The market has largely framed AI through its development phase, focusing on building models and scaling compute. That framing is becoming incomplete. As model capability stabilises and usage scales, the next phase of the cycle is being driven by deployment, where hardware, components, and industrial systems become central to translating AI into productivity. This is not a replacement of the first phase but an expansion, with value dispersing across a broader set of industries beyond models and compute.

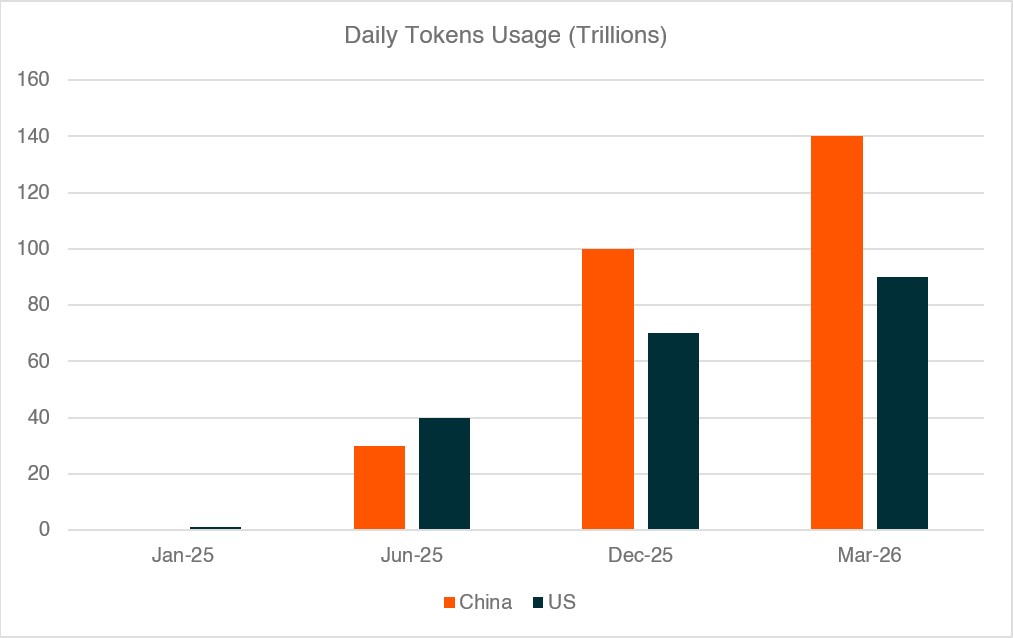

China provides one of the clearest views of how this transition is unfolding. Constraints on advanced chips have pushed developers toward more efficient model architectures, while daily token usage in the country has surpassed 140 trillion in March 2026, more than 1,000 times the level at the start of 20241. Robotics and automation systems are progressing from proof-of-concept toward early commercial deployment, supported by manufacturing scale and policy alignment around industrial upgrading. Taken together, these developments point to a system that is beginning to operate, not just one that is still being built.

Key Takeaways

- AI is shifting from build to deployment, with daily token usage in China up over 1,000 times since early 2024.

- Value is dispersing beyond software into hardware, components, and industrial systems, with humanoid robotics potentially reaching a multi-trillion-dollar market by 2050.

- China sits at the centre of both layers, supplying the tech stack and anchoring the global humanoid value chain.

From Capability to Usage: The Shift Already Underway

The initial phase of the AI cycle was defined by rapid gains in model performance and significant investment in compute infrastructure. This phase produced a concentrated set of winners and shaped investor perception of where value would accrue. The drivers are now changing.

In China, limited access to leading-edge chips has forced a focus on efficiency. Developers are building models that require materially less memory and compute while maintaining competitive performance. The progression of DeepSeek's recent open-source releases illustrates the scale of this shift, with each new version cutting inference compute requirements while extending context length and reducing token pricing (see table below).

Source: DeepSeek; NVIDIA; Artificial Analysis

Note: Inference FLOPs measure the compute cost of generating each token. Context length is the amount of information the model can process in a single request.

This trend is not isolated, inference costs are compressing across the industry, but China’s efficiency-led approach is accelerating the pace of decline.

The efficiency gain has translated into deployment at scale. China's daily token usage surpassed 140 trillion in March 2026, more than 1,000 times the level at the start of 2024, with Chinese AI models having overtaken US models on global usage platforms in February 20262. ByteDance's Doubao alone now processes 120 trillion tokens daily, doubling in three months. The build-out also has room to run. China hyperscalers are deploying capital at around 60% of operating cash flow, compared with closer to 90% at US peers, leaving meaningful capex headroom into 2027 and beyond3.

Source: National Data Administration of China; company disclosures (OpenAI, Google, Microsoft, Anthropic)

Note: US daily token usage estimated from public disclosures by OpenAI, Google (Gemini), Microsoft (Azure OpenAI), and Anthropic. China daily token usage as reported by the National Data Administration of China. Figures are approximate and based on the latest available disclosures for each period.

This combination of efficiency, usage, and funding capacity is lowering the cost of intelligence to a point where deployment is becoming economically viable, shifting the focus away from how much capability can be built toward how effectively it can be applied across industries.

Deployment Requires Systems, Not Just Models

As the cost of intelligence falls and usage scales, the constraint shifts from capability to deployment. AI software is already driving early productivity gains, but the next phase of impact requires systems that can operate in physical environments and deliver consistent outcomes over time. This is where robotics and automation move from adjacent themes into the centre of the AI investment case. This is already visible in robotics, where systems are moving from proof-of-concept into scaled pilots and early commercial deployment.

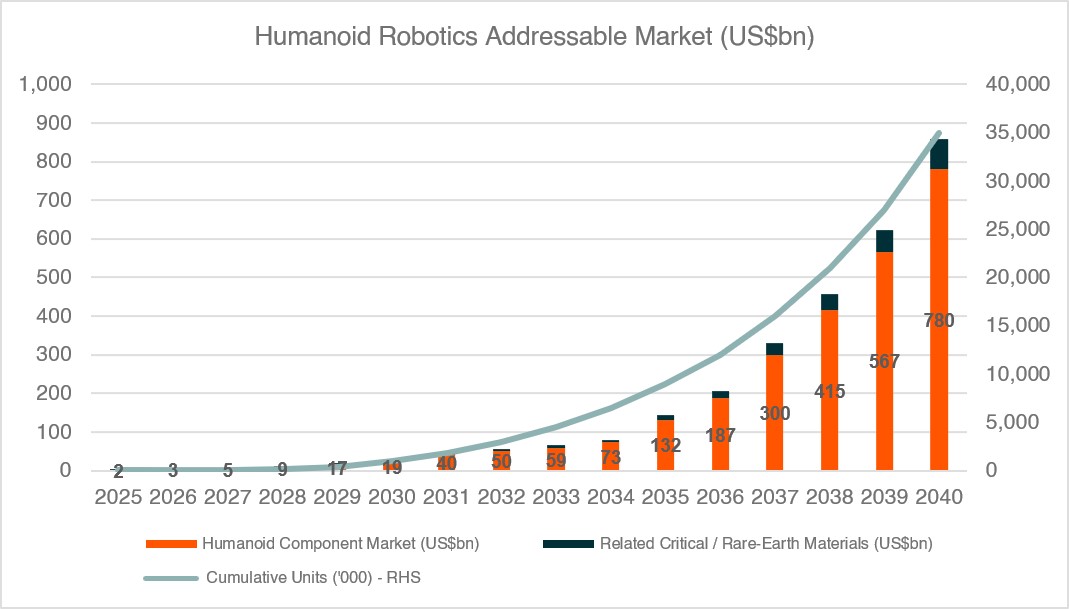

The economic prize justifies the framing, with global labour representing roughly a third of the world's US$117 trillion GDP and the addressable market for robotics and supporting systems likely reaching tens of trillions of dollars as adoption scales4. This build-out is also input-intensive, with critical materials such as rare earths playing a central role in motors, actuators, and precision components that underpin humanoid systems.

Historical precedent reinforces this, with the automobile having multiplied the transportation market many times over rather than taking share from the horse, and fixed-wing aircraft having expanded the addressable market for flight by orders of magnitude beyond the blimp. Humanoid robotics carries similar expansion potential, with new unit sales likely to represent only part of the eventual revenue pool alongside a longer tail of services, parts, software, and supporting infrastructure.

Source: International Federation of Robotics, Morgan Stanley Research

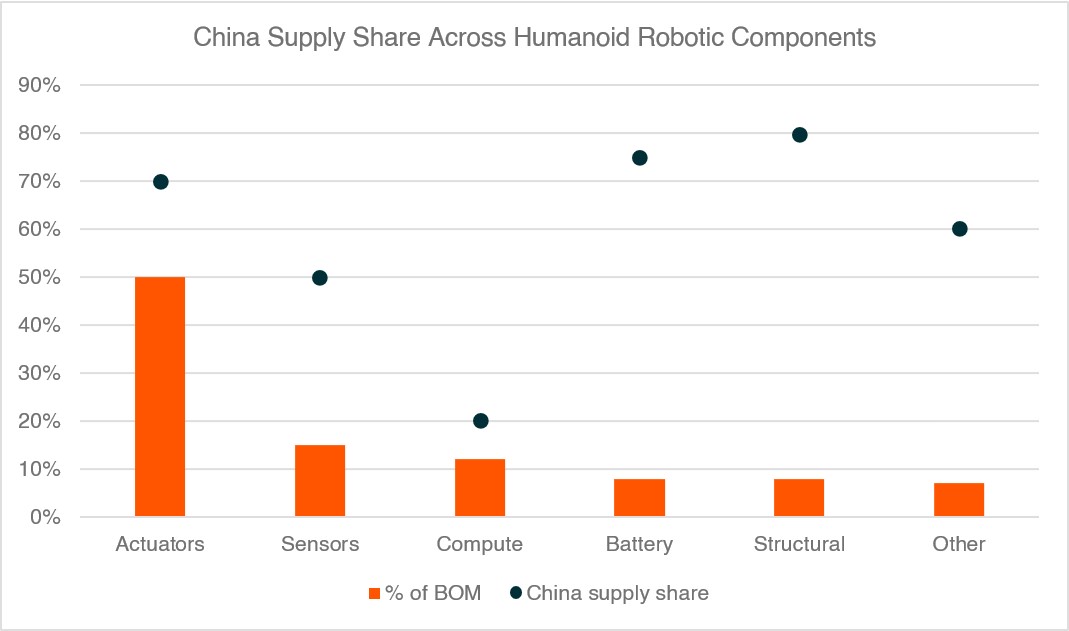

Value is also distributed across the full stack rather than concentrated at the end-product level. High-barrier components such as actuators, harmonic reducers, sensors, and motion control systems are critical to performance and durability and are positioned to capture meaningful share as adoption scales. Multi-modal AI capability sits alongside the hardware layer, with vision-language-action models forming the cognitive bridge that allows robots to operate in unstructured environments. Several of the leading multi-modal video generation models globally now sit with Chinese developers, reinforcing China's position across both the physical and intelligence layers of the system.

China's Position Across the Stack

China's role in this transition is often framed in relative terms against the US. The more relevant observation for investors is that China is progressing across multiple layers of the system simultaneously.

At the model level, the gap with leading global systems is narrowing on pricing, speed, and task execution, while efficiency-led development is creating a differentiated competitive dynamic. At the component level, China's industrial base supplies a large share of the precision parts that humanoid systems depend on. Domestic manufacturers of harmonic drives, servo motors, machine vision, and end-effectors form a dense supplier network that has scaled through the EV and consumer electronics cycles. Policy continues to prioritise AI, robotics, and automation as structural growth areas, supported by capital allocation and industrial strategy5.

This combination of model capability, component depth, and industrial capacity means China is not only developing AI but also producing the physical components that allow it to operate as a system.

Source: McKinsey; Yole Group; Morgan Stanley; SemiAnalysis

Note: BOM = Bill of materials cost = total expense of all raw materials, components, sub-assemblies, and parts required to manufacture a single unit of a product.

Capturing the Opportunity

The next phase of AI will be defined by deployment rather than development. As capability becomes more accessible and usage continues to scale, value is dispersing across the industries that enable real-world application, and China sits across both layers.

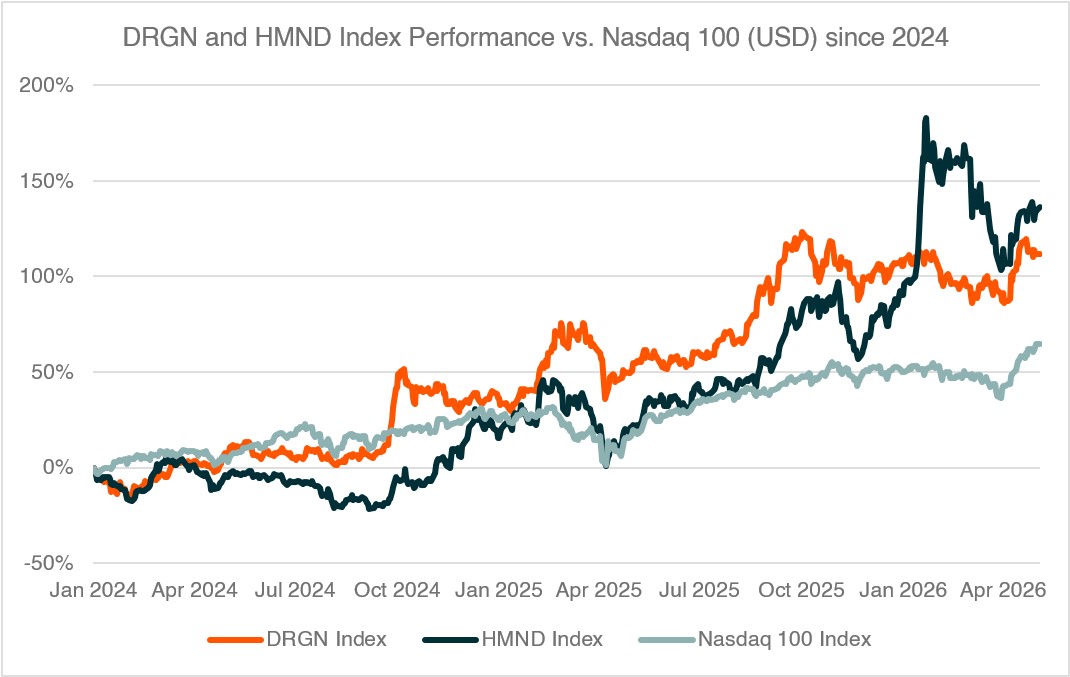

That creates two complementary ways to access the opportunity. The Global X China Tech ETF (DRGN), which tracks the Global X China Tech 20 Index, captures the technology stack, with 20 leading Chinese companies across AI, semiconductors, software, electronics, and automation. It is one of the cleanest ways to express a view on China's self-sufficient innovation cycle, where efficiency-led AI development, domestic chip ramp, and platform leadership are converging into a re-rating of the broader Chinese tech complex. The Global X Humanoid Robotics ETF (HMND) captures the application layer, with global exposure across humanoid systems, industrial robotics, AI integration, and advanced hardware. Around a third of HMND's holdings are Chinese-listed or Chinese-domiciled, reflecting the centrality of China's component and mechatronics base to the global humanoid build-out, but the product also captures the leading developers, integrators, and component suppliers in the US, Korea, and Japan.

Source: Bloomberg data as of 4 May 2026. You cannot directly invest in an index. Past performance if not a indicator of future performance.

The two products work as standalone allocations and as a pair. Investors looking for direct exposure to China's strategic technology push can hold DRGN. Investors looking for the broader physical AI build-out, where the humanoid value chain extends across multiple regions, can hold HMND. Held together, they capture both stages of the same transition, with one focused on building capability and the other on applying it. Both have outperformed the Nasdaq 100 since the start of 2024, and the gap is widening as deployment becomes the story.

Software built the system. Hardware is making it run.