For much of the past decade, equity markets rewarded companies that required relatively little physical capital. Software platforms and digital businesses demonstrated how scale could be achieved without extensive infrastructure, allowing revenue growth to accelerate faster than investment. Asset-light models became associated with high returns on capital, rapid scalability and structural market leadership1.

A different set of economic forces is now drawing attention to industries built on physical capacity. Rising real interest rates increase the cost of capital and change how markets value long-duration growth. At the same time, geopolitical fragmentation and supply chain restructuring are forcing governments and corporations to reconsider how critical systems are built and maintained. Energy networks must expand, industrial production is being reshored across multiple regions, and infrastructure once taken for granted is being reassessed as strategically important2.

This backdrop has brought greater attention to what some investors describe as the HALO trade, short for Heavy Assets, Low Obsolescence3. The concept focuses on companies built around substantial physical infrastructure and long-lived capital assets that are difficult to replicate. Their advantage is not based on rapid innovation cycles but on scale, engineering complexity and the time required to build the systems they operate. These assets often sit at the centre of economic activity, quietly supporting the movement of energy, goods and materials across entire economies.

Key Takeaways

- HALO investing focuses on companies with heavy assets and low obsolescence, where infrastructure, capital intensity and long development timelines create durable barriers to entry.

- Structural forces including higher real yields, supply chain realignment and industrial policy are increasing the strategic importance of physical capacity.

- Industries built on infrastructure, industrial systems and critical materials may attract renewed investor attention as markets reassess the value of tangible assets.

The Repricing of Physical Capacity

The HALO framework reflects a broader repricing taking place across the global economy. For years, capital flowed toward industries capable of scaling rapidly with minimal physical investment. Businesses that could expand through software or digital platforms achieved high margins and strong returns on capital, reinforcing the perception that asset-light models represented the most attractive form of growth. At the same time, advances in artificial intelligence are beginning to challenge the durability of certain software-based business models, particularly those built on seat-based or service-driven pricing, further reinforcing the relative advantage of companies anchored in physical assets that are harder to replicate.

Several structural forces are now shifting that balance. Governments across major economies are investing heavily in energy security, domestic manufacturing capacity and strategic infrastructure. Supply chains that once prioritised efficiency are being redesigned with resilience and redundancy in mind, particularly in sectors linked to energy systems, transportation networks and advanced industrial production4.

Expanding these systems requires substantial capital and long development horizons. Building a power grid, developing a pipeline network or constructing a large industrial facility involves years of engineering work, regulatory approval and financial investment before it becomes operational. These projects are rarely replicated quickly, which creates structural scarcity once capacity is established.

Assets developed under these conditions often remain embedded in the economy for decades. Their durability stems from the combination of capital intensity, regulatory oversight and the essential services they provide. This dynamic sits at the centre of the HALO concept, where the value of an asset is defined not by rapid technological change but by the scale and permanence of the system it supports.

This shift is also evident within traditional asset-light sectors, where large technology platforms are now allocating significant capital toward data centres, power infrastructure and physical network capacity, reinforcing the growing importance of tangible systems.

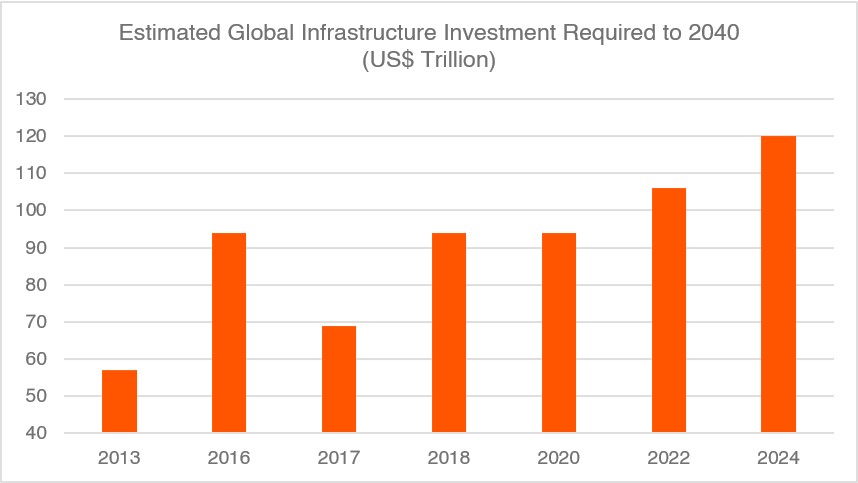

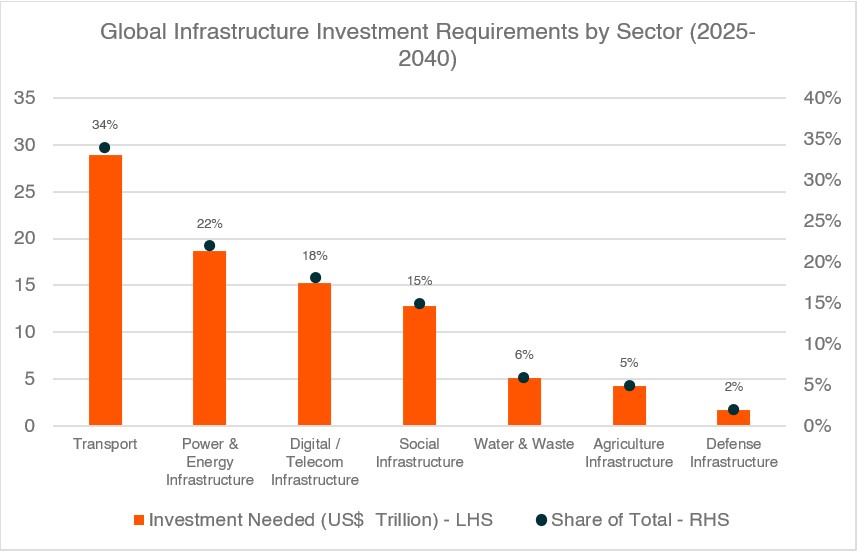

Successive estimates of total infrastructure investment required by 2040 have been revised higher over the past decade, reflecting rising energy demand, electrification, digital networks and the rebuilding of industrial capacity.

Source: McKinsey Global Institute, IEA, BNEF, Oxford Economics

Industries Built on Heavy Assets

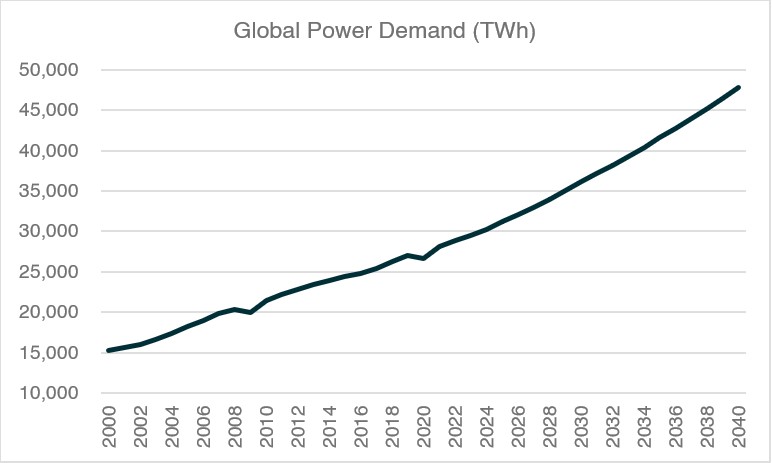

HALO businesses typically operate in sectors where economic value is anchored in large physical systems that support national and global supply chains. Energy infrastructure provides one of the clearest examples. Electricity transmission networks, pipelines and large-scale power generation assets require enormous capital investment and complex regulatory approval processes, yet once built they become foundational components of modern economies5.

Transportation networks exhibit similar characteristics. Rail systems, port infrastructure and freight corridors represent multi-decade investments that facilitate the movement of goods across entire regions. These assets often involve large engineering projects and extensive coordination between governments, utilities and industrial contractors before they can operate efficiently.

Industrial manufacturing capacity also reflects the HALO framework. Advanced production facilities, heavy machinery and specialised equipment require years of planning, design and construction before reaching operational scale. Once established, however, these systems form the backbone of industrial supply chains and remain difficult for competitors to replicate.

Another important layer sits upstream in critical materials and industrial inputs. Infrastructure networks and manufacturing systems depend on specialised metals, engineered components and industrial machinery embedded throughout supply chains. These inputs often receive less attention than finished products, yet they are essential for maintaining the operation of energy systems, transportation networks and industrial facilities.

Across these sectors, the defining feature is the same. Economic value is anchored in tangible assets that require substantial investment, engineering expertise and time to build. This concentration is reflected at a global level, where transport and energy infrastructure account for the largest share of total investment needed, highlighting where physical capacity constraints are most pronounced.

Source: Global Infrastructure Hub (G20), McKinsey Global Institute, World Bank Infrastructure

Past performance is not a reliable indicator of future Performance.

A Different Lens for Long-Term Investing

Viewing markets through the HALO framework highlights a different source of competitive advantage. Instead of focusing exclusively on companies capable of scaling rapidly with minimal capital investment, the approach emphasises industries where value is embedded in infrastructure and physical capacity.

Assets such as power grids, pipelines, rail corridors and industrial facilities cannot be recreated quickly. Their value reflects decades of investment, regulatory frameworks and specialised engineering capabilities. These systems underpin the movement of energy, materials and goods that support broader economic activity6.

Historical cycles provide some context for this shift. During the early 2000s commodity supercycle, rising demand for infrastructure and industrial inputs drove sustained outperformance across resource and capital-intensive sectors, reflecting a similar repricing of physical capacity.

In an environment where resilience, security and industrial capability are becoming more prominent economic priorities, companies operating within these capital-intensive sectors may command renewed strategic importance. The HALO framework therefore encourages investors to examine markets through a lens that emphasises scale, scarcity and infrastructure as drivers of long-term economic value.

Source: International Energy Agency (IEA)

Past performance is not a reliable indicator of future Performance.

Accessing HALO Themes Through Global Markets

Many sectors associated with the HALO framework sit within global infrastructure, industrial and materials industries. The Australian equity market provides strong exposure to certain resource producers but offers more limited representation in global infrastructure operators, specialised industrial manufacturers and advanced equipment producers that underpin many large-scale economic systems.

International markets contain a broader range of companies operating across energy infrastructure, transportation networks, industrial machinery and critical materials supply chains. These businesses often control the physical systems that enable energy distribution, goods movement and industrial production across regions and continents.

For Australian investors, accessing these industries through global thematic exposures provides a way to participate in the physical foundations of the global economy. As markets place greater emphasis on infrastructure, industrial capacity and durable assets, the HALO framework offers a useful perspective for understanding how heavy-asset industries may shape long-term economic growth.

- Global X Artificial Intelligence Infrastructure ETF (AINF): Exposure to companies involved in the physical infrastructure supporting modern computing, including data centres, power systems and network capacity. While HALO is not centred on AI, the fund captures the heavy industrial systems required to build and operate large-scale digital infrastructure.

- Global X Uranium ETF (ATOM): Provides exposure to companies across the uranium and nuclear fuel ecosystem supporting nuclear power generation. Nuclear energy systems involve large upfront investment, complex regulation and facilities designed to operate for decades, aligning closely with the HALO concept of heavy assets with long lifecycles.

- Global X Green Metal Miners ETF (GMTL): Tracks producers of metals such as copper, nickel and lithium that are essential inputs for infrastructure, energy systems and industrial capacity. These materials sit upstream in supply chains yet remain critical to building and maintaining large physical systems.

- Global X Hydrogen ETF (HGEN): Invests in companies involved in hydrogen production, storage and distribution infrastructure. Hydrogen systems require significant capital investment and industrial engineering, reflecting the type of heavy-asset industries associated with the HALO framework.

- Global X US Infrastructure Development ETF (PAVE): Tracks companies involved in the construction and development of infrastructure including roads, bridges, engineering systems and construction materials. Infrastructure assets are capital intensive, take years to build and remain embedded in the economy for decades, making them a clear HALO exposure.

- Global X Silver Miners ETF (SLVM): Provides exposure to global silver mining companies supplying a metal widely used across industrial applications and energy technologies. While primarily a commodity exposure, silver remains an important input supporting industrial systems and manufacturing supply chains.

- Global X Copper Miners ETF (WIRE): Invests in companies producing copper, a foundational industrial metal used in power grids, electrification, transport and infrastructure systems. Copper plays a central role in building and maintaining the physical networks that underpin modern economies.