We believe US and Israel joint action against Iran has shifted the calculus for the Defence Tech theme. While US and allied capabilities far exceed Iran’s, the engagement dynamics are different: sustained pressure from high-volume, low-cost expendable systems can force defenders to burn scarce, expensive interceptors.1

In that environment, cost curves and replenishment cycles become as important as peak capability. Layered on top of the broader global re-armament trend, the ongoing conflict could add urgency to defence tech procurement and modernisation.

The Iran Campaign: Initial Days

On February 28, 2026, the United States and Israel launched major strikes on Iran’s leadership and military infrastructure in a decapitation-style campaign. Iran’s Supreme Leader, Ayatollah Ali Khamenei, was killed, along with senior Islamic Revolutionary Guard Corps (IRGC) and defence leadership. Over the past week, the United States has hit 3,000 targets and lost seven service members.2,3

Since then, the conflict has broadened, destabilising regional trade and civilian life, while shifting global geopolitical and security math.

The Battlefield Variable: Duration

For defence tech investors, the key variable is the duration of this conflict. US operation was well telegraphed and likely priced in, but Iran’s response has been sporadic and more aggressive than many expected, raising the odds that this turns into a longer, operationally messy campaign. That shift matters because it pressures US stockpiles and pulls replenishment forward, a scenario likely different from the market’s base case. The administration has signaled the conflict could extend for four weeks or more.4

Complicating matters is the unprecedented fragmentation of Iran’s leadership, which makes negotiation harder and raises the risk of miscalculation. Repeated, phased targeting of US and allied assets across the region could be a possibility, raising odds of continued spillover into a broader regional conflict. Ceasefire mechanics are also still murky. These deals usually require a clear counterparty, and Iran’s disrupted command structure could slow negotiations even if there’s willingness on both sides.

Iran’s battlefield playbook also loosely mimics Ukraine’s, with a less resourced actor leaning into dispersion and improvisation, seeking to impose costs rather than win decisively. It is not an apples-to-apples comparison, especially given Ukraine’s backing from deep-pocketed allies, but it frames why the market can misprice this kind of conflict at the outset.

In our view, the messy dynamic underscores the breadth of preparation, planning, and real-time resource reallocation the United States may need as the conflict drags on. It also puts pressure on the US defence industrial base to adapt to shifting operational realities.

Battlefield Economics Matter

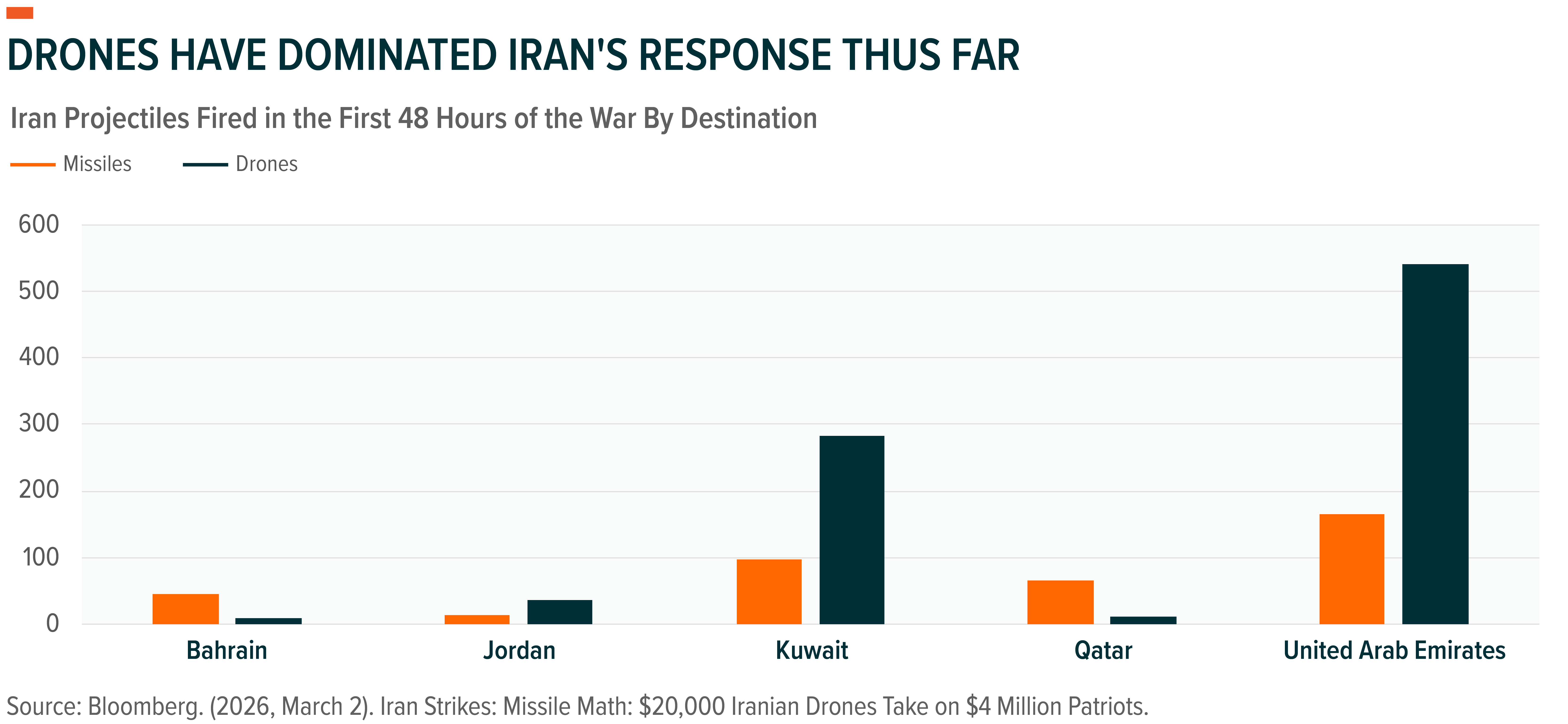

The cost math sits at the center of Iran’s playbook. Iran’s main tools, especially mass-produced one-way drones - like the Shahed - are cheap and easy to replace. Their drone supply chain is already battle-tested, given Iran’s role supplying drones to Russia during the Ukraine war.5 Iran is believed to have approximately 80,000 drones, with each unit costing between US$20,000 to US$50,000, and the ability to produce hundreds or even thousands per month.6,7 So far, Iran has fired more than 2,000 one-way drones since the conflict began.8

On the other side, US and Israeli defences often rely on much more expensive interceptors and higher-end munitions. Interceptors can cost anywhere between US$3 million and US$12 million and are used to take down drones that usually cost a tiny fraction of that.9 Therein lies the asymmetry. If this situation turns into frequent, sustained engagements, the advantage can shift from pure capability to cost curves and volume. That gives Iran room to keep a crude campaign going longer than people anticipate at this time. The practical result is inventory pressure, and a higher chance that US replenishment becomes a priority over the coming months.

Importantly, US interceptor inventories were already tight. The United States reportedly used about 25% of its THAAD interceptors in the June 2025 Israel-Iran conflict, and replenishment can take 3-8 years.10 In our view, the most effective categories in modern, volume-heavy conflict are: a) drones and counter-unmanned aircraft systems (UAS); b) interceptors and air/missile defence stacks (Patriot, THAAD, Standard Missiles, radars); and c) the software and command / control layer. If inventory burns are rapid, reorder cycles can accelerate, boosting procurement.

That’s not to say that the United States cannot ramp up its industrial base to produce lower-cost drones and munitions to stabilise the campaign. The LUCAS drones deployed in this Iran attack, for example, reportedly went from public reveal to deployment in under eight months and marks the first known use of one-way drones by the United States.11 But scaling that output is unlikely to come without more spending.

Markets Could Reprice Defence Tech

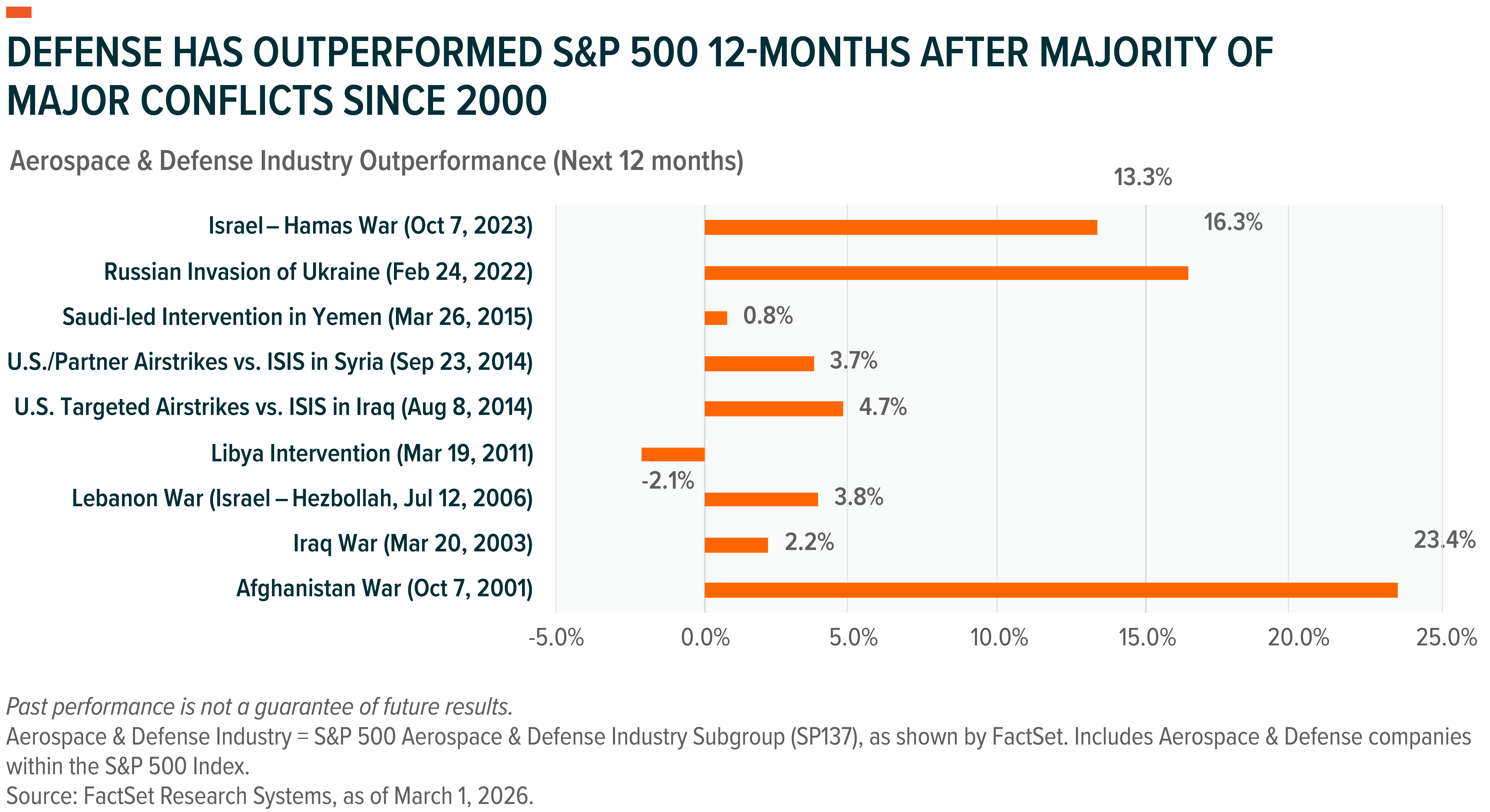

Going back to 2000, our analysis shows that when major global conflicts unfold, defence stocks within the S&P 500 outperformed the overall index by roughly 7.3% over the next 12 months.12* Against today’s backdrop and positioning, that historical pattern could indicate a supportive setup for defence tech exposure. Defence is still largely under-owned. The Aerospace & Defence industry makes up less than 2.5% of the S&P 500 index.13 The ongoing rotation away from Big Tech could provide further support for the sector and the defence-tech theme.

*Past performance is not a reliable indicator of future performance.

Even before this conflict, defence demand was firm. A prolonged conflict scenario raises the probability of incremental procurement and accelerated deliveries. Global X estimates global defence spend to cross US$3.6 trillion by 2030, up from US$2.7 trillion in 2024, with strong chances that a replenishment cycle drives upside growth to the forecast.14*

In the United States alone, the Department of War intends to obligate US$152 billion in reconciliation funding in fiscal year (FY) 2026, up from the previously anticipated US$113 billion. Total US defence expenditures are now expected to reach US$1 trillion in FY2026, years ahead of the Congressional Budget Office’s original estimate.15

*Forecasts are not guaranteed and undue reliance should not be placed on them.

Conclusion: Inventory Burn Meets New Defence Needs

The Iran conflict marks a new chapter in global defence readiness. As refresh cycles and modernization simultaneously advance, defending against high-volume, low-cost, expendable systems becomes imperative. That shift strengthens the opportunity set for companies tied to drone production and the defensive stack around it, including counter-drone, air and missile defense, as well as directed-energy systems. In our view, the market has still not fully priced the durability of these procurement tailwinds.