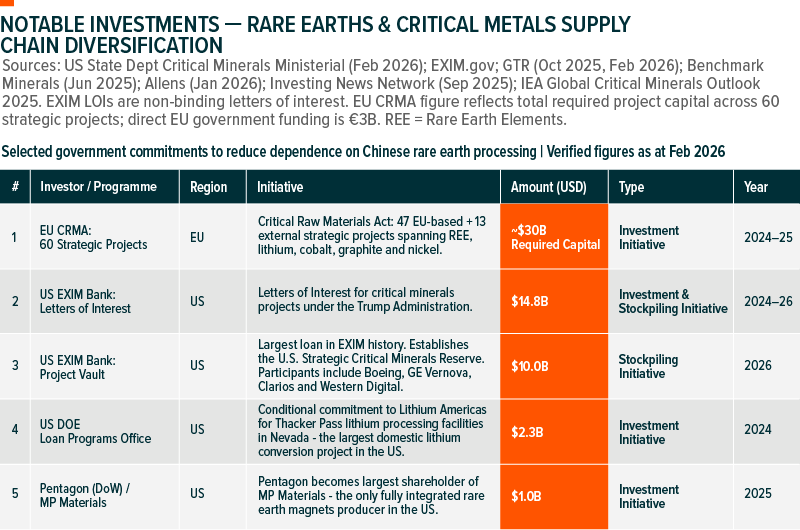

While this concentration represents a strategic vulnerability for nation states around the world, it also creates a two-fold opportunity for investors. As the global economy continues to deglobalize, governments are increasingly incentivised to pursue one of two actions in order to reduce reliance on the supply chain: 1) stockpile critical metals – providing a tailwind for incumbent industry leaders in Asia, or 2) invest heavily in domestic or allied supply chains – a boon to emerging miners across the US, EU, Australia and beyond.

So taken in full, much as Deng Xiaoping suggested in 1992, critical metals are beginning to resemble the oil market of the 20th century: strategically essential assets concentrated within a small number of jurisdictions, capable of shaping industrial competitiveness and geopolitical leverage. However, unlike oil, the critical metals complex sits at the center of multiple technological revolutions simultaneously, underpinning everything from clean energy and robotics to defense systems and artificial intelligence. As nations race to secure reliable access to these materials, the sector is likely to transition from a niche corner of the commodity market into one of the defining strategic investment themes of the coming decade.

Conclusion: A Techno-Geopolitical Megatrend

The critical metals thematic now presents investors with a rare combination of dual tailwinds. On one side sits a powerful wave of technological innovation spanning energy transition, battery technology, robotics, artificial intelligence and more, all of which are driving structurally higher demand for these materials. On the other sits a rapidly shifting geopolitical environment, where governments are increasingly prioritizing domestic supply chains, strategic stockpiles and resource security through policy support and investment incentives.

This convergence means critical metals are no longer simply cyclical commodities tied to industrial production, but increasingly strategic assets embedded within the infrastructure of the new economy. As demand accelerates and capital flows into securing and expanding supply chains, the companies involved in producing, refining and recycling these materials are likely to become key beneficiaries of this transition.

The Global X Rare Earths and Critical Metals ETF (GMTL) provides investors with exposure to a global basket of companies operating across this value chain, offering a way to access a thematic that sits at the intersection of technological disruption, industrial policy and geopolitical change.

Related Fund

GMTL: The Global X Rare Earths and Critical Metals ETF (GMTL) provides access to a global basket of rare earth and critical metals producers which stand to benefit from being a key part of the value chain facilitating growth in frontier technologies such as battery tech, robotics, clean energy and more.