Nuclear power is a clean, efficient, and essential source of electricity used to meet the world’s growing energy demands. Nuclear power can produce electricity at a greater scale while minimising greenhouse gas emissions. This helps countries expand their electricity grid and usage, while limiting air pollution. Close to 10% of the world’s electricity was generated from nuclear power in 2022, accounting for approximately one-quarter of the world’s low-carbon electricity.1

Uranium fuel enables nuclear power plants to generate electricity. A single uranium pellet, slightly larger than a pencil eraser, contains the energy equivalent of a ton of coal, three barrels of oil, or 17,000 cubic feet of natural gas.2 Global nuclear power output primarily drives the demand for this commodity. Despite expected growth in nuclear power, and a correlative increase in uranium demand, gaining exposure to this commodity sometimes proves difficult. Uranium trades with thin liquidity on futures exchanges and there are ownership restrictions related to its usage in weapons production.

Key Questions Covered

- What is uranium?

- How is uranium extracted?

- How is uranium used to generate electricity?

- What are the advantages of uranium?

- What is the outlook for uranium demand?

- What is the status of the uranium supply?

- Are uranium prices expected to recover?

- How can you invest in uranium?

Explaining Uranium and Its Extraction

Uranium is a heavy, dense, and radioactive metal, making it a potent source of energy. Found in most rocks in concentrations of two to four parts per million, it appears as commonly in the Earth’s crust as several other metals, such as tin and tungsten.3 Uranium extraction generally involves recovery from the ground using open-pit mining, underground mining, or in-situ leach (ISL) methods.4

Open-pit and underground mining methods collect rocks that contain very low concentrations of uranium. A milling process crushes the rocks to grind them into fine fragments, while added water helps create a slurry – a semi-liquid mixture. Sulphuric acid or an alkaline solution mixed with the slurry allows 95-98% of the uranium to be recovered. Uranium oxide, also known as yellowcake, is precipitated from this solution. Yellowcake must undergo yet another enrichment process to make it viable as nuclear fuel.5

The preferred method for extracting uranium, ISL mining, proves more cost-effective and environmentally friendly than open-pit or underground mining.6 It involves pumping a solution called a lixiviant into the ground to dissolve the uranium and separate it from the rest of the rock formation. Miners then recover the solution, and after pumped to the surface it undergoes additional processing and concentration to produce a material called yellowcake.7

Uranium can be found in many parts of the world but is top heavy in where the reserves can be found. Countries such as Australia, Kazakhstan, and Canada often lead the uranium production charge, but uranium is present across many nations globally.

Uranium Electricity Generation and Its Advantages

Nuclear power remains one of the few sources of electricity that combines large-scale power output and low greenhouse gas emissions, with costs comparable to those of traditional fossil fuel power stations.8

Similar to coal or natural gas power plants, nuclear reactors generate electricity by producing immense heat. This heat produces steam, which propels a turbine connected to an electric motor. As the turbine rotates, the electric motor produces electricity. In nuclear power stations, however, the heat generated derives from splitting uranium-235 atoms in the process of nuclear fission, as opposed to burning fossil fuels.9

Nuclear fission produces thousands of times more energy than that released through the process of burning similar amounts of fossil fuels, making nuclear power a very efficient method of generating utility-scale power.10 Additionally, the ongoing fuel costs for nuclear power plants tend to be quite low, due to the minimal amount of material needed to power the plant.

In addition to the power density of uranium, nuclear power also ranks among the cleanest methods of producing electricity, as measured by greenhouse gas emissions. The U.S. Environmental Production Agency estimates that 35% of global greenhouse gas emissions derive from electricity and heating (25%), as well as other energy sources (10%), giving nuclear adequate room to lower global emissions, while increasing total share of electricity generation along with wind, solar, hydropower.11

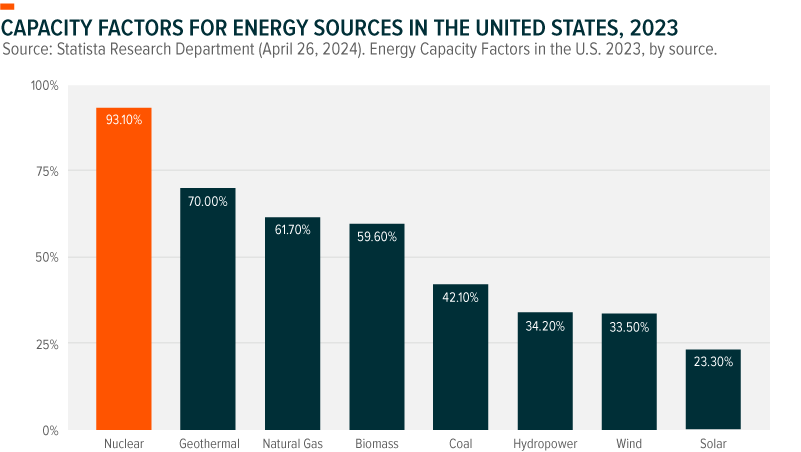

In terms of levelised costs, nuclear power provides a cheaper alternative to biomass, while remaining significantly more cost competitive than offshore wind.12 As a note, while onshore wind and solar are considerably less capital intensive than nuclear, these energy sources tend to be less reliable and qualify as variable renewable energies (VREs). This means they produce energy intermittently, rather than on a demand basis, creating variability in availability when the wind neglects to blow or the sun doesn’t shine. The lower dependency associated with VREs is highlighted when analysing the capacity factor for nuclear against solar and wind.

When comparing power sources with unequal capacity factors, the calculation of the final cost of energy production must include storage costs, since demand spikes and periods of low energy production availability require storage reserves to mitigate blackouts for lower capacity factor sources. The average levelised cost of battery storage is 72.7% more expensive than nuclear, particularly notable given that nuclear plants have achieved almost 3 times greater reliability than wind and solar plants.13 Contrary to popular belief, capacity and electricity generation for various fuel sources do not always align. For this reason, we see nuclear working in tandem with wind, hydroelectricity, and solar, rather than in competition, by helping safeguard energy stability. In addition, the chart below outlines how nuclear produces considerably lower carbon emissions compared to other fixed rate energy sources including coal and natural gas.

The Outlook for Uranium Demand

Nuclear power contributes approximately 10.4% of the world’s total energy supply and serves as a major source of energy in developed markets, such as the European Union (25%) and the United States (19%).14,15,16 Globally, 55 reactors currently under construction would represent a 12.5% increase in nuclear capacity, with an additional 54 reactors planned.17 Reactors in the planning stage represent the second phase after design, while construction marks the final stage prior to being fully operable. The early-stage developments highlight the expanding appetite for nuclear over the past few years. The reactors in the planning stage represent a 30% potential rise in current nuclear capacity, largely led by emerging economies such as China, South Korea, and India.18 Increased demand primarily derives from countries with large populations contending with the dual issues of substantial electricity requirements and escalating air pollution problems, such as India and China. The latter represents the world’s largest market for uranium and China plans to expand its nuclear power capacity significantly. As of February 2024, China has 55 operational reactors, producing an estimated 53.3 gigawatts, with 26 reactors under construction, and an additional 41 planned.19

The Chinese government intends to invest $440 billion in nuclear reactors over the next 15 years, targeting the production of 200 gigawatts of nuclear energy by 2035.20 The monumental project entails building over 150 reactors across mainland China, part of President Xi Jinping’s goal of carbon neutrality by 2060 and peak emissions by 2030.21 China’s plan projects lowering carbon emissions by 1.5 billion tons, more than what the United Kingdom, Spain, France, and Germany currently produce, combined. The International Energy Agency predicts China will triple its nuclear energy capacity in the next 20 years, forecasting China to outpace the European Union and the United States to become the largest nuclear power producer by as early as 2030.22

With larger emerging countries, such as China and India, continuing their extensive nuclear expansion plans, smaller nations such as South Korea, Bangladesh, and Turkey also continue to gain government support for new reactors, with active planning of multiple reactors underway in each country.23 In the developed world, France has announced plans to build six new nuclear power reactors, with an additional eight reactors under consideration.24 The pro-nuclear initiative is part of Macron’s plan to lower the country’s energy consumption while increasing its carbon free production capacity. France also delayed its initial policy goal of reducing nuclear power’s share of electricity generation, allowing extensions to the original 40-year operating life of some reactors, similar to the lifetime extensions used in the United States.25 Europe in general is echoing France’s shift in its stance on nuclear power. In February 2022, the European Commission ruled to label nuclear as a sustainable source of energy, with the announcement aimed at helping raise private capital to meet the E.U. climate change targets.26

These global initiatives delineate the vital role that nuclear energy plays in decarbonisation efforts. The omnipresent shift away from fixed fossil fuels demonstrates the need for an on-demand clean source of energy to achieve net zero goals. Nuclear is a crucial energy source in filling energy production gaps associated with the energy transition. We can see in the United States, for example, nuclear power’s outsized reliability relative to other energy sources.

Uranium Market Status: Still in a Supply Deficit

Uranium supply consists of new production from mining activity and existing inventories, largely from decommissioned nuclear weapons stockpiles. Since 1980, weapons-grade uranium in the United States and the former Soviet Union has been blended down to be repurposed as reactor fuel as part of nuclear disarmament agreements. This steady flow of supply kept uranium prices, as well as mining production, artificially low.

Supply from mining production met approximately 67% of 2021 uranium demand, with the remainder being met with commercial stockpiles, nuclear weapons stockpiles, recycled plutonium, uranium from reprocessing used fuel, and some from the re-enrichment of depleted uranium tails.27 However, the depletion of these secondary supplies are projected to drop to 35 million pounds, or 19% of U3O8 total supply, by 2025 and further reduce to only 11% of total supply in 2030.28 Although this supply stream will contribute towards meeting uranium demand in the near-term, there remained a deficit of 8 million pounds within the uranium market in 2023. In the medium-term (2024-2027), supply deficits should consolidate in the 3-to-14-million-pound range per year, with supply gaps estimated to tighten post-2027, as higher-cost mines and greenfield projects come online.29

The demand side of the equation also looks very promising. UxC, one of the world’s leading sources for data on uranium, projects that the demand for this commodity will grow 21.7%, to over 213 million pounds of U3O8 by 2035, from 175 million pounds U3O8 in 2021.30

Outlook for the Uranium Industry

Uranium prices took a hit following the 2011 Fukushima nuclear disaster, which led to the multi-year shutdown of all nuclear power plants in Japan. Over the past ten years, the global nuclear industry has recovered production of nuclear power beyond pre-Fukushima levels. Japan especially put a concerted effort into restoring its nuclear capabilities, operating a total of 33 nuclear reactors to date.31

Production cuts in early 2019 supported uranium prices, but the investment case has turned even more positive on the demand side since the pre-pandemic environment. Initiatives, including the recent passage of the $6 billion civil nuclear credit program outlined in the nuclear energy provision of the U.S. infrastructure bill and the European Commission’s classification of nuclear as sustainable, are helping establish nuclear power as a key solution in the shift away from fossil fuels and thus influencing uranium demand.32 We believe the policy changes, as well as the supply deficit causing the new sources of demand, support a strong growth outlook for uranium.

The brisk stances taken by governments around the world are also advancing the broader uranium industry. Large uranium producers, such as Cameco and Kazatomprom, as well as small cap miners, can benefit from the shift to uranium. As of 2024, uranium has hit 10-year highs, and as such uranium mining companies have outperformed.33

Investing in Uranium

The nuances of gaining exposure to uranium increase in comparison to dealing in other more commonly traded commodities, such as oil or gold. Common solutions involve purchasing uranium mining stocks or exchange traded funds (ETFs) that own a basket of uranium mining stocks. Another entails gaining access to uranium futures, which trade with relatively light liquidity. Individual uranium mining stocks potentially hold high idiosyncratic risks though, but accessing the industry through a broad basket of uranium mining stocks globally could help mitigate some of these risks. While uranium futures offer exposure to the spot price of uranium, they can be subject to negative returns associated with contango, which occurs when the spot price of a commodity trades below its future price, along with thin liquidity.

Individual stocks also potentially offer somewhat of a levered play on the underlying commodity price, given the high fixed costs associated with mining. Uranium mining stocks maintain a relatively high unsystematic risk, due to the esoteric nature of the industry. For this reason, we believe investing in uranium ETFs may provide an efficient and cost-effective method for accessing a diverse basket of companies involved in uranium mining activities around the world.

Considerations for Investing in Uranium

Despite the upside potential of uranium and nuclear power, there are some risks to keep in mind. In the past, nuclear technologies have caused a number of political, environmental and social issues. The 1986 Chernobyl and 2011 Fukushima nuclear disasters live on in memory for many around the world and brought the safety of nuclear into question. Technological advancements have increased the scalability and safety of nuclear power, however negative perceptions around nuclear and its use in weaponry linger – particularly in the face of geopolitical tensions.

In 2017, the United Nations Treaty on the Prohibition of Nuclear Weapons (TPNW) was enacted to ban nuclear weapon activities, with the ultimate goal of completely eliminating them.34 As a result of the treaty, the nuclear weapon industry saw investment inflows drop by US$63 billion in 2021 compared to 2019, according to a study by the International Campaign to Abolish Nuclear Weapons (ICAN) and PAX.35

Additionally, Uranium mining can have adverse effects on the environment and people’s health, according to the US National Institutes of Health (NIH).36 The NIH highlights three categories of concern.

- Mine site and miner health and safety. Noting, uranium miners are more likely to succumb to “multifactorial health hazards” including lung and other forms of cancer.37

- Health and safety of people in the immediate vicinity who might be affected by the spread of radioactivity.

- Global health and environmental effects of increasing background radiation and water contamination.

When investing in uranium it is important to weigh up these potential concerns and whether this type of investment aligns with one’s risk profile.