For the past few decades, the global economy ran on a single organising principle: efficiency. Supply chains stretched across continents in pursuit of the lowest-cost producer, capital flowed freely across borders, and governments outsourced strategic industries to markets, trusting that price signals would allocate resources better than policy ever could. The costs of that fragility remained invisible for a long time.

They became visible in sequence. A pandemic exposed just-in-time supply chains as a liability. A land war in Europe repriced energy security in weeks. Trade restrictions multiplied at a pace not seen since the 1930s. What replaced the old order was not a correction but something genuinely new, a world in which governments and corporations are deliberately building redundant capacity, paying a premium for domestic control, and treating strategic industries as sovereign assets rather than market commodities.

This is the regime shift that HALO 1.0 identified at the asset level. HALO 2.0 goes one layer deeper, asking not just what kind of assets win in this world but why the demand for them is structural, sovereign, and still in its early innings.

Key Takeaways

- The pre-2020 global system optimised for efficiency, but the post-2020 system is being rebuilt around security, redundancy, and sovereign control in a shift that is structural rather than cyclical.

- Governments are now treating supply chains, energy systems, and digital infrastructure as national security assets, driving strategic capital deployment that does not depend on the economic cycle to sustain it.

- The result is a multi-decade repricing of physical capital, where the assets underpinning sovereign capability are being funded at a scale the market has not yet fully priced.

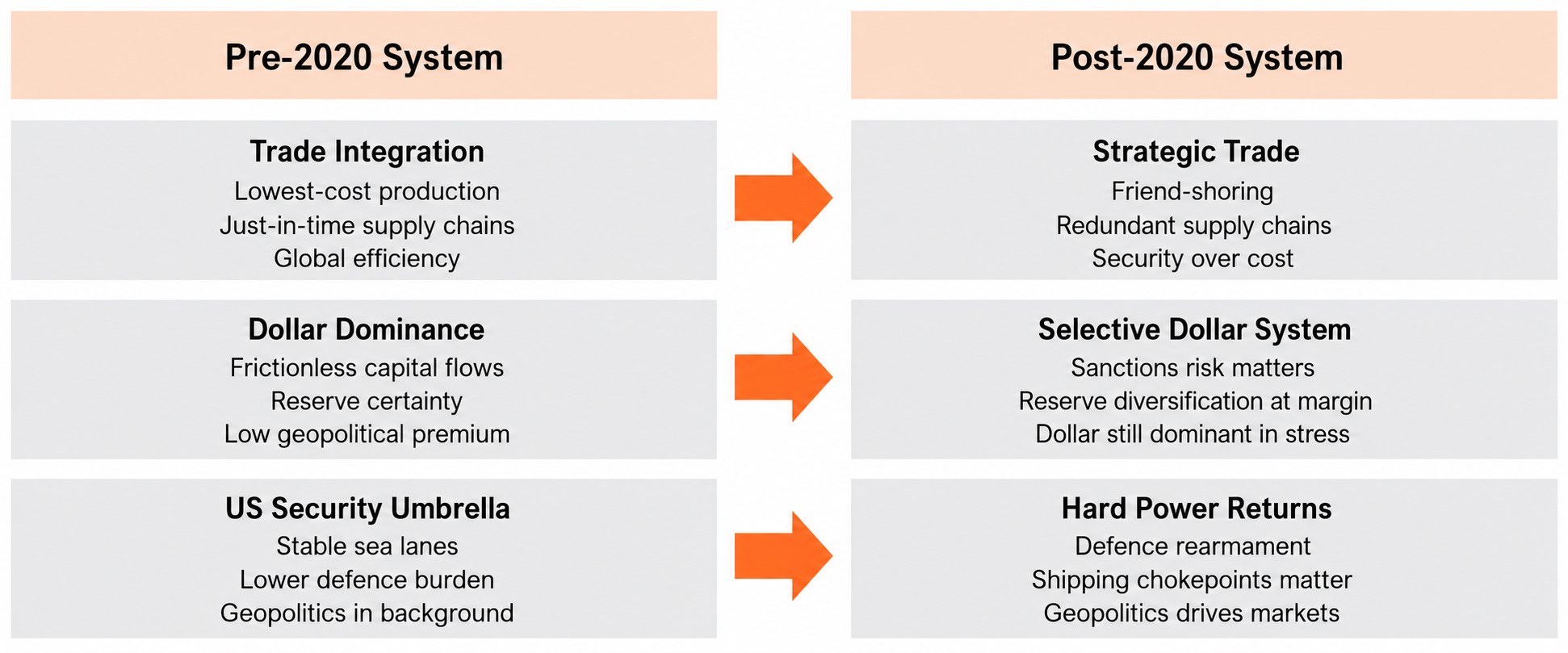

The Global System Is Being Rewritten

The world that existed before 2020 was built on three interlocking assumptions. Trade would continue to integrate, with production flowing to wherever it was cheapest. Capital would move freely, with the dollar at the centre of a frictionless global system. And security would remain a background condition, underwritten by US power at a cost low enough that most nations could largely ignore it.

All three broke down within a few years of each other. The pandemic revealed how deeply the pursuit of efficiency had hollowed out the redundancy that resilience requires. The war in Ukraine demonstrated that geography matters, that pipelines can be weaponised, and that dependence on a single supplier is a strategic liability. And the acceleration of trade restrictions made clear that the frictionless global trading system was a political choice that could be reversed, not a permanent feature of the landscape. What has replaced it is a system organised around a different principle entirely, one in which governments are no longer asking which supplier is cheapest but which supply chains they can control and what it costs to own strategic capacity rather than rent it from the global market.

Source: Global X ETFs

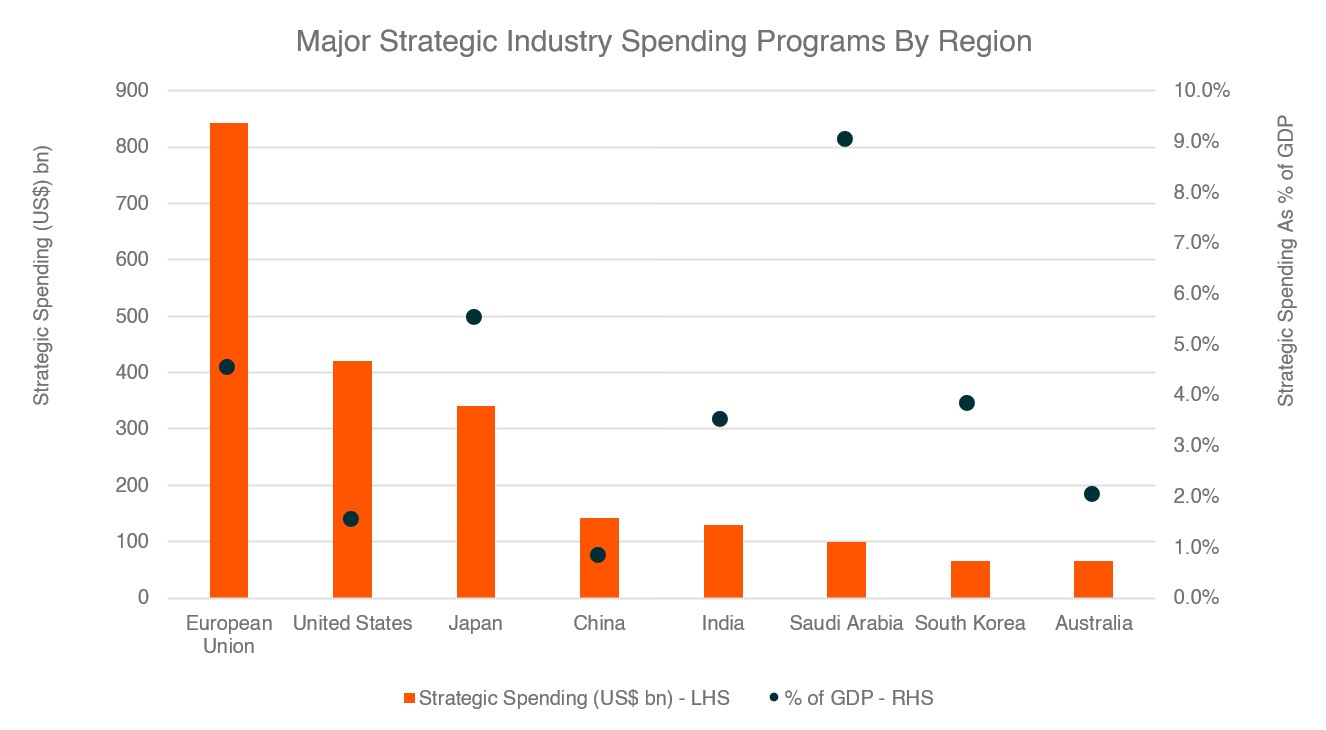

Sovereign Capital Is Flowing at Scale

The shift from efficiency to security is being expressed in legislation, budget commitments, and industrial policy across every major economy simultaneously, at a scale that has no modern precedent outside of wartime.

In the United States, the Infrastructure Investment and Jobs Act (IIJA), the CHIPS and Science Act, and the Inflation Reduction Act collectively authorised more than US$2 trillion toward domestic physical capacity, semiconductor manufacturing, and clean energy infrastructure, with deployment continuing across administrations at varying pace and scope. In Europe, the ReArm Europe program is directing hundreds of billions toward defence and strategic industrial capability, with the EU alone committing close to US$900bn in strategic industry spending representing nearly 9% of GDP. Japan, South Korea, India, and Australia have each launched their own versions of the same trade, strategic industry programs designed to reduce dependence on foreign supply and build domestic capacity in sectors deemed too important to leave to the market. These are not stimulus packages designed to smooth a cyclical downturn but structural commitments to sovereign capability that will take years to deploy and decades to depreciate, with less than a third of committed IIJA funds deployed as of mid-2026 and ReArm Europe still in the planning and contracting phase across most member states.

Notes: US = CHIPS Act + IRA; EU = European Chips Act + ReArm Europe; China = semiconductor self-sufficiency programs; Japan = semiconductor reshoring + defence modernisation; South Korea = K-Semiconductor Strategy; India = semiconductor incentives + defence localisation; Saudi Arabia = Vision 2030 industrial diversification; Australia = National Reconstruction Fund + defence capability investment.

Sources: White House, European Commission, Reuters, State Council of China, METI Japan, MOTIE Korea, Government of India, Saudi Vision 2030, Australian Budget Papers.

The Cost of Security Is Rising, and Markets Are Still Pricing It In

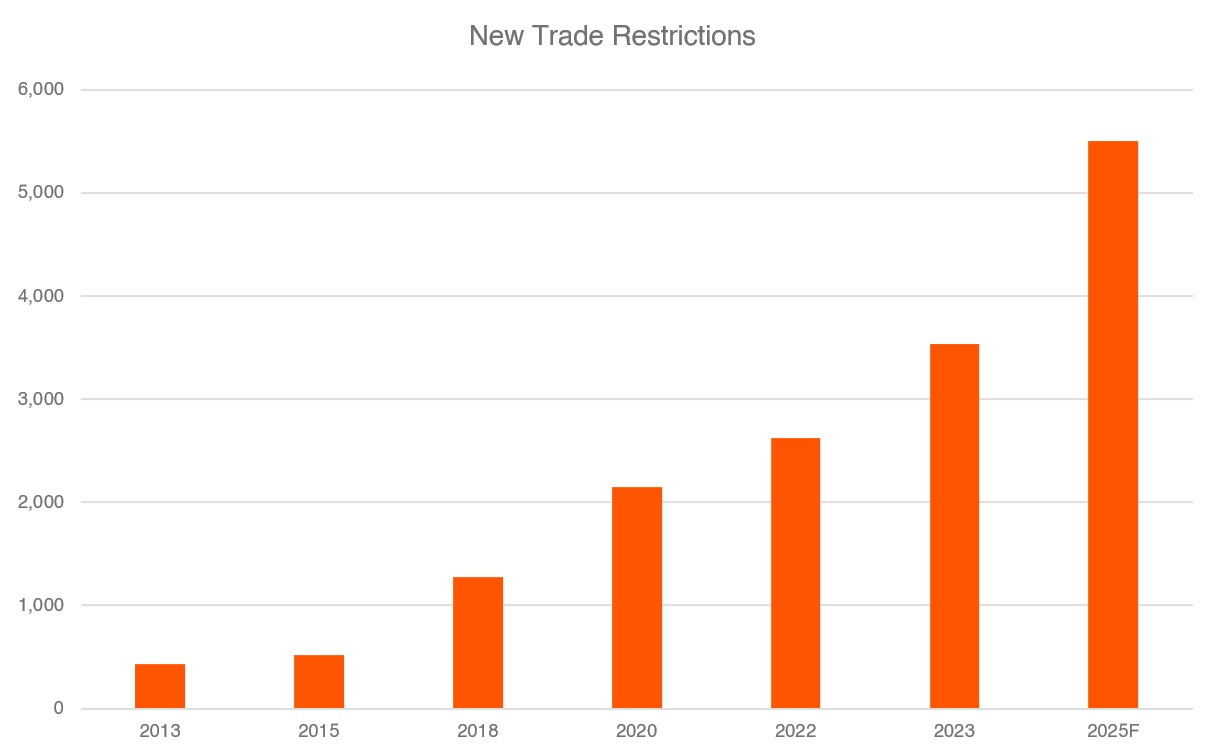

Trade fragmentation is not just a supply chain story. It is a repricing of risk that flows through every layer of the global economy. New trade restrictions have grown from under 500 annually in 2013 to more than 5,000 by 2025, a tenfold increase in little over a decade, as tariffs, export controls, investment restrictions, and sanctions became routine instruments of economic policy rather than exceptional measures.

For investors, this changes the return profile of physical capital in a way that traditional valuation frameworks do not fully capture. An asset that is strategically necessary commands a different kind of demand than one that is merely economically useful, because governments will fund it, protect it with regulation, and support it through downturns in ways that pure market dynamics would not. The pre-2020 framework penalised over-investment in physical capacity because global markets could always supply it more cheaply. The post-2020 framework penalises under-investment because the cost of not having it has become visible, measurable, and politically unacceptable.

Notes: Includes tariffs, export controls, subsidies, sanctions, investment restrictions and localisation measures. Sources: United Nations DESA, IMF, Global Trade Alert, WTO.

Accessing the Sovereign Capital Cycle

The regime shift expresses itself differently depending on which layer of the sovereign capital cycle an investor wants to access, and three products capture the most direct expressions of it.

Hard power returning means defence spending is no longer a discretionary budget line but a floor with a political mandate to rise. The Global X Defence Tech ETF (DTEC) captures this layer, with exposure to the companies building the systems and technologies that governments across NATO, Asia, and the Indo-Pacific are now committing to fund at scale. Domestic physical sovereignty means the infrastructure underpinning economic activity is being treated as a strategic asset rather than a maintenance liability, and the Global X US Infrastructure Development ETF (PAVE) captures this layer through the US contractors, engineers, and materials companies executing the largest domestic infrastructure investment cycle in a generation. Compute sovereignty means AI infrastructure has become a national security consideration, with data centre capacity, power infrastructure, and the physical networks supporting AI workloads now treated as sovereign capability, and the Global X Artificial Intelligence Infrastructure ETF (AINF) captures this layer through the energy, grid, and infrastructure companies building the physical backbone of the AI economy.

Held together, DTEC, PAVE, and AINF are not three separate thematics competing for the same dollar. They are three expressions of a single structural shift, each capturing a different dimension of what it means to invest in a world that has decided security is worth paying for.

The global system is being rewritten, and the assets being built to support it are already known.