Investing in technology (“tech”) usually comes with stereotypes. The stereotypes include tech being riskier, more prone to bubbles and full of loss-making companies. Given the harsh lessons of the dotcom bubble in 2000, the stereotypes are understandable to a point.1 Nevertheless, the tech sector has changed quite significantly over the past 20-odd years. Fundamentals have improved and now increasingly resemble the broad market. In this article, we sieve through the stereotypes and take a hard look at the sector, as proxied by the Nasdaq 100 (NDX Index). We then end with two case studies on more niche technology indices and illustrate the same point.

Key Takeaways

- A small group of market leaders significantly influences industry trends and contributes to value creation within the technology sector.

- Contrary to the perception that technology investments are high-risk, leading innovative companies score well on quality metrics like profit margins and free cash flow yields.2

- Investing in a concentrated portfolio of leading technology firms can yield substantial returns, challenging the traditional risks associated with tech investments.

The Stereotype of Tech Being Junkier is No Longer Valid

The dotcom era, characterised by speculative investments and inflated stock prices, shaped investor perceptions of the tech sector. During this period, companies with weak financials were often overlooked as investors focused on the promise of future growth. For instance, AOL briefly became the largest company in the S&P 500 in December 1999, highlighting the exuberance of the era. However, as the bubble burst, many of these companies, including AOL, faced significant challenges, leading to a reassessment of the tech sector's viability.

Given the money that was lost in that period, many investors have bad muscle memory when it comes to investing in tech. Especially given that at the time of writing the tech sector is on another multi-year tear, driven by artificial intelligence.

It may be of some comfort then to look at the numbers and see how things have changed. The tech sector of today is very different to that of the turn of the millennium.

Fundamentals: How the Tech Sector Has Changed

The quality of companies in the tech sector – as proxied by the Nasdaq 100 – has changed drastically over the past two decades. There are several ways of looking at this. A favourite of mine is index turnover, which measures how many old stocks are getting thrown out of the index and new ones added in. This is an important number: if turnover is high, it is usually because companies are falling and there’s correspondingly more churn and burn. When turnover is low it indicates more stability within the constituents.

The Nasdaq 100 index turnover has stabilised over the past two decades, indicating increased stability within its constituents. This suggests that companies included in the index are demonstrating sustained performance to retain their position. From 2000 to 2010, 35% of companies remained in the NDX, a figure that increased to over 45% from 2010 to 2020. This trend underscores the sector's maturity and enhanced stability following the tech bubble. Moreover, our analysis reveals that while the turnover has stabilised, a small subset of companies played a significant role in market capitalisation growth. Specifically, approximately 40% of the index's market capitalisation growth can be attributed to just 5% of the companies over the specified period, highlighting their outsized contribution to value creation.

Technology Companies Have Not Only Driven Value Creation but Also Becoming Increasingly Stable.

Looking at the balance sheets of these companies, we also see clear evidence of improvement. Importantly, regarding the stereotype that tech companies are often loss-making, between 2000 and 2023, the percentage of profitable companies within the Nasdaq rose from 59% to 86%.3

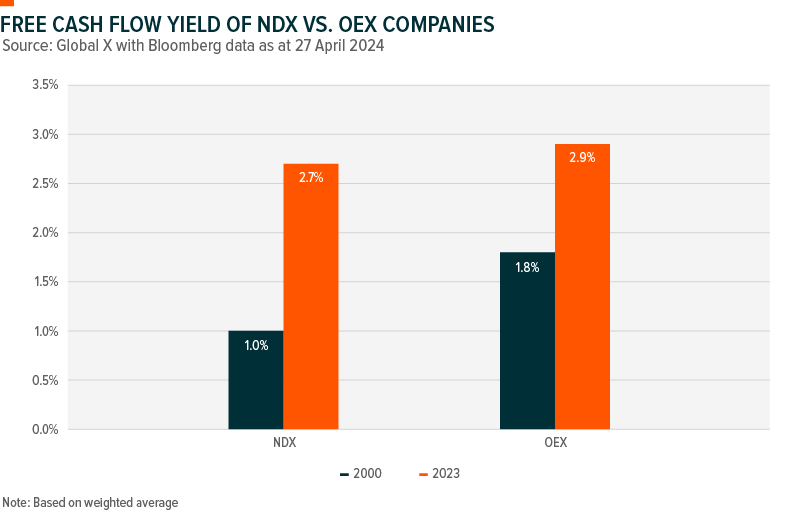

Looking at Jeff Bezos’ favourite number, free cash flow yield, which measures how much cash tech companies are generating relative to their market value, the Nasdaq 100 free cash flow yield climbed from 1.0% to 2.7% over the same period. This indicates improved profitability, yes, but also potentially improved value as well. If we compare this to the S&P 100 Index (OEX), which comprises the top 100 companies in the S&P and measures the broader market, 91% of companies were profitable in 2023, with a free cash flow (FCF) yield of 2.9%. This indicates the tech sector is converging on the broad market.

Financial Health of Nasdaq 100 Companies Has Improved Considerably

Profitable = positive EPS for the last financial year of the stated period

FCF = free cash flow = earnings before in interest & tax – operational cash flow – capital expenditure

Net cash = positive value from liquid cash position – short- and long-term debt

Perhaps most startling is what has happened to profit margins themselves. Operating margins rose from 2.1% in 2000 to 27.7% in 2023, surpassing that of S&P 100’s 25.6%. These numbers are strongly suggestive of improving financial fundamentals and grates against the stereotype of the tech sector being full of loss-makers.

Free Cash Flow Yield Has Improved Along With Improving Profitability

Operating margins = reported operating profit / sales

Financial Performance Metrics Of Nasdaq 100 Companies

Case Studies: Global X Artificial Intelligence Index and FANG+ Index

To further illustrate our points that tech stocks are now fundamentally stronger compared to two decades ago, we explore two tech themes: artificial intelligence and the Magnificent Seven.4 For our investigation, we use the indices tracking the Global X Artificial Intelligence ETF (ASX: GXAI) and the Global X FANG+ ETF (ASX: FANG), being Indxx Artificial Intelligence and Big Data Index (IAIQ) and NYSE FANG+ Index (NYFANG) respectively. We consider an analysis of these indices to be timely, given the concerns raised in the market about overvaluation in artificial intelligence and of the Magnificent Seven stocks.

As we can see below, contrary to some beliefs, investing in these sectors does not necessarily involve risking capital on financially weak companies. As of the end of 2023, 80% of companies in the artificial intelligence index were profitable, 50% held net cash positions, and 82% generated positive free cash flow, with an average FCF yield of 3.0%. Similarly, the FANG+ index showed strong financial health: 90% of its companies were profitable, 60% were in net cash positions, and all generated positive free cash flow, with an average FCF yield of 3.6%.

Conclusion: Time to Move on

Investors know that markets are forward looking, and our industry is fond of disclaiming that “past performance is no guide to the future”. Yet investors often look to history as a guide nonetheless. There may be some comfort in knowing that the tech sector of today looks very different to that of the past. The tech sector now has meaningful earnings, strong balance sheets and long-term structural applications. Stereotypes and scar tissue may remain, but they can change. A topic that investors should learn and embrace when it comes to tech investing.