When society is presented with new technologies, adoption is rarely determined solely by whether the new option is superior. More often, it hinges on whether the environment is supportive enough, or the economics compelling enough, to justify the switch. Once that threshold is reached, adoption can accelerate rapidly.

With legacy energy systems under pressure amid geopolitical tensions, and volatility increasingly a feature rather than a bug of this new economic era, we believe the moment has arrived for the electric economy - spanning electric vehicles (EVs), lithium, clean energy, and energy storage systems (ESS). EVs and battery technology appear to have finally crossed the threshold of no return, with the next phase of growth set to unfold at a materially faster pace than in recent years.

Key Takeaways

- EV adoption had slowed due to falling petrol prices, upfront price premiums, and limited infrastructure buildout, but all three headwinds have either gradually eased over time or are now being reversed.

- While average all-in costs for EVs had already quietly reached parity with petrol vehicles over the past two years, the energy crisis in the Middle East has now shifted the cost advantage firmly in favour of EVs.

- Nations are now more incentivised than ever to pivot away from reliance on energy imports, toward domestic renewable energy sources and energy storage systems, generating a tailwind for battery tech and lithium.

Need A Spark?

The adoption of a new technology is contingent on a range of requirements ranging from policy support to economics. In the case of EVs, elements such as technological viability, government support and regulation, as well as long-term economics, have largely been achieved and established. However, consumer demand and demographics have been more uneven, with certain regions demonstrating significantly higher levels of penetration than others.

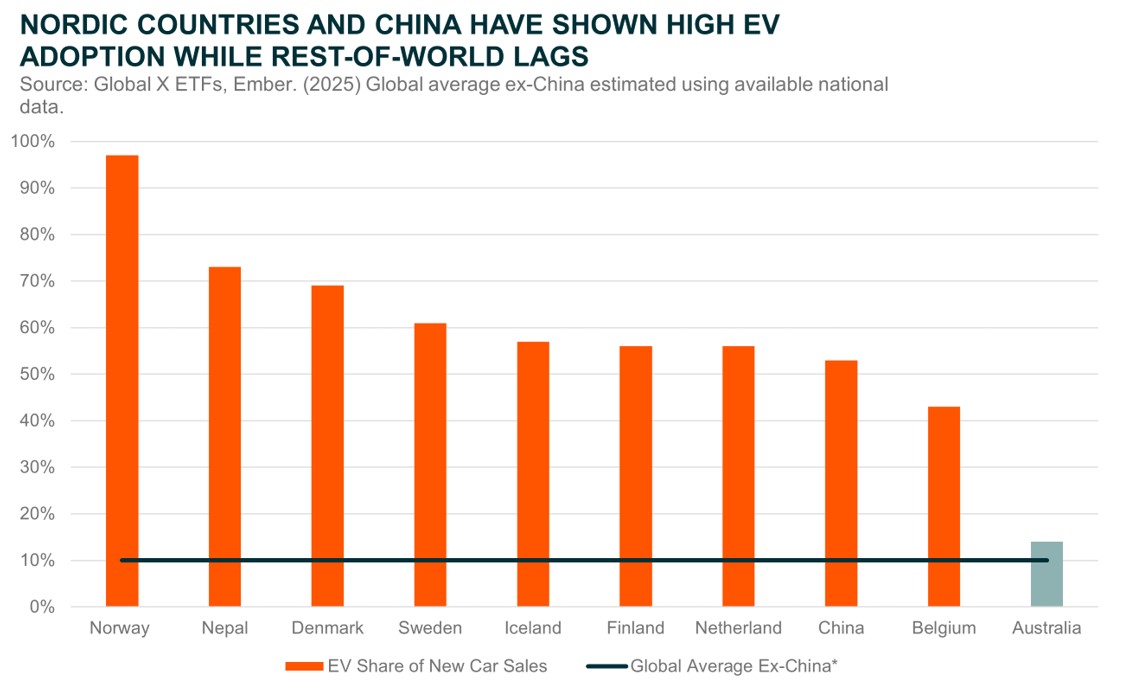

The growth observed in regions such as China and the Nordic countries, has been organic, driven by distinct advantages including lower relative production costs and more advanced infrastructure buildout. For the rest of the world, however, these conditions are less prevalent, and adoption has slowed as EVs have run into dual headwinds: falling fuel prices and a price premium over comparable petrol vehicles.

However, the arrival of an energy crisis in the form of the Iran War may prove to be the catalysts that re-ignites the fire under EV adoption.

The Logical Consumer

Cost parity has long been hailed by both consumer media and investors as the key inflection point for EV adoption. The logic is straightforward: as EVs become just as cheap to buy and own as petrol vehicles, their superior technology and day-to-day performance should be enough to drive widespread switching.

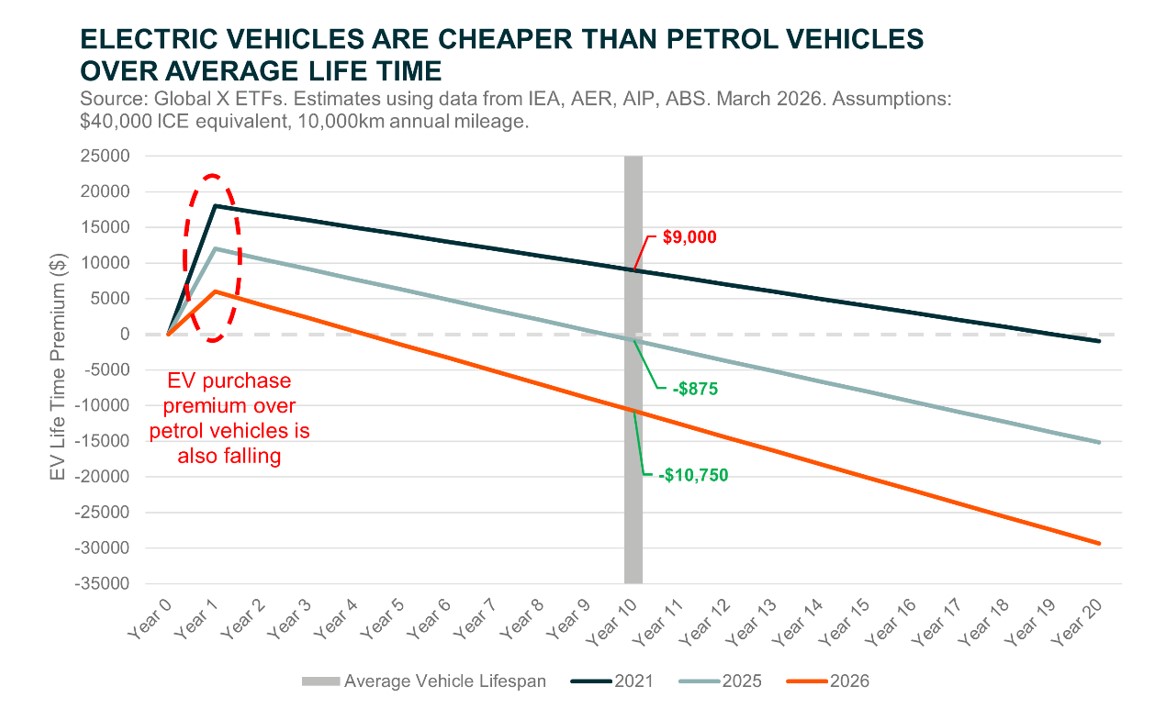

However, we believe this is most likely not sufficient. What this framework overlooks is the stickiness of ingrained consumer behaviour, including a natural scepticism toward new technologies. For example, according to our analysis, the average all-in cost of an EV in 2025 was already approximately $875 cheaper than that of a comparable petrol vehicle over a typical 10-year ownership period.

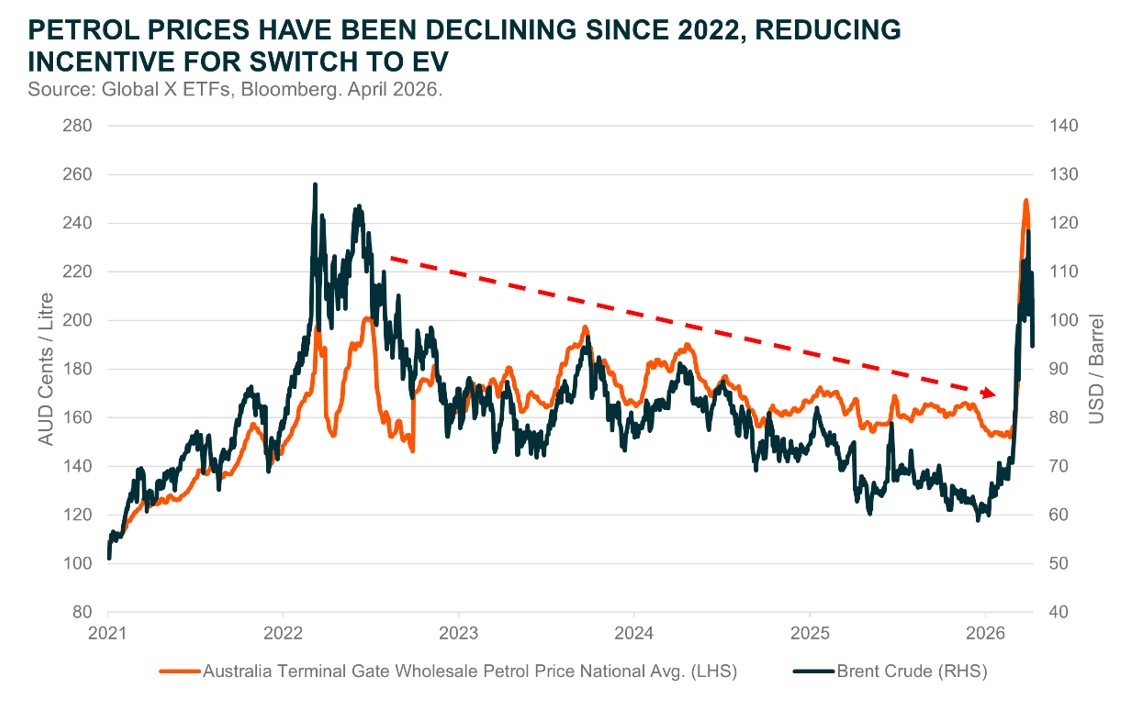

What is actually necessary then, is a large enough comparative advantage - usually economic - that it becomes illogical not to switch. And with petrol prices sitting multiple standard deviations above their long-term average, that moment appears to have arrived. The same analysis that showed EVs were on par with petrol vehicles in 2025 now estimates that the all-in cost of an EV is more than $10,000 cheaper than a petrol vehicle over an average ownership period of 10 years. Suddenly, what used to be a decision based on preference, has become a matter of economic logic.

Further, the repeated volatility in fuel prices has likely ingrained a shift in consumer expectations, reinforcing the view that low petrol prices are not something to rely on. The Iran War marks the second major conflict in five years, alongside Russia-Ukraine, to directly disrupt fuel markets. As such, even if the economic advantage of EVs over petrol vehicles narrows as prices normalise, consumers may still view EVs as a practical hedge against future energy price shocks.

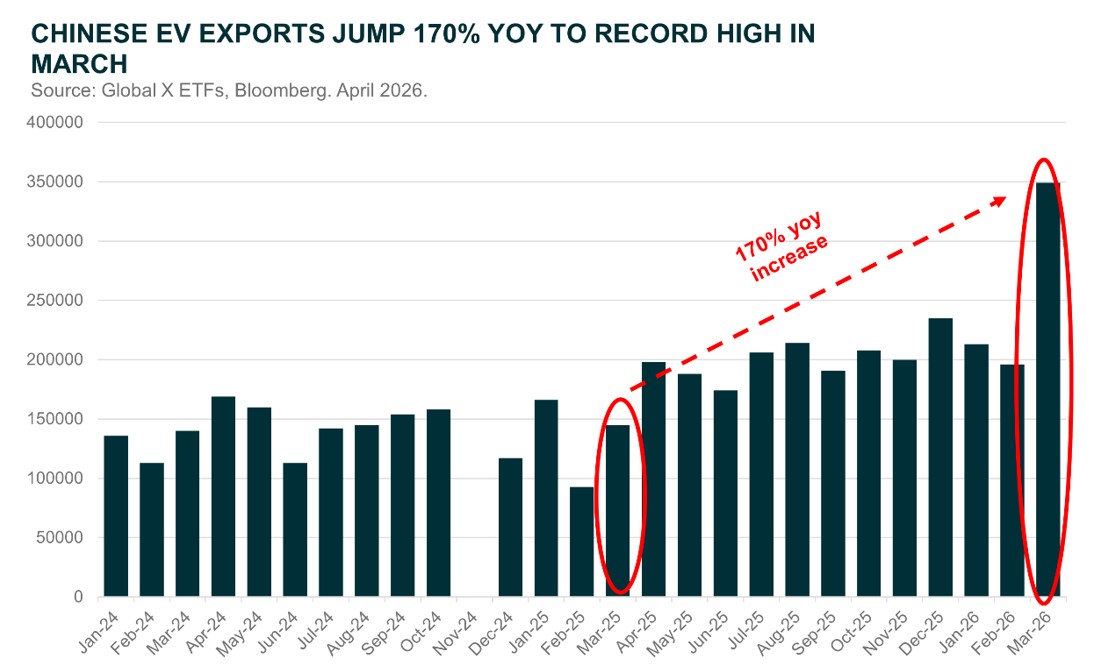

As of April 2026, the first signs of the EV re-acceleration are already appearing in sales figures and export numbers. Australia saw EVs take its highest share of sales ever in March, and in a more global metric, Chinese EV exports for March jumped more than 170% year-over-year.1

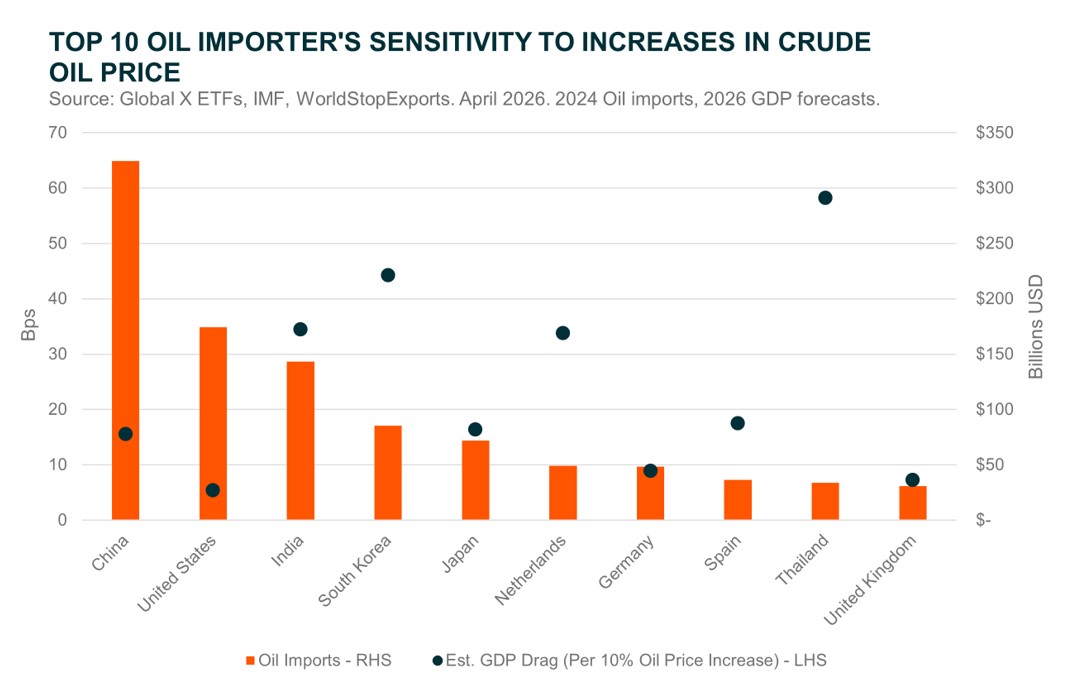

Grappling With Energy Security

In the same way that consumers are increasingly incentivised to reduce their exposure to petrol price fluctuations, nation states have also had a rude awakening to the risks of over-reliance on energy imports.

It has become increasingly clear in recent years, particularly following President Trump’s return to power, that the world is moving along a path of deglobalisation. As a result, commodities, including energy, are becoming more politicised and increasingly vulnerable to disruption. The Iran War has merely exposed these vulnerabilities and may act as a catalyst for countries to address and better manage risks in the future.

For most nation states without reliable domestic access to energy resources, the rational response is to accelerate investment in renewable infrastructure such as wind and solar. Central to this buildout are Energy Storage Systems (ESS), which not only store excess generation but also smooth out the inherent intermittency of renewable supply.

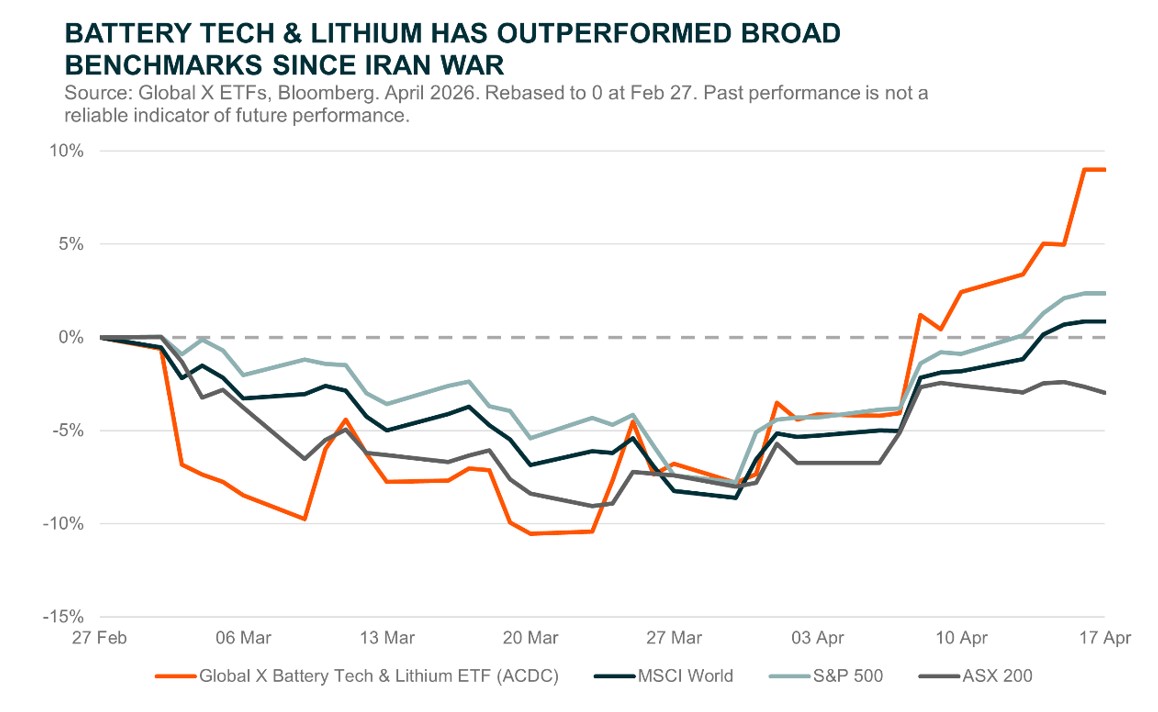

While governments typically move more slowly due to political constraints and election cycles, the scale of their capital deployment far exceeds that of even the largest institutions. Markets tend to anticipate and front-run these strategic shifts, which may help explain why the Global X Battery Tech & Lithium ETF (ACDC) rebounded to pre-war levels faster than broader benchmarks and has continued to outperform.

Conclusion: Re-accelerating Adoption

The EV story has long been framed around cost parity, infrastructure, and policy support. Those pieces are now largely in place. What has been missing is a catalyst strong enough to break inertia. Recent geopolitics, and the broader structural instability it represents, may be that catalyst.

What began as a cyclical shock to energy markets is increasingly shaping structural behaviour. For consumers, EVs are no longer just a cleaner or more advanced alternative, but a rational hedge against persistent fuel price volatility. For governments, the imperative is even clearer. Energy security has moved to the forefront, accelerating the shift toward domestic renewable generation and storage.

This alignment of consumer economics and national strategy is what typically defines true inflection points in adoption curves. While the pace of change may not be linear, the direction of travel appears increasingly set. The electric economy is no longer reliant on favourable conditions to grow. It is being pulled forward by necessity.

Related Fund

ACDC: The Global X Battery Tech & Lithium ETF (ACDC) offers investors exposure to global companies developing electro-chemical storage technology and mining companies producing battery-grade lithium.