The global defence industry is undergoing a structural transformation that extends well beyond the cyclical budget debates the market has historically used to price the sector. Two concurrent conflicts have exposed the limits of Western defence production capacity and depleted interceptor and munitions stockpiles that took decades to build. They have also demonstrated that the adversary production base is scaling faster than the West can replenish, with Russia, China, and Iran collectively outspending the US on a purchasing power parity basis for the first time in modern history1.

The sovereign capital thesis we laid out in The Security Premium identified a world in which governments are no longer asking which supplier is cheapest but which supply chains they can control and what it costs to own strategic capacity rather than rent it from the global market. Defence technology sits at the sharpest edge of that thesis. This piece examines why the spending cycle now underway is non-discretionary regardless of political outcomes, why the supply-side dynamics reshaping global procurement are structural rather than temporary, and why the market has yet to fully price the earnings trajectory that follows.

Key Takeaways

- The market applied peacetime budget uncertainty to a wartime spending environment, mispricing defence equities at the exact moment the structural case for owning them was being validated on the battlefield.

- The industrial gap between Western production capacity and adversary output has made the rearmament cycle non-discretionary, with the spending trajectory now set by the adversary production base rather than by domestic political preferences.

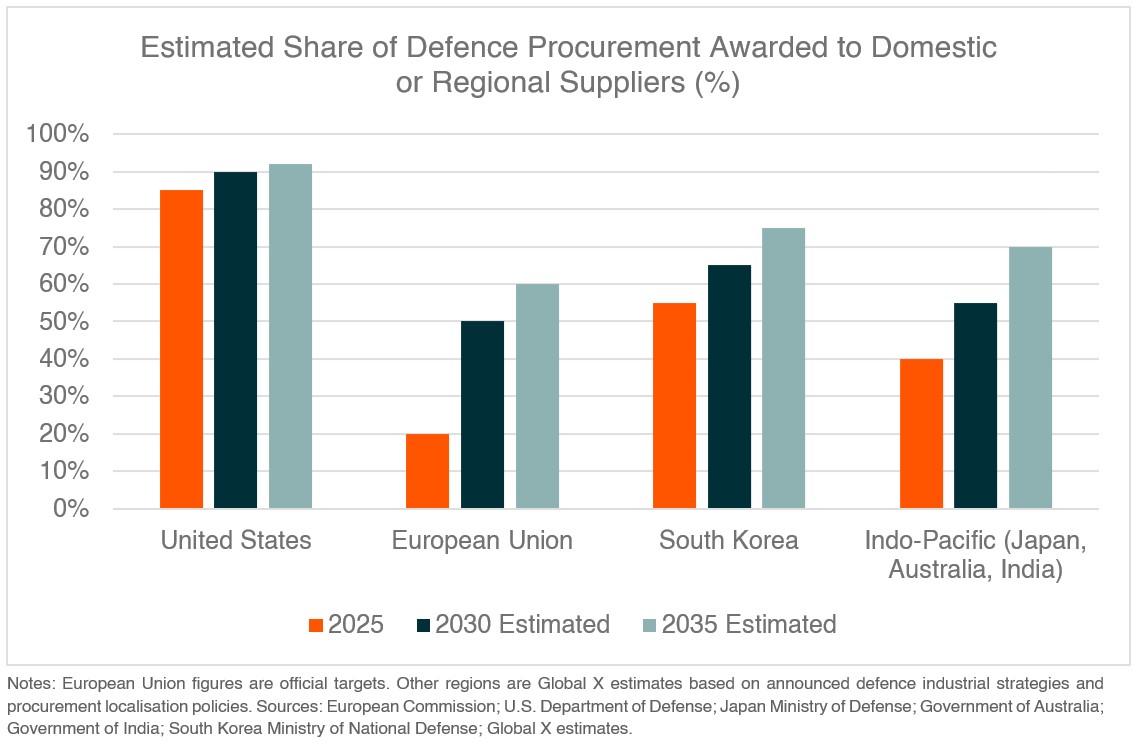

- US production saturation through 2029 is redirecting defence procurement toward European and Indo-Pacific manufacturers at a scale and pace the market has not yet priced2.

Wars spend. Peacetimes budget.

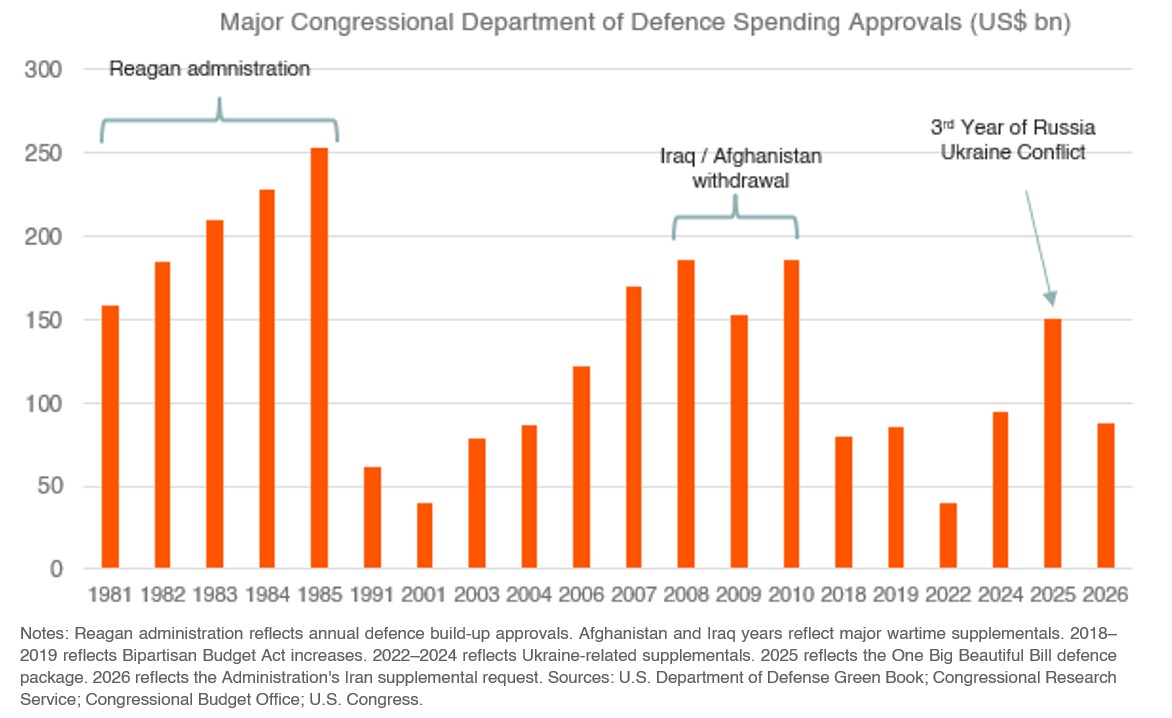

During active conflict, defence spending rarely waits for the annual budget process because governments have little choice but to sustain military operations. Existing inventories are drawn down, emergency procurement authorities are activated and operations are financed through supplemental appropriations alongside the annual defence budget. The immediate priority is maintaining military capability rather than debating long-term force structure. It is only once the immediate operational demands begin to stabilise that governments typically shift their attention towards replenishing depleted inventories, expanding industrial capacity and addressing capability gaps exposed during the conflict. As history has shown, many of the largest structural defence funding commitments have been announced during these periods of strategic reassessment, including the Reagan military build-up in the early 1980s, the post-sequestration increases under the Trump administration and the current wave of NATO and European rearmament initiatives3.

The market appeared to get this distinction backwards during the first half of 2026. Defence companies fell roughly 22% from the start of the Iran hostilities while the S&P 500 rallied around 10%, reflecting investor concerns over the stalling reconciliation bill, the compressing midterm calendar and the prospect of a ceasefire4. Yet the underlying demand signal was never in question. Missile interceptors, precision-guided munitions and other critical systems were being consumed in real time across the Middle East while inventories continued to decline and governments were already preparing the next phase of defence spending. Rather than removing the case for defence investment, the ceasefire shifted the policy focus from financing current operations towards replenishing stockpiles, expanding production capacity and modernising military capability. History suggests that it is these periods of strategic reassessment, following the identification of capability gaps, that have often supported some of the largest and most enduring structural defence funding commitments.

The Industrial Base Is No Longer Sufficient

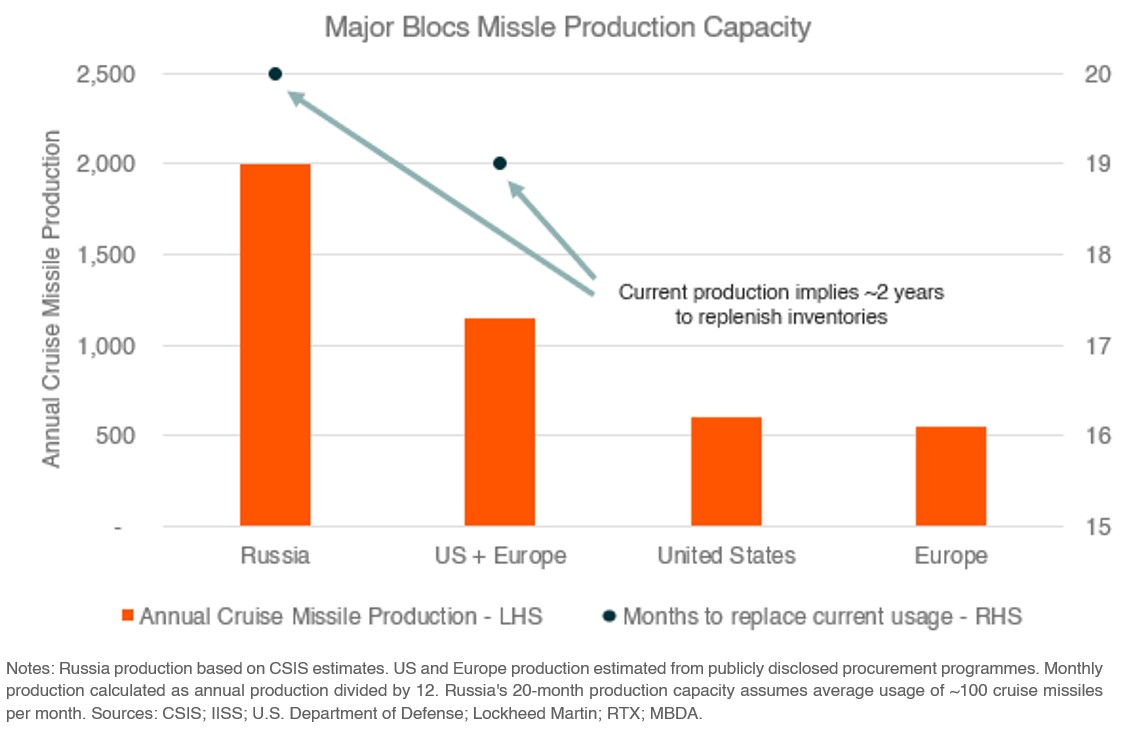

The rearmament cycle now unfolding across the US, Europe and the Indo-Pacific is being driven less by domestic political preferences than by the reality that Western defence industrial capacity is no longer sufficient to meet the demands of an increasingly contested security environment. Whether a particular reconciliation package passes or which party controls Congress may influence the timing and composition of spending, but it is unlikely to alter the broader direction of travel. Russia produces roughly 2,130 cruise missiles per year, nearly double the combined output of the US and Europe, and even while launching roughly 100 cruise missiles per month into Ukraine, Russia is still able to build inventory rather than deplete it5. At current production trajectories, Russia could hold a cruise missile stockpile more than double Europe's within a decade, a gap that makes continued underinvestment in Western defence production an increasingly untenable position for any government regardless of its fiscal priorities.

On a purchasing power parity basis, Russia, China, and Iran collectively began outspending the US on defence in 2023 for the first time in modern history, and even the full US$1.5tn FY27 budget request would only restore the spending ratio to roughly 1.3x, equivalent to conditions in 2014 and well below the 2000-2024 average of 1.7x. The conflicts in Ukraine and Iran have simultaneously drawn down US interceptor stockpiles by 25-45% in a matter of weeks6, consuming between 1.5 to 3 years of production output depending on the system. The FY27 budget request reflects the scale of the response: missiles and munitions procurement is up 189% YoY, total modernisation funding is up 73%, and the US$1.5tn headline figure represents the largest defence budget in US history. In Europe, NATO's stated target of increasing air defence capabilities by 400% translates into an estimated US$390bn opportunity for global suppliers through 2035, a figure that already adjusts for existing inventories7.

Production Constraints Are Reshaping Procurement

The third dynamic the market has yet to fully price is how production constraints are reshaping global defence procurement. US interceptor orders placed in 2026 and 2027 are projected to saturate domestic production capacity through 2029, creating a structural bottleneck that is already forcing European customers to look elsewhere. Switzerland has been told deliveries of Patriot, the US-made surface-to-air missile defence system, could slip four to five years to 2030-328, and defence officials have publicly stated they are evaluating European alternatives and may cancel the purchase entirely if binding delivery dates are not provided. Around US$30bn of outstanding European Patriot contracts face similar delay risks, with lead times extending to as long as 14 years from contract signature to delivery9.

This is no longer a question of European strategic autonomy but a supply-driven reality already visible in contract awards, where 45% of medium and long-range air defence orders are now being awarded to EU manufacturers compared with roughly 20% of existing inventories. The European Commission has set targets of 50% intra-EU procurement by 2030, rising to 60% by 203510, while European manufacturers broadly plan to double production capacity over the next decade. The Global X Defence Tech ETF (DTEC) is positioned across both sides of this shift, holding US primes expanding domestic production alongside European and Indo-Pacific companies benefiting from demand redirected by US capacity constraints. Despite air defence and missiles dominating the defence narrative in 2026, European defence equities are up only 2% year to date and US defence 3%, suggesting much of the structural opportunity remains ahead of the market rather than already priced in11.

Accessing the Defence Technology Cycle

Defence equities sold off in the first half of 2026 because the market was watching the wrong signal. It tracked the budget process while the spending was already happening, it priced the ceasefire as a reduction in demand rather than the beginning of the replenishment cycle that historically drives defence earnings, and it derated the next-generation technology companies at the exact moment their capabilities were being proven in combat. None of those dynamics have reversed. The industrial mismatch with adversaries is widening, not narrowing. The production bottlenecks in the US are redirecting procurement globally rather than constraining it. And the budget debates that investors were waiting for are now entering peacetime, which is when defence authorisations have historically been approved at their most ambitious scale. Profit-taking after 2025's sharp gains is a near-term risk, but it reflects valuation discipline, not a reversal of the underlying procurement cycle.

The Global X Defence Tech ETF (DTEC) is designed to capture this cycle, providing exposure across the full defence technology stack in a single allocation. The fund holds companies across the US, Europe, the Middle East, and the Indo-Pacific that are positioned on both sides of the procurement shift now underway, giving investors access to a structural spending cycle that is global in scope, multi-year in duration, and increasingly non-discretionary in nature. The market has not yet priced the earnings trajectory that follows, and for investors willing to look through the noise of the budget process to the reality of what is being built underneath it, DTEC offers a way to access it.

Considerations for investing in DTEC

As with all investments, an investment in DTEC has risks - see the PDS for more information. This fund may expose investors to currency risk, sector risk, concentration risk, and/or market risk. Different investment strategies carry different risks, depending on the assets that make up the strategy. The value of your investment may fall, you may receive back less than your original investment.