The Australian share market has spent much of the past decade lagging global equities, as investors increasingly looked offshore for structural growth opportunities in areas such as artificial intelligence. Yet while broad local market returns have disappointed relative to global shares, income-oriented strategies have quietly emerged as some of the strongest performing domestic equity strategies.

Recent changes to Australia's capital gains tax (CGT) regime may reinforce this trend. For decades, the tax system has encouraged investors to maximise capital growth through concessional treatment of long-term gains. However, the introduction of inflation indexation and a minimum 30% tax rate on capital gains may alter the relative attractiveness of income-producing assets.

Key Takeaways:

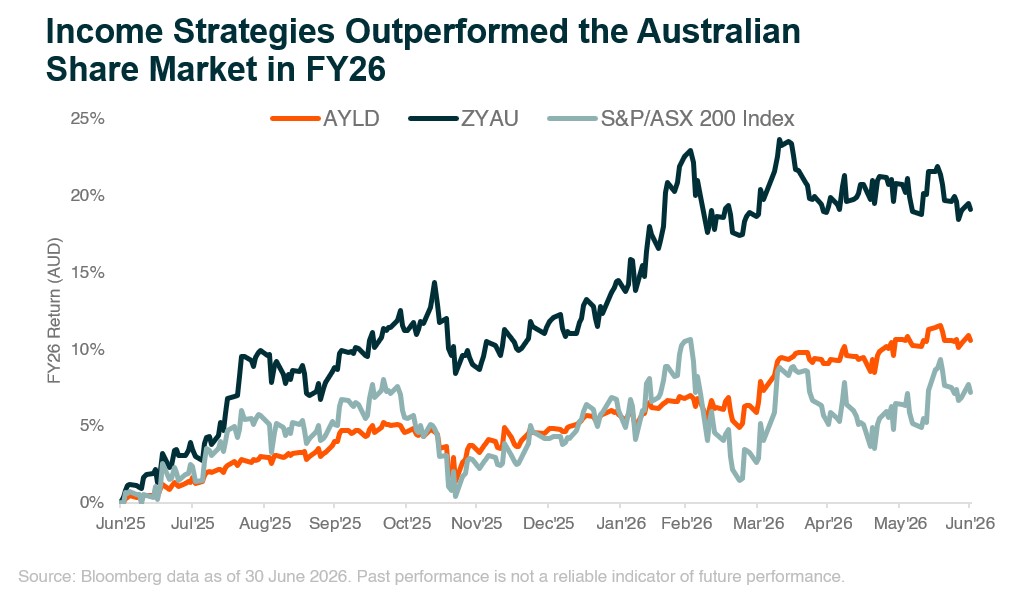

- Australian equities underperformed global markets for a fourth consecutive financial year in FY26, recording their weakest annual performance in four years. Yet beneath the surface, income-oriented strategies including high dividend and covered call approaches outperformed the broader Australian share market.

- The government's CGT reforms may accelerate a structural shift towards income investing. As the historical tax advantage of capital growth narrows, investors may increasingly favour dividend-paying companies and franked income streams over speculative growth and small-cap investments.

- Investors may need to think not only about how much return a portfolio generates, but also how those returns are delivered. For some investors, income-oriented strategies may produce superior after-tax outcomes than traditional growth strategies under the new CGT regime.

Australia’s Income Advantage Is Starting to Matter Again

For much of the past decade, Australian investors have faced a difficult trade-off. The domestic share market has remained a reliable source of dividends and franking credits, but global equities have increasingly become the engine of capital growth.

FY26 reinforced this divide. Australian equities delivered their weakest financial year return since 2022 and underperformed global equities for a fourth consecutive financial year.1 Much of that gap can be explained by the extraordinary strength of global technology and artificial intelligence beneficiaries, where Australian investors have limited domestic exposure.

Yet beneath the surface, income strategies told a very different story. Covered call strategies like the Global X S&P/ASX 200 Covered Call Complex ETF (AYLD) and high dividend strategies like the Global X S&P/ASX 200 High Dividend ETF (ZYAU) outperformed the broader Australian share market, highlighting that Australia’s equity market may be better understood as a key income opportunity.

Source: Bloomberg data as of 30 June 2026. Past performance is not a reliable indicator of future performance.

This matters because investors do not necessarily need Australian equities to play the same role as global equities. Global markets may remain the preferred destination for structural growth themes such as AI, semiconductors, and energy transition. Australia, by contrast, may increasingly serve a balancing act of providing dividend income and potential after-tax benefits like franking credits within a diversified portfolio.

In other words, the local equity market’s greatest weakness being its lack of high-growth technology exposure, may also reinforce its greatest strength: income. These tax changes could mean the bug has now become the feature.

Tax Reform Could Reinforce the Income Trade

The government’s CGT reforms may further strengthen the case for income investing. The reforms replace the 50% CGT discount with inflation indexation and introduce a minimum 30% tax rate on capital gains from 1 July 2027, with gains accrued before that date grandfathered.

For decades, the tax system rewarded investors for maximising capital growth. Investors could defer tax for years and then apply the 50% CGT discount when gains were eventually realised. That created a powerful incentive to favour capital appreciation over income.

The new regime changes that equation. Capital gains will still benefit from tax deferral and inflation indexation, although concerns remain around the asymmetrical treatment of gains and losses. Overall, however, the historical tax advantage of capital growth has narrowed. For investors whose marginal tax rate is below 30%, including many retirees and lower-income investors, capital gains may now be taxed more heavily than income.

This could have broader market implications. Investors may place a higher value on companies that can generate tangible cash flows, pay sustainable dividends and return capital to shareholders. Boards may also face greater pressure to justify reinvestment, acquisitions and long-dated growth projects if investors increasingly favour realised income over deferred capital gains.

This does not necessarily mean small cap or growth investing is dead. However, it may alter the competition for capital. Speculative growth businesses and early-stage companies could face a higher hurdle rate when raising capital, particularly where investment returns are uncertain or dependent on long-term capital appreciation. In some cases, this may encourage growth companies to seek capital offshore or list in markets where growth remains more highly valued.

Conversely, Australia's established dividend-paying sectors could become increasingly attractive. Banks, miners, infrastructure, telcos and other mature cash-generative businesses may benefit from a structural reallocation of capital from both domestic and international investors seeking income and potential after-tax benefits. If this occurs, Australia's long-standing dividend culture may evolve from a characteristic of the market into one of its most important competitive advantages.

The Source of Return May Matter More Than Before

For perhaps the first time in decades, investors may need to think not only about how much return a portfolio generates, but also how those returns are decomposed and delivered.

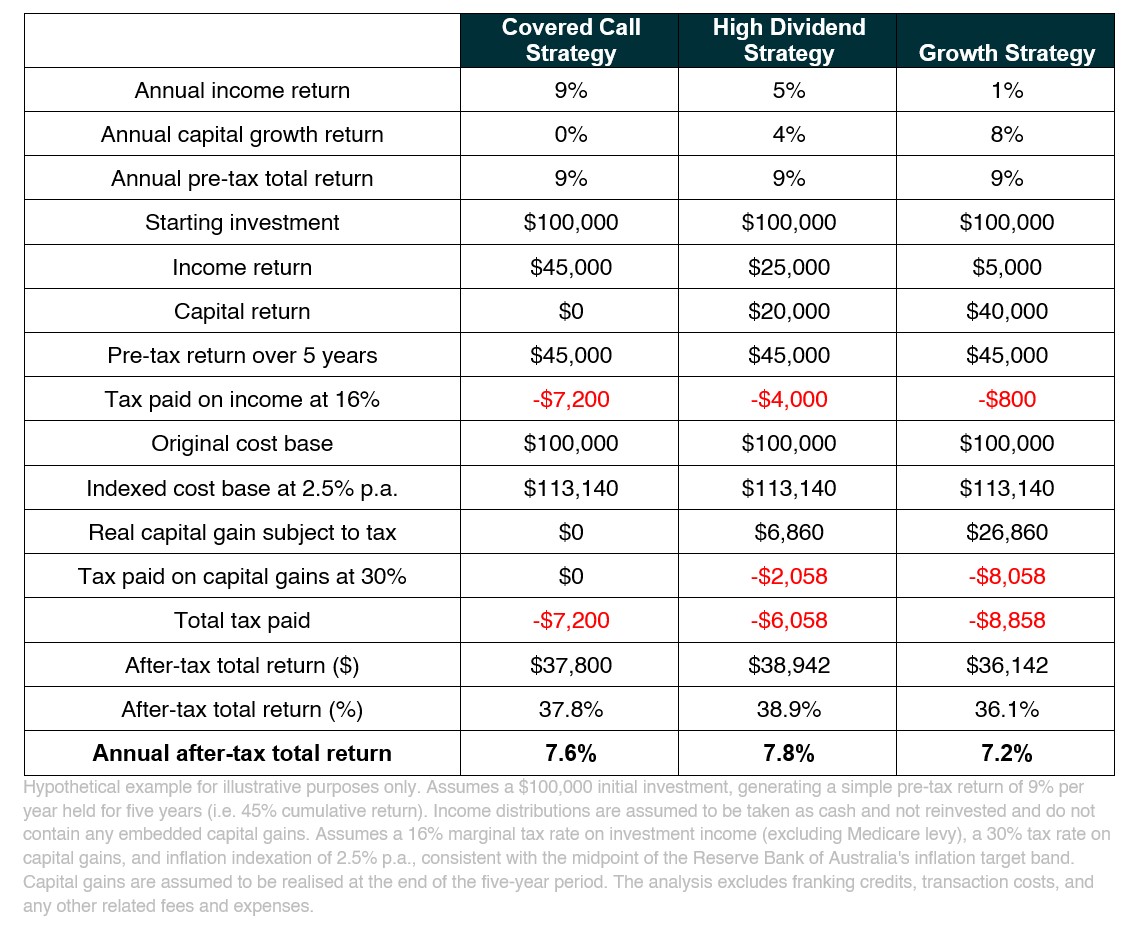

The implications of these new tax reforms are perhaps best illustrated by comparing after-tax outcomes. The example below assumes a typical retiree investor in a low-income tax bracket earns a total pre-tax return of 45% over five years, equivalent to approximately 9% per annum on a simple return basis. The only difference between the strategies is the source of return. A covered call strategy derives all of its return from income, a high dividend strategy derives a combination of income and capital growth, while a growth strategy derives the majority of its return from capital appreciation.

The results are revealing. The covered call strategy is likely to be the least affected by the new CGT regime, given that the majority, if not all, of its returns are derived from income rather than capital appreciation. The growth strategy benefits from lower annual taxation, but ultimately faces a larger tax bill when gains are realised. Meanwhile, the high dividend strategy sits in the middle, balancing income and capital growth, and ultimately delivers the highest after-tax return in our theoretical example.

This does not mean income investing will always triumph over growth investing. Rather, it suggests that the long-standing tax preference for capital growth has narrowed materially. In the years ahead, the optimal portfolio may depend on the balance between income and capital appreciation used to generate it. For years, Australian investors have gone offshore for growth and stayed local for income. The next phase of Australia's tax regime may only reinforce that trade.

The Next Era of Tax-Aware Investing

These reforms may ultimately go down as one of the most significant and controversial tax changes in Australian investing history. Whether investors agree with the changes or not, the reality is that they are scheduled to commence from 1 July 2027 and have the potential to reshape how Australians think about investing. Tax considerations should never override an investor's objectives, risk tolerance or strategic asset allocation. However, they do influence behaviour. If these reforms remain in place over the long term, investors may increasingly need to focus on after-tax outcomes, with income investing potentially re-emerging not simply as a source of portfolio cash flow, but as a source of tax alpha in its own right.

Related Funds

ZYAU: The Global X S&P/ASX 200 High Dividend ETF (ZYAU) invests in 50 high-dividend stocks from the S&P/ASX 200 Index.

AYLD: The Global X S&P/ASX 200 Covered Call Complex ETF (AYLD) writes call options on the S&P/ASX 200 Index, saving investors the time and potential expense of doing so individually.

Footnotes